Advertisement

Some investors rely on dividends for growing their wealth, and if you're one of those dividend sleuths, you might be intrigued to know that Rococo Co. Ltd. (TSE:5868) is about to go ex-dividend in just 3 days. The ex-dividend date occurs one day before the record date which is the day on which shareholders need to be on the company's books in order to receive a dividend. The ex-dividend date is important because any transaction on a stock needs to have been settled before the record date in order to be eligible for a dividend. Meaning, you will need to purchase Rococo's shares before the 27th of December to receive the dividend, which will be paid on the 29th of March.

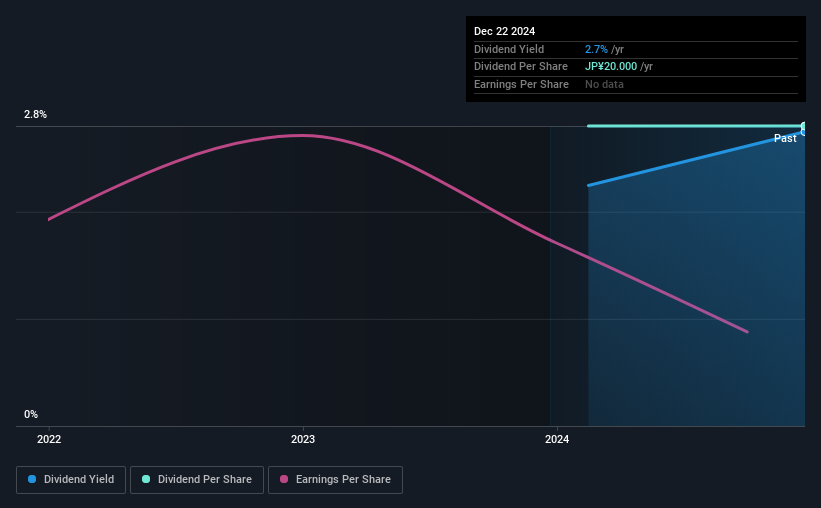

The company's next dividend payment will be JP¥20.00 per share. Last year, in total, the company distributed JP¥20.00 to shareholders. Last year's total dividend payments show that Rococo has a trailing yield of 2.7% on the current share price of JP¥728.00. We love seeing companies pay a dividend, but it's also important to be sure that laying the golden eggs isn't going to kill our golden goose! We need to see whether the dividend is covered by earnings and if it's growing.

View our latest analysis for Rococo

Dividends are typically paid out of company income, so if a company pays out more than it earned, its dividend is usually at a higher risk of being cut. That's why it's good to see Rococo paying out a modest 35% of its earnings.

Click here to see how much of its profit Rococo paid out over the last 12 months.

Have Earnings And Dividends Been Growing?

Businesses with shrinking earnings are tricky from a dividend perspective. Investors love dividends, so if earnings fall and the dividend is reduced, expect a stock to be sold off heavily at the same time. Rococo's earnings per share have fallen at approximately 16% a year over the previous three years. When earnings per share fall, the maximum amount of dividends that can be paid also falls.

Rococo also issued more than 5% of its market cap in new stock during the past year, which we feel is likely to hurt its dividend prospects in the long run. It's hard to grow dividends per share when a company keeps creating new shares.

Given that Rococo has only been paying a dividend for a year, there's not much of a past history to draw insight from.

Final Takeaway

Should investors buy Rococo for the upcoming dividend? Rococo's earnings per share are down over the past three years, although it has the cushion of a low payout ratio, which would suggest a cut to the dividend is relatively unlikely. We think there are likely better opportunities out there.

So if you want to do more digging on Rococo, you'll find it worthwhile knowing the risks that this stock faces. Our analysis shows 3 warning signs for Rococo and you should be aware of these before buying any shares.

Generally, we wouldn't recommend just buying the first dividend stock you see. Here's a curated list of interesting stocks that are strong dividend payers.

New: AI Stock Screener & Alerts

Our new AI Stock Screener scans the market every day to uncover opportunities.

• Dividend Powerhouses (3%+ Yield)

• Undervalued Small Caps with Insider Buying

• High growth Tech and AI Companies

Or build your own from over 50 metrics.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About TSE:5868

Excellent balance sheet and good value.

Market Insights

Advertisement

Community Narratives

A Quality Compounder Marked Down on Overblown Fears

Fair Value US$120.72|60.9% undervalued

BA

Community Contributor

Wyndham Continues Global Expansion with 19% Ancillary Revenue Growth

Fair Value US$105.80|19.7% undervalued

ZW

Community Contributor