- Japan

- /

- Electronic Equipment and Components

- /

- TSE:3670

Returns On Capital At Kyoritsu Computer & CommunicationLtd (TYO:3670) Paint A Concerning Picture

When we're researching a company, it's sometimes hard to find the warning signs, but there are some financial metrics that can help spot trouble early. Typically, we'll see the trend of both return on capital employed (ROCE) declining and this usually coincides with a decreasing amount of capital employed. This indicates to us that the business is not only shrinking the size of its net assets, but its returns are falling as well. In light of that, from a first glance at Kyoritsu Computer & CommunicationLtd (TYO:3670), we've spotted some signs that it could be struggling, so let's investigate.

Return On Capital Employed (ROCE): What is it?

For those who don't know, ROCE is a measure of a company's yearly pre-tax profit (its return), relative to the capital employed in the business. The formula for this calculation on Kyoritsu Computer & CommunicationLtd is:

Return on Capital Employed = Earnings Before Interest and Tax (EBIT) ÷ (Total Assets - Current Liabilities)

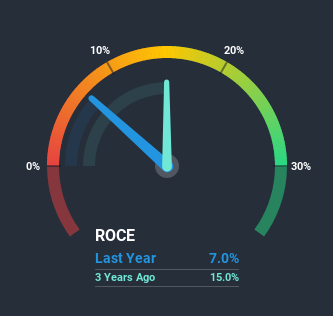

0.07 = JP¥147m ÷ (JP¥2.8b - JP¥733m) (Based on the trailing twelve months to November 2020).

So, Kyoritsu Computer & CommunicationLtd has an ROCE of 7.0%. Even though it's in line with the industry average of 7.3%, it's still a low return by itself.

Check out our latest analysis for Kyoritsu Computer & CommunicationLtd

While the past is not representative of the future, it can be helpful to know how a company has performed historically, which is why we have this chart above. If you're interested in investigating Kyoritsu Computer & CommunicationLtd's past further, check out this free graph of past earnings, revenue and cash flow.

What Does the ROCE Trend For Kyoritsu Computer & CommunicationLtd Tell Us?

We are a bit worried about the trend of returns on capital at Kyoritsu Computer & CommunicationLtd. About three years ago, returns on capital were 15%, however they're now substantially lower than that as we saw above. Meanwhile, capital employed in the business has stayed roughly the flat over the period. Companies that exhibit these attributes tend to not be shrinking, but they can be mature and facing pressure on their margins from competition. If these trends continue, we wouldn't expect Kyoritsu Computer & CommunicationLtd to turn into a multi-bagger.

What We Can Learn From Kyoritsu Computer & CommunicationLtd's ROCE

In summary, it's unfortunate that Kyoritsu Computer & CommunicationLtd is generating lower returns from the same amount of capital. Investors must expect better things on the horizon though because the stock has risen 20% in the last five years. Either way, we aren't huge fans of the current trends and so with that we think you might find better investments elsewhere.

Kyoritsu Computer & CommunicationLtd does come with some risks though, we found 4 warning signs in our investment analysis, and 1 of those makes us a bit uncomfortable...

While Kyoritsu Computer & CommunicationLtd may not currently earn the highest returns, we've compiled a list of companies that currently earn more than 25% return on equity. Check out this free list here.

When trading Kyoritsu Computer & CommunicationLtd or any other investment, use the platform considered by many to be the Professional's Gateway to the Worlds Market, Interactive Brokers. You get the lowest-cost* trading on stocks, options, futures, forex, bonds and funds worldwide from a single integrated account. Promoted

Mobile Infrastructure for Defense and Disaster

The next wave in robotics isn't humanoid. Its fully autonomous towers delivering 5G, ISR, and radar in under 30 minutes, anywhere.

Get the investor briefing before the next round of contracts

Sponsored On Behalf of CiTechValuation is complex, but we're here to simplify it.

Discover if Kyoritsu Computer & CommunicationLtd might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisThis article by Simply Wall St is general in nature. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

*Interactive Brokers Rated Lowest Cost Broker by StockBrokers.com Annual Online Review 2020

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

About TSE:3670

Kyoritsu Computer & CommunicationLtd

Kyoritsu Computer & Communication Co.,Ltd.

Very low risk not a dividend payer.

Market Insights

Weekly Picks

Early mover in a fast growing industry. Likely to experience share price volatility as they scale

A case for CA$31.80 (undiluted), aka 8,616% upside from CA$0.37 (an 86 bagger!).

Moderation and Stabilisation: HOLD: Fair Price based on a 4-year Cycle is $12.08

Recently Updated Narratives

An amazing opportunity to potentially get a 100 bagger

Amazon: Why the World’s Biggest Platform Still Runs on Invisible Economics

Sunrun Stock: When the Energy Transition Collides With the Cost of Capital

Popular Narratives

MicroVision will explode future revenue by 380.37% with a vision towards success

Crazy Undervalued 42 Baggers Silver Play (Active & Running Mine)