- Japan

- /

- Semiconductors

- /

- TSE:6525

Kokusai Electric (TSE:6525) Eyes DRAM Growth with Generative AI and Advanced Packaging Expansion

Reviewed by Simply Wall St

Kokusai Electric (TSE:6525) has recently reported a remarkable 47% increase in revenue, driven by strong sales in DRAM and logic/foundry equipment, as highlighted by CFO Yoshitaka Kawakami. The company's strategic investments in R&D, including the new Tonami plant, position it well for future growth, particularly in the burgeoning generative AI sector. This report delves into key areas such as financial performance, strategic challenges, growth opportunities in advanced packaging, and external risks like regulatory issues in China.

Take a closer look at Kokusai Electric's potential here.

Innovative Factors Supporting Kokusai Electric

In the latest earnings call, Yoshitaka Kawakami, Managing Executive Officer and CFO, highlighted Kokusai Electric's impressive revenue growth and profitability. The company reported a 47% increase in overall revenue from equipment and services, driven by strong sales in DRAM and logic/foundry equipment. This growth is bolstered by the rising demand for DRAM equipment, particularly in the context of generative AI advancements. Furthermore, Kokusai Electric's strategic investments in R&D, including the completion of the Tonami plant, enhance its production capabilities and future growth prospects. The company is also forecasted to achieve earnings growth of 17.3% per year, significantly outpacing the JP market's growth of 7.9%. Additionally, a satisfactory net debt to equity ratio of 10.1% and a net profit margin improvement to 14.5% underscore its financial health.

Strategic Gaps That Could Affect Kokusai Electric

Kokusai Electric faces several challenges. The Price-To-Earnings Ratio of 18.8x is notably higher than the peer average of 14.1x, suggesting that the stock might be considered expensive relative to industry standards. Moreover, the company's Return on Equity at 17.3% falls short of the 20% benchmark, indicating room for improvement in efficiency. The recent initiation of dividend payments, with a yield of 1.4%, is lower than the top tier in the JP market, raising questions about their stability. Additionally, the company has experienced cash flow pressures due to share buybacks, potentially impacting short-term financial flexibility.

Growth Avenues Awaiting Kokusai Electric

The spread of generative AI presents significant growth opportunities for Kokusai Electric, particularly in the DRAM sector. The company is well-positioned to capitalize on this trend, as highlighted by Kawakami. Expansion into new business areas, such as advanced packaging, is also underway. Sales of equipment for interposers are expected to reach ¥10 billion by March 2025, doubling previous forecasts, as noted by President and CEO Fumiyuki Kanai. This expansion, coupled with a strong presence in China, offers substantial potential for increased market share and revenue growth.

External Factors Threatening Kokusai Electric

Regulatory risks in China pose a potential threat to Kokusai Electric's operations. Kanai emphasized the need for careful business planning to mitigate the impact of possible export restrictions. Additionally, intense market competition and economic uncertainties present challenges that the company must navigate to maintain its competitive edge. Supply chain disruptions are another concern, with the need to ensure resilience in areas like film deposition being critical for sustained growth. The company's share price volatility over the past three months also indicates market instability, which could lead to unexpected price movements.

Conclusion

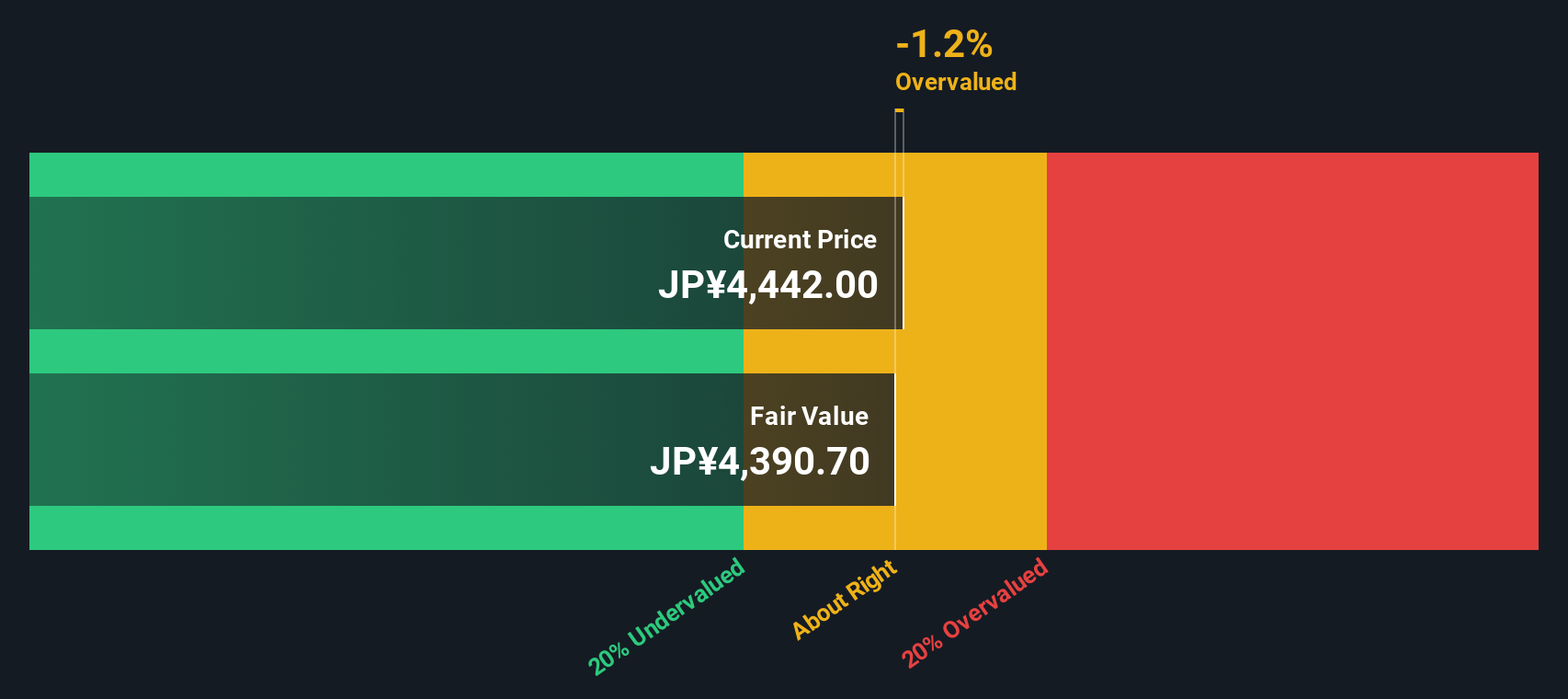

Kokusai Electric's impressive revenue growth of 47% and strategic investments in R&D position it well for future expansion, particularly in the DRAM sector driven by generative AI advancements. However, the company's Price-To-Earnings Ratio of 18.8x, while higher than industry peers, suggests a premium that reflects its strong growth potential and strategic market positioning, as supported by a favorable discounted cash flow analysis. Challenges such as cash flow pressures and regulatory risks in China remain, but Kokusai Electric's expansion into advanced packaging and its strong presence in China offer promising avenues for market share and revenue growth. The company's forecasted earnings growth of 17.3% per year, outpacing the JP market, underscores its potential for sustained financial performance, although efficiency improvements and strategic planning are crucial to navigate external threats and maintain competitive advantage.

Turning Ideas Into Actions

Curious About Other Options?

- Explore high-performing small cap companies that haven't yet garnered significant analyst attention.

- Fuel your portfolio with companies showing strong growth potential, backed by optimistic outlooks both from analysts and management.

- Find companies with promising cash flow potential yet trading below their fair value.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

```Valuation is complex, but we're here to simplify it.

Discover if Kokusai Electric might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About TSE:6525

Kokusai Electric

Engages in the development, manufacture, sale, repair, and maintenance of semiconductor manufacturing equipment worldwide.

Excellent balance sheet and fair value.

Market Insights

Community Narratives