- Japan

- /

- Electronic Equipment and Components

- /

- TSE:4062

Ibiden Co.,Ltd. Just Missed EPS By 48%: Here's What Analysts Think Will Happen Next

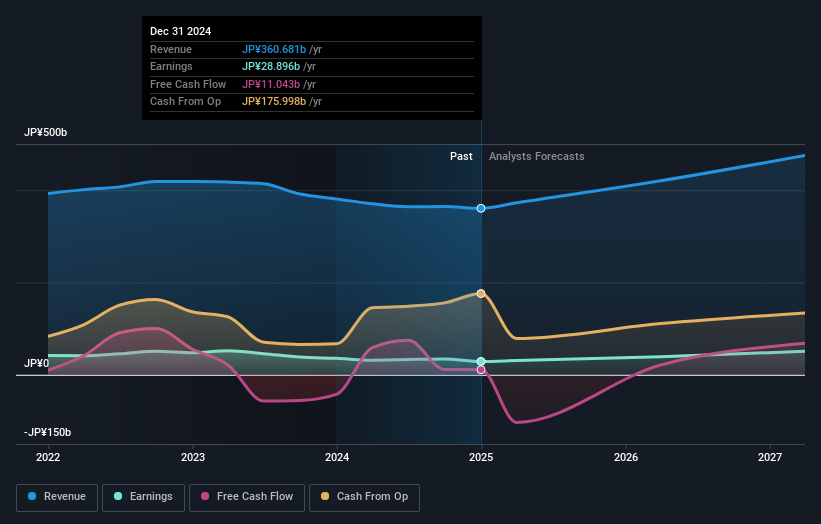

Ibiden Co.,Ltd. (TSE:4062) just released its latest quarterly report and things are not looking great. Results showed a clear earnings miss, with JP¥89b revenue coming in 6.9% lower than what the analystsexpected. Statutory earnings per share (EPS) of JP¥30.64 missed the mark badly, arriving some 48% below what was expected. The analysts typically update their forecasts at each earnings report, and we can judge from their estimates whether their view of the company has changed or if there are any new concerns to be aware of. Readers will be glad to know we've aggregated the latest statutory forecasts to see whether the analysts have changed their mind on IbidenLtd after the latest results.

Check out our latest analysis for IbidenLtd

Taking into account the latest results, the current consensus from IbidenLtd's 17 analysts is for revenues of JP¥420.3b in 2026. This would reflect a meaningful 17% increase on its revenue over the past 12 months. Statutory earnings per share are predicted to leap 34% to JP¥278. In the lead-up to this report, the analysts had been modelling revenues of JP¥423.4b and earnings per share (EPS) of JP¥288 in 2026. So it looks like there's been a small decline in overall sentiment after the recent results - there's been no major change to revenue estimates, but the analysts did make a minor downgrade to their earnings per share forecasts.

The consensus price target held steady at JP¥6,076, with the analysts seemingly voting that their lower forecast earnings are not expected to lead to a lower stock price in the foreseeable future. It could also be instructive to look at the range of analyst estimates, to evaluate how different the outlier opinions are from the mean. There are some variant perceptions on IbidenLtd, with the most bullish analyst valuing it at JP¥7,655 and the most bearish at JP¥4,500 per share. Analysts definitely have varying views on the business, but the spread of estimates is not wide enough in our view to suggest that extreme outcomes could await IbidenLtd shareholders.

Looking at the bigger picture now, one of the ways we can make sense of these forecasts is to see how they measure up against both past performance and industry growth estimates. It's clear from the latest estimates that IbidenLtd's rate of growth is expected to accelerate meaningfully, with the forecast 13% annualised revenue growth to the end of 2026 noticeably faster than its historical growth of 5.2% p.a. over the past five years. Compare this with other companies in the same industry, which are forecast to grow their revenue 7.3% annually. It seems obvious that, while the growth outlook is brighter than the recent past, the analysts also expect IbidenLtd to grow faster than the wider industry.

The Bottom Line

The biggest concern is that the analysts reduced their earnings per share estimates, suggesting business headwinds could lay ahead for IbidenLtd. Fortunately, they also reconfirmed their revenue numbers, suggesting that it's tracking in line with expectations. Additionally, our data suggests that revenue is expected to grow faster than the wider industry. The consensus price target held steady at JP¥6,076, with the latest estimates not enough to have an impact on their price targets.

With that in mind, we wouldn't be too quick to come to a conclusion on IbidenLtd. Long-term earnings power is much more important than next year's profits. We have forecasts for IbidenLtd going out to 2027, and you can see them free on our platform here.

It is also worth noting that we have found 1 warning sign for IbidenLtd that you need to take into consideration.

Mobile Infrastructure for Defense and Disaster

The next wave in robotics isn't humanoid. Its fully autonomous towers delivering 5G, ISR, and radar in under 30 minutes, anywhere.

Get the investor briefing before the next round of contracts

Sponsored On Behalf of CiTechNew: AI Stock Screener & Alerts

Our new AI Stock Screener scans the market every day to uncover opportunities.

• Dividend Powerhouses (3%+ Yield)

• Undervalued Small Caps with Insider Buying

• High growth Tech and AI Companies

Or build your own from over 50 metrics.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About TSE:4062

IbidenLtd

Manufactures and sells electronic and ceramics products in Japan, Asia, North America, and internationally.

Excellent balance sheet with reasonable growth potential.

Similar Companies

Market Insights

Weekly Picks

Early mover in a fast growing industry. Likely to experience share price volatility as they scale

A case for CA$31.80 (undiluted), aka 8,616% upside from CA$0.37 (an 86 bagger!).

Moderation and Stabilisation: HOLD: Fair Price based on a 4-year Cycle is $12.08

Recently Updated Narratives

Airbnb Stock: Platform Growth in a World of Saturation and Scrutiny

Adobe Stock: AI-Fueled ARR Growth Pushes Guidance Higher, But Cost Pressures Loom

Thomson Reuters Stock: When Legal Intelligence Becomes Mission-Critical Infrastructure

Popular Narratives

Crazy Undervalued 42 Baggers Silver Play (Active & Running Mine)

NVDA: Expanding AI Demand Will Drive Major Data Center Investments Through 2026

The AI Infrastructure Giant Grows Into Its Valuation

Trending Discussion