3 Top Growth Companies With High Insider Ownership On Japanese Exchanges

Reviewed by Simply Wall St

Japan's stock markets have recently shown strong performance, with the Nikkei 225 Index rising by 5.6% and the broader TOPIX Index up by 3.7%, buoyed by dovish commentary from the Bank of Japan and optimism around China's stimulus measures. This favorable economic backdrop makes it an opportune time to explore growth companies with high insider ownership on Japanese exchanges. In today's market, stocks that combine robust growth potential with significant insider ownership can be particularly appealing, as they often indicate strong confidence from those closest to the company's operations and future prospects.

Top 10 Growth Companies With High Insider Ownership In Japan

| Name | Insider Ownership | Earnings Growth |

| Micronics Japan (TSE:6871) | 15.3% | 31.5% |

| Hottolink (TSE:3680) | 27% | 61.5% |

| Kasumigaseki CapitalLtd (TSE:3498) | 34.7% | 43.5% |

| Medley (TSE:4480) | 34% | 30.4% |

| Kanamic NetworkLTD (TSE:3939) | 25% | 28.3% |

| ExaWizards (TSE:4259) | 22% | 75.2% |

| Money Forward (TSE:3994) | 21.4% | 68.1% |

| AeroEdge (TSE:7409) | 10.7% | 25.3% |

| Soracom (TSE:147A) | 16.5% | 54.1% |

| freee K.K (TSE:4478) | 23.9% | 74.1% |

We'll examine a selection from our screener results.

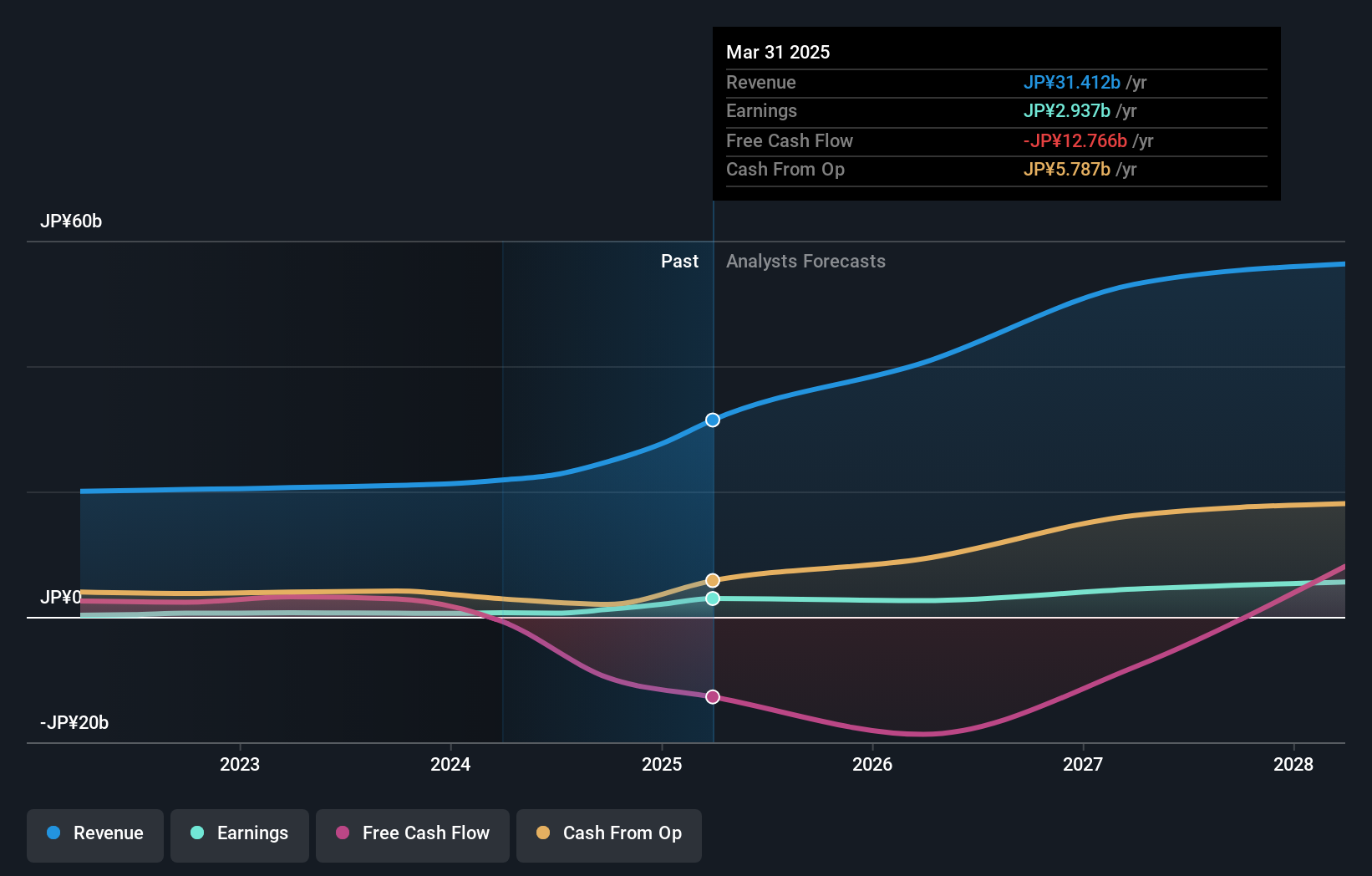

SAKURA Internet (TSE:3778)

Simply Wall St Growth Rating: ★★★★★☆

Overview: SAKURA Internet Inc. provides cloud computing services in Japan and has a market cap of ¥179.11 billion.

Operations: The company's revenue segment includes the Internet Infrastructure Business, which generated ¥22.66 billion.

Insider Ownership: 18.2%

Return On Equity Forecast: N/A (2027 estimate)

SAKURA Internet, a growth company with high insider ownership, is forecast to see revenue grow at 33.9% annually, outpacing the JP market's 4.3%. Earnings are expected to rise significantly at 55.63% per year over the next three years. Despite recent volatility and past shareholder dilution, SAKURA's robust growth prospects are underscored by its guidance for FY2025: JPY 28 billion in net sales and JPY 2 billion in operating profit.

- Click to explore a detailed breakdown of our findings in SAKURA Internet's earnings growth report.

- Our valuation report here indicates SAKURA Internet may be overvalued.

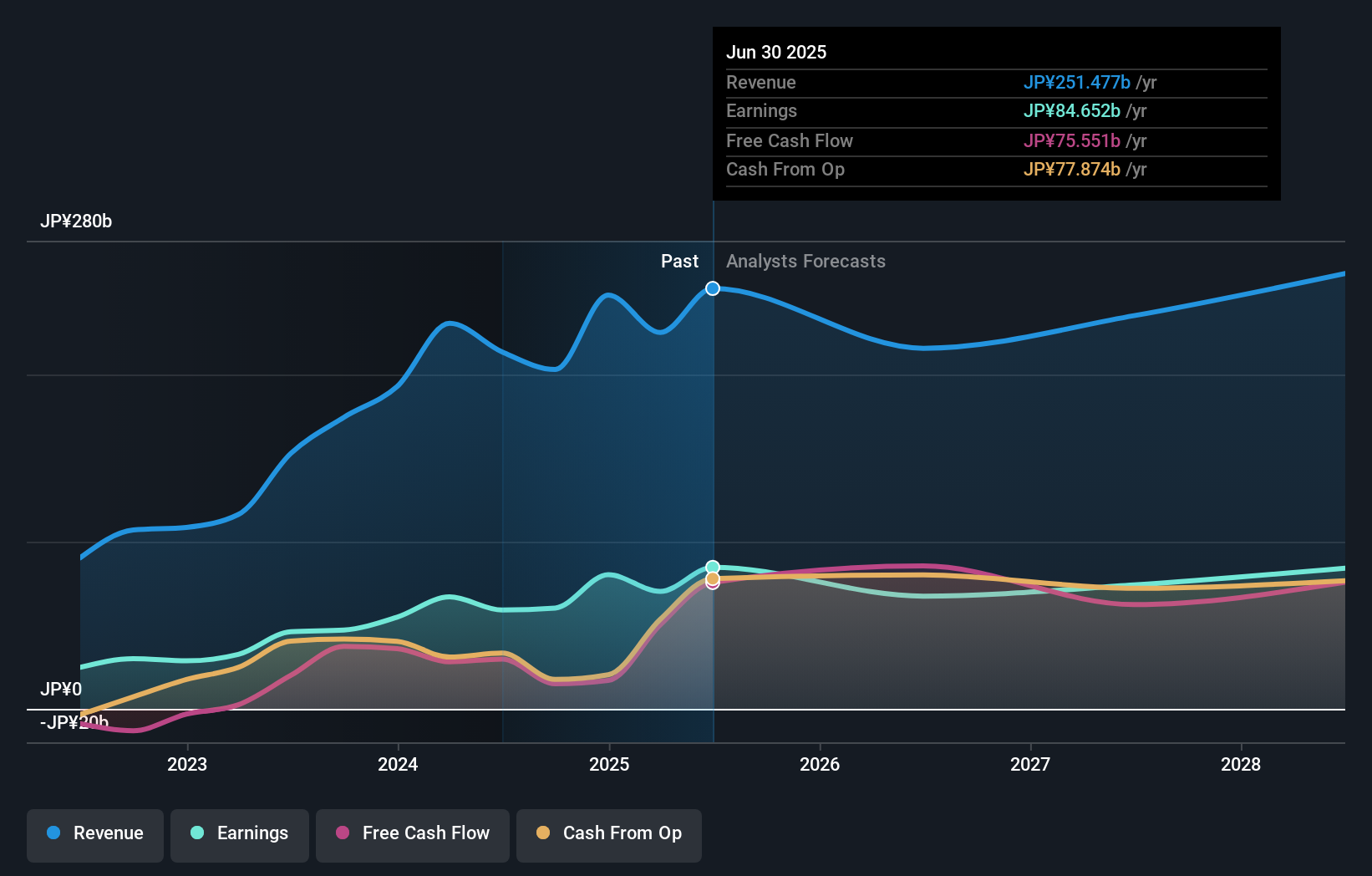

Money Forward (TSE:3994)

Simply Wall St Growth Rating: ★★★★★★

Overview: Money Forward, Inc. offers financial solutions for individuals, financial institutions, and corporations primarily in Japan and has a market cap of approximately ¥325.95 billion.

Operations: The Platform Services Business segment of Money Forward, Inc. generates ¥36.16 billion in revenue.

Insider Ownership: 21.4%

Return On Equity Forecast: 21% (2027 estimate)

Money Forward is expected to become profitable within three years, with earnings forecasted to grow 68.12% annually and revenue at 20.7% per year, significantly outpacing the market. Recent board meetings focused on strategic partnerships and restructuring initiatives, including a potential joint venture with Sumitomo Mitsui Card Company and transferring fintech-related business rights. Trading at 49.6% below estimated fair value, Money Forward's high insider ownership aligns with its strong growth outlook despite no substantial recent insider trading activity.

- Click here to discover the nuances of Money Forward with our detailed analytical future growth report.

- Our comprehensive valuation report raises the possibility that Money Forward is priced higher than what may be justified by its financials.

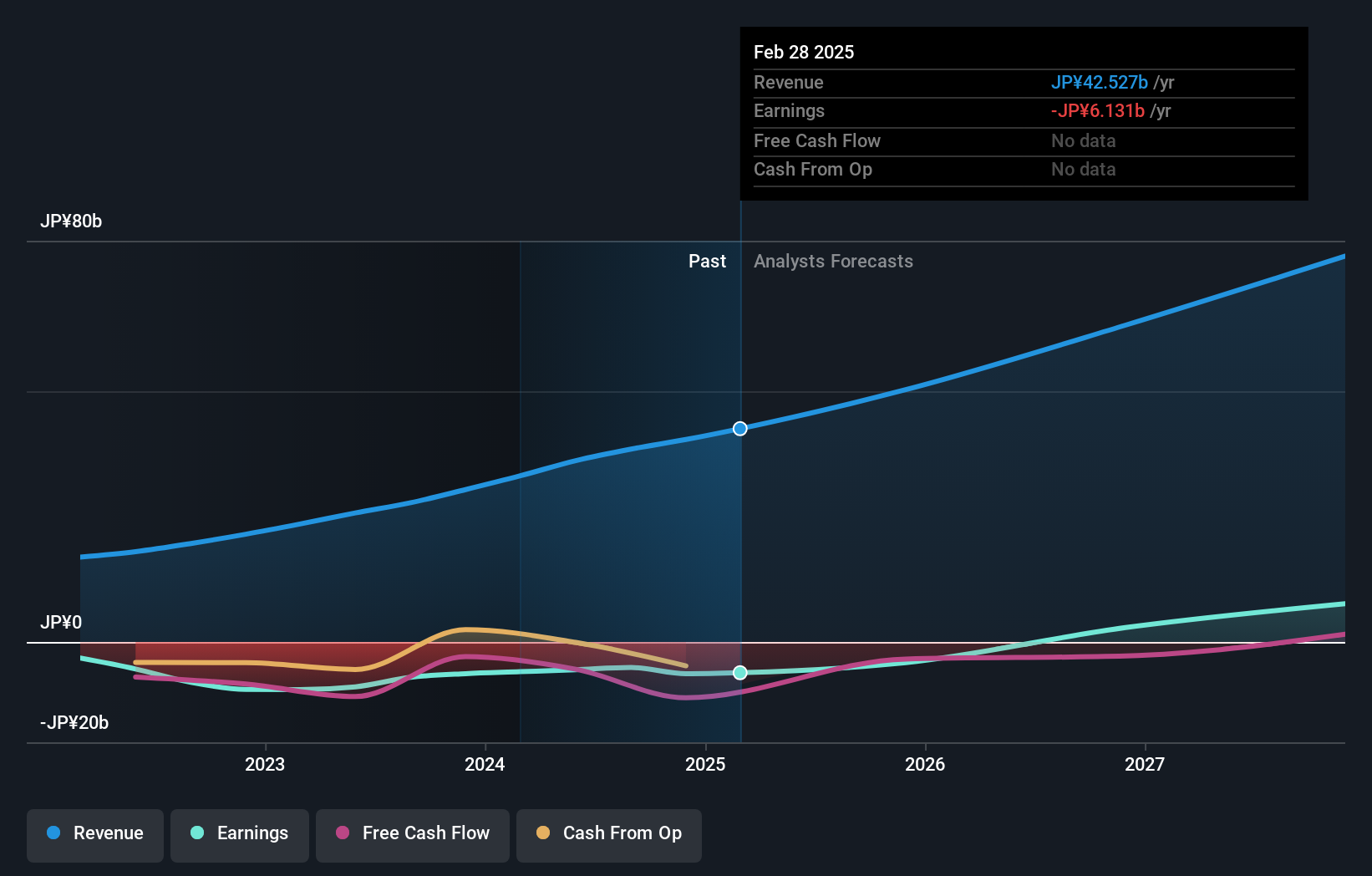

Lasertec (TSE:6920)

Simply Wall St Growth Rating: ★★★★☆☆

Overview: Lasertec Corporation designs, manufactures, and sells inspection and measurement equipment both in Japan and internationally, with a market cap of ¥2.37 trillion.

Operations: The company's primary revenue segment, generating ¥213.51 billion, is from the design, manufacture, and sale of inspection and measurement equipment.

Insider Ownership: 11.8%

Return On Equity Forecast: 41% (2027 estimate)

Lasertec's earnings are forecast to grow 15.9% annually, outpacing the Japanese market. Despite high volatility in its share price, Lasertec has shown strong profit growth of 28% over the past year. The company recently launched SICA108, enhancing SiC wafer inspection capabilities and maintaining its technological edge. With no substantial insider trading activity reported recently, high insider ownership aligns with Lasertec's promising growth trajectory and robust return on equity projections (41.4%).

- Click here and access our complete growth analysis report to understand the dynamics of Lasertec.

- The valuation report we've compiled suggests that Lasertec's current price could be inflated.

Seize The Opportunity

- Take a closer look at our Fast Growing Japanese Companies With High Insider Ownership list of 102 companies by clicking here.

- Got skin in the game with these stocks? Elevate how you manage them by using Simply Wall St's portfolio, where intuitive tools await to help optimize your investment outcomes.

- Simply Wall St is your key to unlocking global market trends, a free user-friendly app for forward-thinking investors.

Searching for a Fresh Perspective?

- Explore high-performing small cap companies that haven't yet garnered significant analyst attention.

- Diversify your portfolio with solid dividend payers offering reliable income streams to weather potential market turbulence.

- Find companies with promising cash flow potential yet trading below their fair value.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.The analysis only considers stock directly held by insiders. It does not include indirectly owned stock through other vehicles such as corporate and/or trust entities. All forecast revenue and earnings growth rates quoted are in terms of annualised (per annum) growth rates over 1-3 years.

New: Manage All Your Stock Portfolios in One Place

We've created the ultimate portfolio companion for stock investors, and it's free.

• Connect an unlimited number of Portfolios and see your total in one currency

• Be alerted to new Warning Signs or Risks via email or mobile

• Track the Fair Value of your stocks

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About TSE:3778

Flawless balance sheet with high growth potential.