- Japan

- /

- Professional Services

- /

- TSE:6200

Nippon Electric Glass And Two More Stocks Possibly Trading Below Value Estimates On Japanese Exchange

Reviewed by Simply Wall St

Japan's stock markets recently showcased robust performance, with major indices like the Nikkei 225 and TOPIX reaching all-time highs amid a backdrop of economic shifts. This surge reflects a complex interplay of factors including wage increases and currency fluctuations, setting an intriguing stage for investors looking at potentially undervalued stocks. In such a market environment, discerning investors might find opportunities in stocks that are trading below their intrinsic values, possibly due to temporary market dynamics or overlooked growth prospects.

Top 10 Undervalued Stocks Based On Cash Flows In Japan

| Name | Current Price | Fair Value (Est) | Discount (Est) |

| Mimaki Engineering (TSE:6638) | ¥2082.00 | ¥3946.90 | 47.2% |

| Fujibo Holdings (TSE:3104) | ¥4775.00 | ¥9416.60 | 49.3% |

| S-Pool (TSE:2471) | ¥318.00 | ¥619.81 | 48.7% |

| Medley (TSE:4480) | ¥3745.00 | ¥7111.59 | 47.3% |

| Cyber Security Cloud (TSE:4493) | ¥2220.00 | ¥4326.96 | 48.7% |

| Macromill (TSE:3978) | ¥855.00 | ¥1666.28 | 48.7% |

| Yokowo (TSE:6800) | ¥2049.00 | ¥3909.95 | 47.6% |

| DKS (TSE:4461) | ¥3745.00 | ¥7223.38 | 48.2% |

| Bushiroad (TSE:7803) | ¥377.00 | ¥716.25 | 47.4% |

| Money Forward (TSE:3994) | ¥5350.00 | ¥10381.15 | 48.5% |

Below we spotlight a couple of our favorites from our exclusive screener.

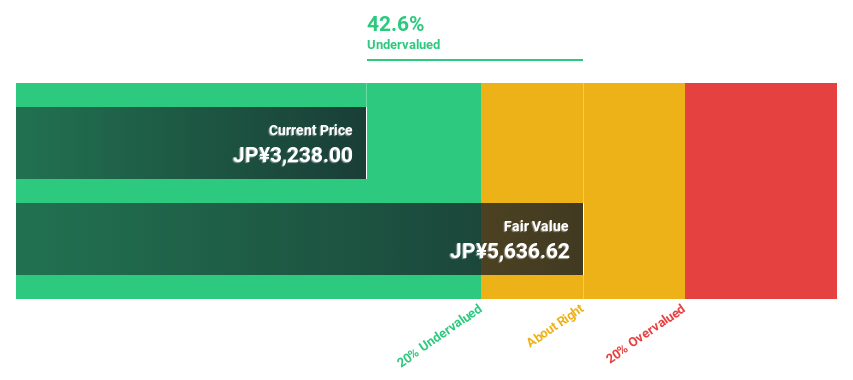

Nippon Electric Glass (TSE:5214)

Overview: Nippon Electric Glass Co., Ltd. is a global manufacturer and seller of specialty glass products and glass-making machinery, operating primarily in Japan, China, South Korea, the United States, and Europe, with a market capitalization of approximately ¥316.04 billion.

Operations: The company generates its revenue from the manufacture and sale of specialty glass products and glass-making machinery across key regions including Japan, China, South Korea, the United States, and Europe.

Estimated Discount To Fair Value: 35.2%

Nippon Electric Glass, priced at ¥3650, trades significantly below our fair value estimate of ¥5633.89, highlighting its undervalued status based on cash flows. Despite a dividend yield of 3.56%, coverage by earnings and free cash flows is weak, suggesting potential sustainability issues. The company's recent development of the GC CoreTM substrate could enhance semiconductor performance and reduce production costs, potentially boosting future profitability which is expected to grow robustly over the next three years. However, its forecasted revenue growth at 5.4% annually lags behind more aggressive market averages.

- Our growth report here indicates Nippon Electric Glass may be poised for an improving outlook.

- Unlock comprehensive insights into our analysis of Nippon Electric Glass stock in this financial health report.

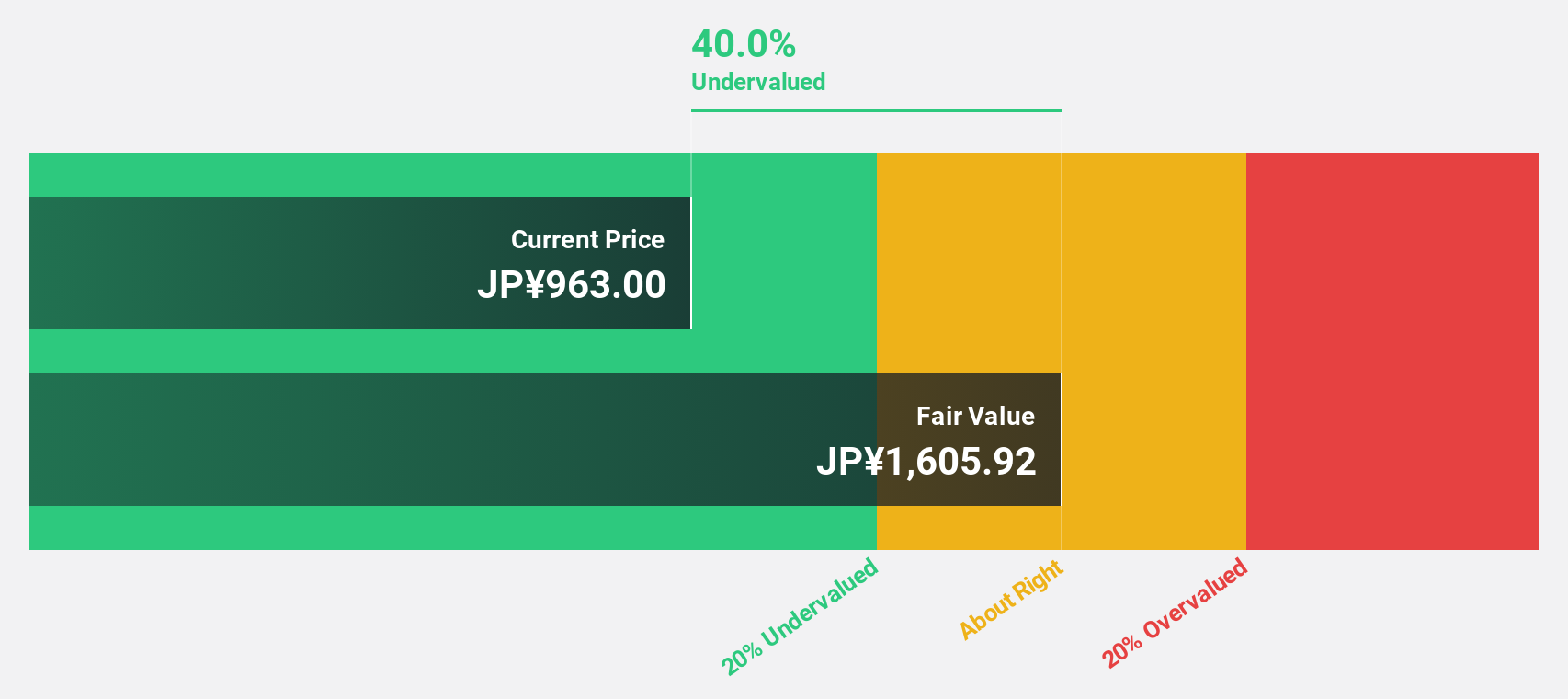

Insource (TSE:6200)

Overview: Insource Co., Ltd., operating in Japan, offers a range of services including lecturer dispatch training and open lectures, with a market capitalization of ¥70.10 billion.

Operations: The company generates revenue primarily through its services related to lecturer dispatch training and open lectures.

Estimated Discount To Fair Value: 41.9%

Insource, priced at ¥836, is undervalued based on DCF with a fair value of ¥1438.29. The company's earnings are forecast to grow by 17.98% annually, outpacing the Japanese market average. Despite this growth potential and a high projected ROE of 36.5%, its dividend track record remains unstable and the share price has been highly volatile recently. Additionally, Insource's recent expansion into three new locations could bolster client services and support continued revenue growth, which is expected to exceed the market average at 15.3% annually.

- Our expertly prepared growth report on Insource implies its future financial outlook may be stronger than recent results.

- Take a closer look at Insource's balance sheet health here in our report.

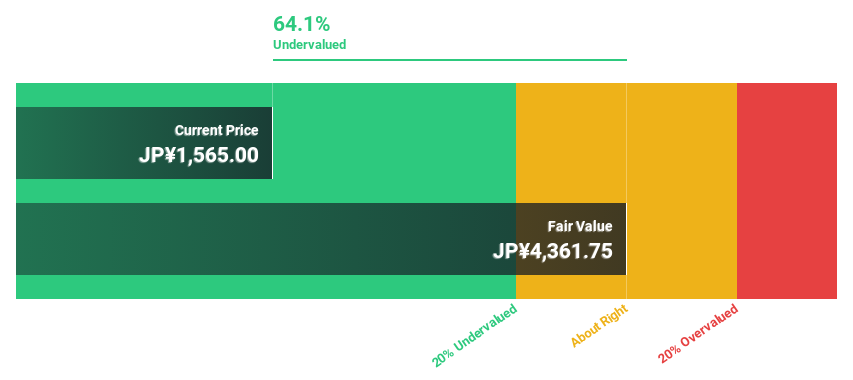

Mimaki Engineering (TSE:6638)

Overview: Mimaki Engineering Co., Ltd. specializes in developing, manufacturing, and selling computer devices and software both in Japan and internationally, with a market capitalization of approximately ¥59.95 billion.

Operations: The company generates revenue from the development, manufacture, and sale of computer devices and software across domestic and international markets.

Estimated Discount To Fair Value: 47.2%

Mimaki Engineering, trading at ¥2082, is significantly undervalued with a fair value estimate of ¥3946.9. The company's earnings are expected to grow by 20.23% annually, surpassing the Japanese market forecast of 9%. Despite its high volatility in share price, Mimaki has shown strong past earnings growth of 32.1% last year and anticipates revenue growth at 8.5% per year—double the market's rate. Recent corporate guidance projects robust financials for FY2025 with substantial increases in net sales and profits, alongside consistent dividends.

- According our earnings growth report, there's an indication that Mimaki Engineering might be ready to expand.

- Click here to discover the nuances of Mimaki Engineering with our detailed financial health report.

Make It Happen

- Gain an insight into the universe of 90 Undervalued Japanese Stocks Based On Cash Flows by clicking here.

- Already own these companies? Link your portfolio to Simply Wall St and get alerts on any new warning signs to your stocks.

- Simply Wall St is a revolutionary app designed for long-term stock investors, it's free and covers every market in the world.

Looking For Alternative Opportunities?

- Explore high-performing small cap companies that haven't yet garnered significant analyst attention.

- Diversify your portfolio with solid dividend payers offering reliable income streams to weather potential market turbulence.

- Fuel your portfolio with companies showing strong growth potential, backed by optimistic outlooks both from analysts and management.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

New: AI Stock Screener & Alerts

Our new AI Stock Screener scans the market every day to uncover opportunities.

• Dividend Powerhouses (3%+ Yield)

• Undervalued Small Caps with Insider Buying

• High growth Tech and AI Companies

Or build your own from over 50 metrics.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About TSE:6200

Insource

Provides various lecturer dispatch type training, open lecture, and other services in Japan.

Flawless balance sheet with solid track record.