Advertisement

HIMACS' (TSE:4299) Conservative Accounting Might Explain Soft Earnings

Shareholders appeared unconcerned with HIMACS, Ltd.'s (TSE:4299) lackluster earnings report last week. Our analysis suggests that while the profits are soft, the foundations of the business are strong.

View our latest analysis for HIMACS

A Closer Look At HIMACS' Earnings

As finance nerds would already know, the accrual ratio from cashflow is a key measure for assessing how well a company's free cash flow (FCF) matches its profit. In plain english, this ratio subtracts FCF from net profit, and divides that number by the company's average operating assets over that period. This ratio tells us how much of a company's profit is not backed by free cashflow.

Therefore, it's actually considered a good thing when a company has a negative accrual ratio, but a bad thing if its accrual ratio is positive. That is not intended to imply we should worry about a positive accrual ratio, but it's worth noting where the accrual ratio is rather high. To quote a 2014 paper by Lewellen and Resutek, "firms with higher accruals tend to be less profitable in the future".

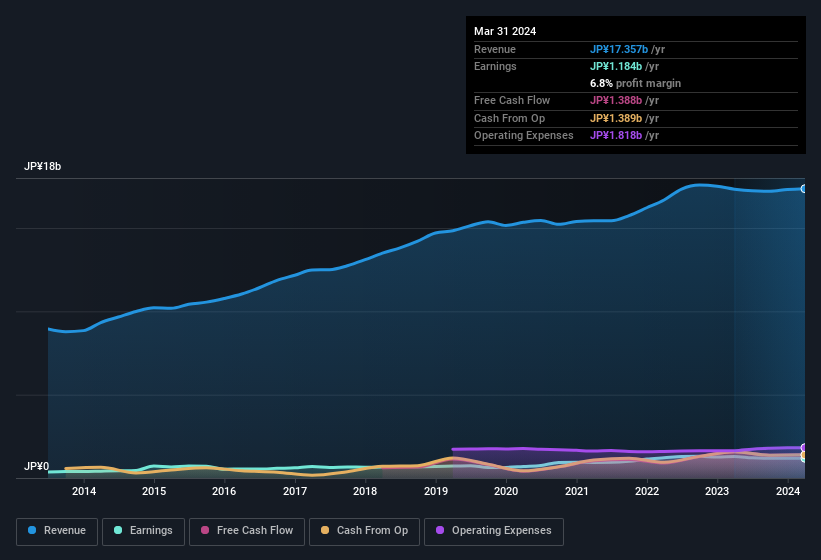

For the year to March 2024, HIMACS had an accrual ratio of -0.14. That indicates that its free cash flow was a fair bit more than its statutory profit. To wit, it produced free cash flow of JP¥1.4b during the period, dwarfing its reported profit of JP¥1.18b. HIMACS' free cash flow actually declined over the last year, which is disappointing, like non-biodegradable balloons.

Note: we always recommend investors check balance sheet strength. Click here to be taken to our balance sheet analysis of HIMACS.

Our Take On HIMACS' Profit Performance

As we discussed above, HIMACS has perfectly satisfactory free cash flow relative to profit. Based on this observation, we consider it likely that HIMACS' statutory profit actually understates its earnings potential! And on top of that, its earnings per share have grown at 29% per year over the last three years. Of course, we've only just scratched the surface when it comes to analysing its earnings; one could also consider margins, forecast growth, and return on investment, among other factors. With this in mind, we wouldn't consider investing in a stock unless we had a thorough understanding of the risks. At Simply Wall St, we found 1 warning sign for HIMACS and we think they deserve your attention.

This note has only looked at a single factor that sheds light on the nature of HIMACS' profit. But there is always more to discover if you are capable of focussing your mind on minutiae. Some people consider a high return on equity to be a good sign of a quality business. While it might take a little research on your behalf, you may find this free collection of companies boasting high return on equity, or this list of stocks with significant insider holdings to be useful.

Valuation is complex, but we're here to simplify it.

Discover if HIMACS might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About TSE:4299

HIMACS

Provides defined valued processes for various system lifecycles in Japan.

Flawless balance sheet 6 star dividend payer.

Market Insights

Advertisement

Community Narratives

A formidable player in AI and enterprise computing.

Fair Value US$210.00|12.2% overvalued

CO

Community Contributor

IREN's Bold Moves in Sustainable Bitcoin Mining & AI Data Centers

Fair Value US$72.52|17.1% undervalued

BL

Community Contributor

Cooling the Champions: The Aussie Tech Behind F1's Victories

Fair Value AU$12.40|38.7% undervalued

TR

Community Contributor