Advertisement

- Japan

- /

- Semiconductors

- /

- TSE:8035

Tokyo Electron Limited Beat Analyst Estimates: See What The Consensus Is Forecasting For This Year

Tokyo Electron Limited (TSE:8035) shareholders are probably feeling a little disappointed, since its shares fell 4.5% to JP¥22,010 in the week after its latest interim results. It looks like a credible result overall - although revenues of JP¥1.1t were in line with what the analysts predicted, Tokyo Electron surprised by delivering a statutory profit of JP¥529 per share, a notable 17% above expectations. Following the result, the analysts have updated their earnings model, and it would be good to know whether they think there's been a strong change in the company's prospects, or if it's business as usual. So we gathered the latest post-earnings forecasts to see what estimates suggest is in store for next year.

View our latest analysis for Tokyo Electron

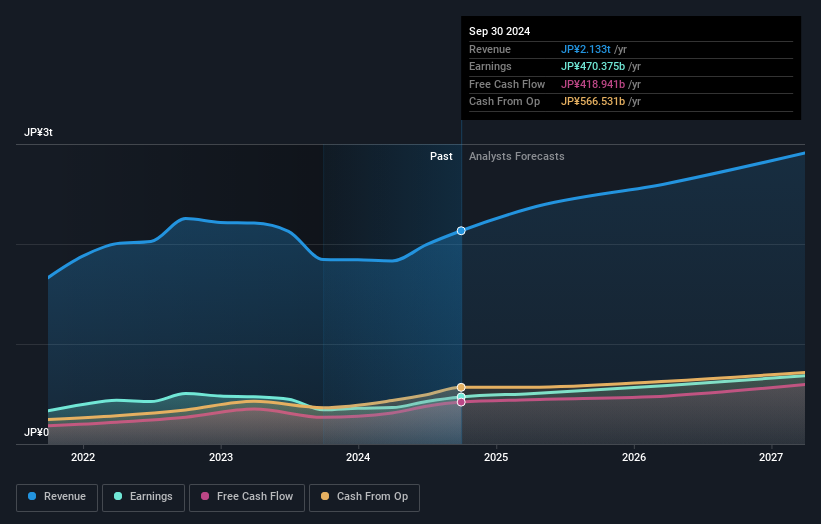

After the latest results, the 18 analysts covering Tokyo Electron are now predicting revenues of JP¥2.36t in 2025. If met, this would reflect a decent 11% improvement in revenue compared to the last 12 months. Statutory earnings per share are predicted to rise 6.9% to JP¥1,091. In the lead-up to this report, the analysts had been modelling revenues of JP¥2.31t and earnings per share (EPS) of JP¥1,045 in 2025. So there seems to have been a moderate uplift in sentiment following the latest results, given the upgrades to both revenue and earnings per share forecasts for next year.

Despite these upgrades,the analysts have not made any major changes to their price target of JP¥33,994, suggesting that the higher estimates are not likely to have a long term impact on what the stock is worth. That's not the only conclusion we can draw from this data however, as some investors also like to consider the spread in estimates when evaluating analyst price targets. Currently, the most bullish analyst values Tokyo Electron at JP¥41,000 per share, while the most bearish prices it at JP¥24,300. Analysts definitely have varying views on the business, but the spread of estimates is not wide enough in our view to suggest that extreme outcomes could await Tokyo Electron shareholders.

Looking at the bigger picture now, one of the ways we can make sense of these forecasts is to see how they measure up against both past performance and industry growth estimates. It's clear from the latest estimates that Tokyo Electron's rate of growth is expected to accelerate meaningfully, with the forecast 22% annualised revenue growth to the end of 2025 noticeably faster than its historical growth of 13% p.a. over the past five years. By contrast, our data suggests that other companies (with analyst coverage) in a similar industry are forecast to grow their revenue at 10% per year. Factoring in the forecast acceleration in revenue, it's pretty clear that Tokyo Electron is expected to grow much faster than its industry.

The Bottom Line

The biggest takeaway for us is the consensus earnings per share upgrade, which suggests a clear improvement in sentiment around Tokyo Electron's earnings potential next year. Pleasantly, they also upgraded their revenue estimates, and their forecasts suggest the business is expected to grow faster than the wider industry. There was no real change to the consensus price target, suggesting that the intrinsic value of the business has not undergone any major changes with the latest estimates.

With that said, the long-term trajectory of the company's earnings is a lot more important than next year. We have forecasts for Tokyo Electron going out to 2027, and you can see them free on our platform here.

We don't want to rain on the parade too much, but we did also find 2 warning signs for Tokyo Electron that you need to be mindful of.

Valuation is complex, but we're here to simplify it.

Discover if Tokyo Electron might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About TSE:8035

Tokyo Electron

Develops, manufactures, and sells semiconductor production equipment in Japan, Europe, North America, Taiwan, China, South Korea, and internationally.

Outstanding track record with flawless balance sheet.

Similar Companies

Market Insights

Advertisement

Community Narratives

The Next Phase of Energy Storage: How NeoVolta Is Tackling America’s Power Crunch

Fair Value US$7.50|35.1% undervalued

MA

Community Contributor

Why EnSilica is Worth Possibly 13x its Current Price

Fair Value UK£5.00|89.8% undervalued

DO

Community Contributor

M&A Activity, Industry Diversification & A Defense Contract Monopoly Will Push BWXT For Healthy Long-Term Growth

Fair Value US$220.00|15.2% undervalued

CL

Community Contributor

A case for Cassiar Gold Corp (TSXV: GLDC) to reach CAD$8-10 before 2030 (X30-37)

Fair Value CA$10.00|96.0% undervalued

AG

Community Contributor