Advertisement

- Japan

- /

- Electronic Equipment and Components

- /

- TSE:3107

Daiwabo Holdings (TSE:3107): Valuation Insights Following Strategic IT Workforce Partnership with BCC

Simply Wall St

Reviewed by Simply Wall St

Daiwabo Holdings (TSE:3107) has entered into a capital and business partnership with BCC Co., Ltd., with the goal of deepening collaboration in IT workforce solutions. The move is intended to help address labor shortages and expand new business opportunities.

See our latest analysis for Daiwabo Holdings.

Daiwabo Holdings’ latest partnership follows a period of renewed optimism, with the share price gaining 7.8% over the past month and returning 2.9% to shareholders in the last year. Momentum has been somewhat patchy. However, the company’s longer-term total shareholder return of over 170% in five years still stands out compared to many peers.

If Daiwabo’s strategic moves interest you, it is a great moment to expand your search and discover fast growing stocks with high insider ownership

But with shares rallying recently and a discounted valuation compared to analyst targets, the question remains: is Daiwabo Holdings a bargain, or has the market already accounted for its potential for future growth?

Price-to-Earnings of 8.7x: Is it justified?

Daiwabo Holdings is trading at a price-to-earnings (P/E) ratio of 8.7x, which is well below the Japanese electronic industry average and peer levels. Based on the last close price, the shares appear attractively valued relative to comparable companies in its sector.

The price-to-earnings ratio measures the price that investors are willing to pay for each unit of Daiwabo's earnings. This is a common way for the market to gauge how much confidence there is in a company’s future profit potential, particularly relevant for established firms in technology distribution and industrial equipment, like Daiwabo Holdings.

With Daiwabo’s P/E at 8.7x, well beneath the peer average of 15.5x and the industry average of 14.6x, the market seems to be pricing in modest or even declining earnings growth, despite a year of exceptional profit gains. Notably, this P/E is also under the estimated fair price-to-earnings ratio of 13.2x, suggesting that the market could move higher if sentiment improves or earnings outlooks change.

Explore the SWS fair ratio for Daiwabo Holdings

Result: Price-to-Earnings of 8.7x (UNDERVALUED)

However, risks such as recent declines in both annual revenue and net income growth could signal challenges ahead for Daiwabo's outlook.

Find out about the key risks to this Daiwabo Holdings narrative.

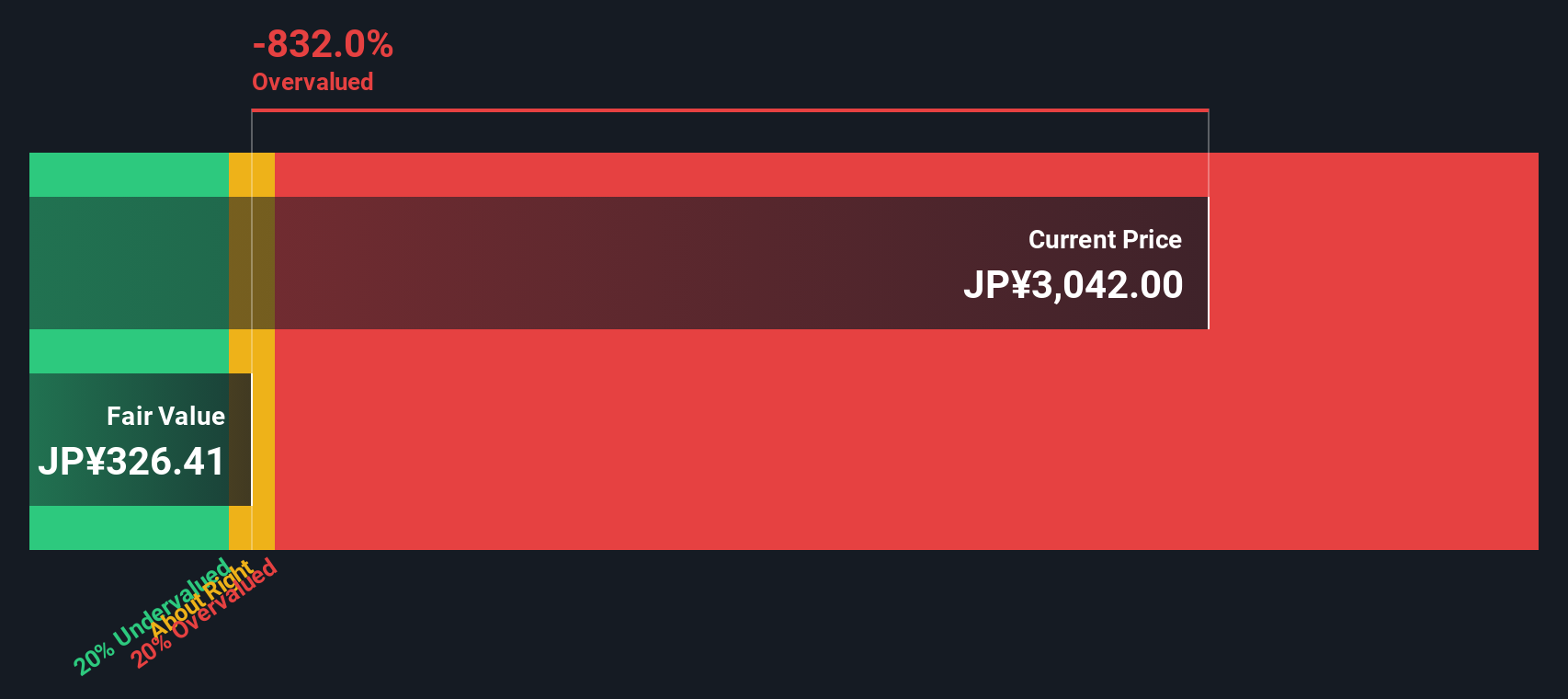

Another View: DCF Model Puts the Brakes On

While Daiwabo Holdings looks cheap using earnings ratios, the SWS DCF model tells a different story. According to our DCF calculations, the shares are actually trading above fair value. This suggests the market might be more optimistic than the fundamentals warrant right now. When methods disagree, which lens should investors trust?

Look into how the SWS DCF model arrives at its fair value.

Simply Wall St performs a discounted cash flow (DCF) on every stock in the world every day (check out Daiwabo Holdings for example). We show the entire calculation in full. You can track the result in your watchlist or portfolio and be alerted when this changes, or use our stock screener to discover 920 undervalued stocks based on their cash flows. If you save a screener we even alert you when new companies match - so you never miss a potential opportunity.

Build Your Own Daiwabo Holdings Narrative

If you have a different perspective or prefer hands-on analysis, you can quickly build your own view using our tools in just a few minutes. Why not Do it your way?

A great starting point for your Daiwabo Holdings research is our analysis highlighting 3 key rewards and 3 important warning signs that could impact your investment decision.

Looking for more investment ideas?

Smart investors always keep an eye on what’s next. Take control of your portfolio’s growth by tapping into powerful trends and emerging market leaders today.

- Supercharge your returns by chasing these 920 undervalued stocks based on cash flows and uncovering opportunities the market has not fully recognized yet.

- Target steady passive income streams by tapping into these 15 dividend stocks with yields > 3% with attractive yields and strong fundamentals.

- Ride the AI innovation wave as you connect with leading-edge companies among these 25 AI penny stocks shaping tomorrow’s world.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

New: Manage All Your Stock Portfolios in One Place

We've created the ultimate portfolio companion for stock investors, and it's free.

• Connect an unlimited number of Portfolios and see your total in one currency

• Be alerted to new Warning Signs or Risks via email or mobile

• Track the Fair Value of your stocks

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About TSE:3107

Flawless balance sheet average dividend payer.

Market Insights

Advertisement

Community Narratives

MicroVision will explode future revenue by 380.37% with a vision towards success

Fair Value US$60|98.4% undervalued

TH

Community Contributor

The Indispensable Artery for a New North American Economy

Fair Value CA$132.87|0.7% overvalued

TI

Community Contributor

Recently Updated Narratives

CO

composite32 on Astor Enerji ·

Astor Enerji will surge with a fair value of $140.43 in the next 3 years

Fair Value:₺140.4335.5% undervalued

1 followerusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

RE

RecMag on Proximus ·

Proximus: The State-Backed Backup Plan with 7% Gross Yield and 15% Currency Upside.

Fair Value:€17.1356.7% undervalued

30 followersusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

AG

Agricola on IMPACT Silver ·

A case for for IMPACT Silver Corp (TSXV:IPT) to reach USD $4.52 (CAD $6.16) in 2026 (23 bagger in 1 year) and USD $5.76 (CAD $7.89) by 2030

Fair Value:CA$7.8996.2% undervalued

1 followerusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

Popular Narratives

TH

TheWallstreetKing on MicroVision ·

MicroVision will explode future revenue by 380.37% with a vision towards success

Fair Value:US$6098.4% undervalued

101 followersusers have followed this narrative

10 commentsusers have commented on this narrative

20 likesusers have liked this narrative

OS

oscargarcia on Alphabet ·

The company that turned a verb into a global necessity and basically runs the modern internet, digital ads, smartphones, maps, and AI.

Fair Value:US$3405.8% undervalued

138 followersusers have followed this narrative

6 commentsusers have commented on this narrative

18 likesusers have liked this narrative

AN

AnalystConsensusTarget on NVIDIA ·

NVDA: Expanding AI Demand Will Drive Major Data Center Investments Through 2026

Fair Value:US$250.3929.3% undervalued

930 followersusers have followed this narrative

6 commentsusers have commented on this narrative

23 likesusers have liked this narrative