- Japan

- /

- Electronic Equipment and Components

- /

- TSE:6856

Why Investors Shouldn't Be Surprised By HORIBA, Ltd.'s (TSE:6856) 26% Share Price Surge

HORIBA, Ltd. (TSE:6856) shares have had a really impressive month, gaining 26% after a shaky period beforehand. Not all shareholders will be feeling jubilant, since the share price is still down a very disappointing 35% in the last twelve months.

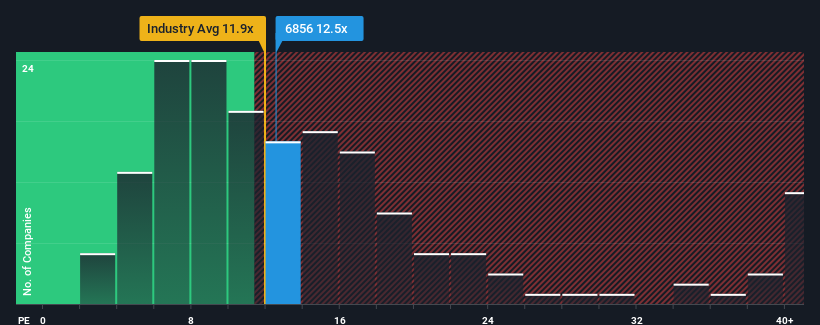

Although its price has surged higher, you could still be forgiven for feeling indifferent about HORIBA's P/E ratio of 12.5x, since the median price-to-earnings (or "P/E") ratio in Japan is also close to 13x. Although, it's not wise to simply ignore the P/E without explanation as investors may be disregarding a distinct opportunity or a costly mistake.

Our free stock report includes 1 warning sign investors should be aware of before investing in HORIBA. Read for free now.HORIBA hasn't been tracking well recently as its declining earnings compare poorly to other companies, which have seen some growth on average. One possibility is that the P/E is moderate because investors think this poor earnings performance will turn around. You'd really hope so, otherwise you're paying a relatively elevated price for a company with this sort of growth profile.

View our latest analysis for HORIBA

How Is HORIBA's Growth Trending?

There's an inherent assumption that a company should be matching the market for P/E ratios like HORIBA's to be considered reasonable.

Retrospectively, the last year delivered a frustrating 16% decrease to the company's bottom line. Still, the latest three year period has seen an excellent 59% overall rise in EPS, in spite of its unsatisfying short-term performance. Accordingly, while they would have preferred to keep the run going, shareholders would probably welcome the medium-term rates of earnings growth.

Turning to the outlook, the next three years should generate growth of 9.3% per annum as estimated by the nine analysts watching the company. That's shaping up to be similar to the 9.8% per annum growth forecast for the broader market.

In light of this, it's understandable that HORIBA's P/E sits in line with the majority of other companies. Apparently shareholders are comfortable to simply hold on while the company is keeping a low profile.

The Bottom Line On HORIBA's P/E

HORIBA's stock has a lot of momentum behind it lately, which has brought its P/E level with the market. While the price-to-earnings ratio shouldn't be the defining factor in whether you buy a stock or not, it's quite a capable barometer of earnings expectations.

As we suspected, our examination of HORIBA's analyst forecasts revealed that its market-matching earnings outlook is contributing to its current P/E. Right now shareholders are comfortable with the P/E as they are quite confident future earnings won't throw up any surprises. It's hard to see the share price moving strongly in either direction in the near future under these circumstances.

And what about other risks? Every company has them, and we've spotted 1 warning sign for HORIBA you should know about.

If these risks are making you reconsider your opinion on HORIBA, explore our interactive list of high quality stocks to get an idea of what else is out there.

Valuation is complex, but we're here to simplify it.

Discover if HORIBA might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About TSE:6856

Flawless balance sheet, good value and pays a dividend.

Similar Companies

Market Insights

Community Narratives