Advertisement

Readers hoping to buy Kinjiro Co.,Ltd. (TSE:4013) for its dividend will need to make their move shortly, as the stock is about to trade ex-dividend. The ex-dividend date is one business day before a company's record date, which is the date on which the company determines which shareholders are entitled to receive a dividend. The ex-dividend date is an important date to be aware of as any purchase of the stock made on or after this date might mean a late settlement that doesn't show on the record date. Accordingly, KinjiroLtd investors that purchase the stock on or after the 27th of December will not receive the dividend, which will be paid on the 25th of March.

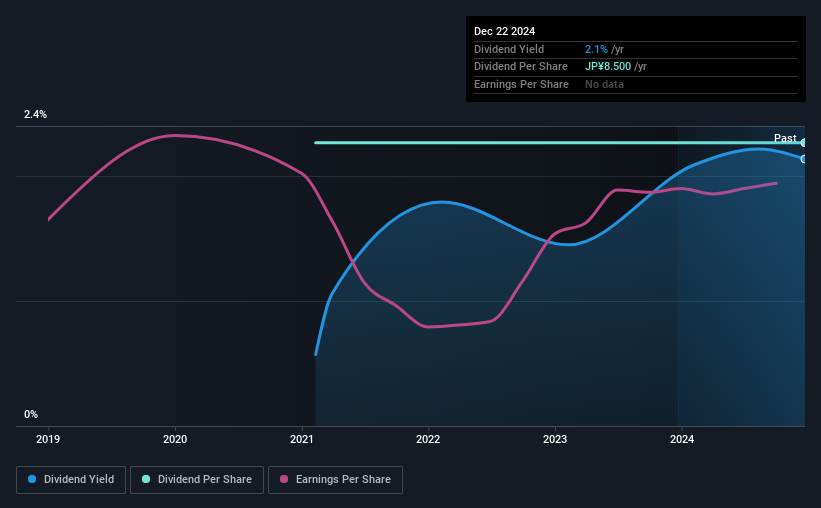

The company's next dividend payment will be JP¥8.50 per share, on the back of last year when the company paid a total of JP¥8.50 to shareholders. Based on the last year's worth of payments, KinjiroLtd stock has a trailing yield of around 2.1% on the current share price of JP¥398.00. We love seeing companies pay a dividend, but it's also important to be sure that laying the golden eggs isn't going to kill our golden goose! As a result, readers should always check whether KinjiroLtd has been able to grow its dividends, or if the dividend might be cut.

See our latest analysis for KinjiroLtd

Dividends are usually paid out of company profits, so if a company pays out more than it earned then its dividend is usually at greater risk of being cut. Fortunately KinjiroLtd's payout ratio is modest, at just 44% of profit. A useful secondary check can be to evaluate whether KinjiroLtd generated enough free cash flow to afford its dividend. The company paid out 109% of its free cash flow over the last year, which we think is outside the ideal range for most businesses. Cash flows are usually much more volatile than earnings, so this could be a temporary effect - but we'd generally want to look more closely here.

KinjiroLtd does have a large net cash position on the balance sheet, which could fund large dividends for a time, if the company so chose. Still, smart investors know that it is better to assess dividends relative to the cash and profit generated by the business. Paying dividends out of cash on the balance sheet is not long-term sustainable.

While KinjiroLtd's dividends were covered by the company's reported profits, cash is somewhat more important, so it's not great to see that the company didn't generate enough cash to pay its dividend. Cash is king, as they say, and were KinjiroLtd to repeatedly pay dividends that aren't well covered by cashflow, we would consider this a warning sign.

Click here to see how much of its profit KinjiroLtd paid out over the last 12 months.

Have Earnings And Dividends Been Growing?

Companies with consistently growing earnings per share generally make the best dividend stocks, as they usually find it easier to grow dividends per share. If earnings fall far enough, the company could be forced to cut its dividend. With that in mind, we're encouraged by the steady growth at KinjiroLtd, with earnings per share up 3.2% on average over the last five years. Earnings have been growing somewhat, but we're concerned dividend payments consumed most of the company's cash flow over the past year.

Another key way to measure a company's dividend prospects is by measuring its historical rate of dividend growth. KinjiroLtd's dividend payments are broadly unchanged compared to where they were four years ago.

The Bottom Line

Has KinjiroLtd got what it takes to maintain its dividend payments? KinjiroLtd has seen its earnings per share grow steadily and paid out less than half its profit over the last year. Unfortunately, its dividend was not well covered by free cash flow. All things considered, we are not particularly enthused about KinjiroLtd from a dividend perspective.

If you want to look further into KinjiroLtd, it's worth knowing the risks this business faces. For example - KinjiroLtd has 2 warning signs we think you should be aware of.

Generally, we wouldn't recommend just buying the first dividend stock you see. Here's a curated list of interesting stocks that are strong dividend payers.

Valuation is complex, but we're here to simplify it.

Discover if KinjiroLtd might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About TSE:4013

Solid track record with excellent balance sheet.

Market Insights

Advertisement

Community Narratives

For the Emperor: Why Games Workshop Could Be a Star Investment

Fair Value UK£160.00|0.4% overvalued

RO

Community Contributor

Securitas will boost margins with AI and tech-driven services

Fair Value SEK 260.91|44.5% undervalued

UN

Community Contributor

A Leader in EV Charging with Growth Potential

Fair Value €27.00|17.8% undervalued

TI

Community Contributor