Advertisement

- Japan

- /

- Semiconductors

- /

- TSE:6266

There's A Lot To Like About Tazmo's (TSE:6266) Upcoming JP¥30.00 Dividend

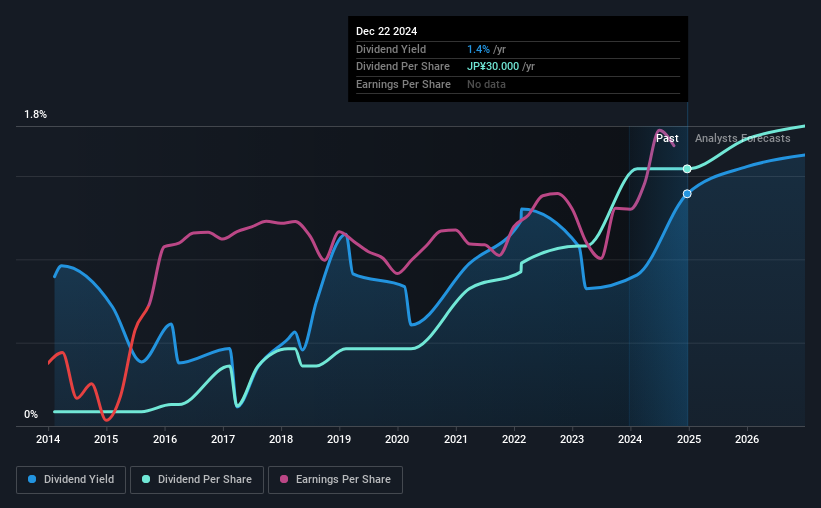

Readers hoping to buy Tazmo Co., Ltd. (TSE:6266) for its dividend will need to make their move shortly, as the stock is about to trade ex-dividend. The ex-dividend date is one business day before a company's record date, which is the date on which the company determines which shareholders are entitled to receive a dividend. The ex-dividend date is important as the process of settlement involves two full business days. So if you miss that date, you would not show up on the company's books on the record date. Accordingly, Tazmo investors that purchase the stock on or after the 27th of December will not receive the dividend, which will be paid on the 28th of March.

The company's next dividend payment will be JP¥30.00 per share, on the back of last year when the company paid a total of JP¥30.00 to shareholders. Based on the last year's worth of payments, Tazmo stock has a trailing yield of around 1.4% on the current share price of JP¥2153.00. Dividends are an important source of income to many shareholders, but the health of the business is crucial to maintaining those dividends. So we need to investigate whether Tazmo can afford its dividend, and if the dividend could grow.

See our latest analysis for Tazmo

If a company pays out more in dividends than it earned, then the dividend might become unsustainable - hardly an ideal situation. Tazmo is paying out just 9.0% of its profit after tax, which is comfortably low and leaves plenty of breathing room in the case of adverse events. Yet cash flows are even more important than profits for assessing a dividend, so we need to see if the company generated enough cash to pay its distribution. What's good is that dividends were well covered by free cash flow, with the company paying out 6.3% of its cash flow last year.

It's encouraging to see that the dividend is covered by both profit and cash flow. This generally suggests the dividend is sustainable, as long as earnings don't drop precipitously.

Click here to see the company's payout ratio, plus analyst estimates of its future dividends.

Have Earnings And Dividends Been Growing?

Stocks in companies that generate sustainable earnings growth often make the best dividend prospects, as it is easier to lift the dividend when earnings are rising. If business enters a downturn and the dividend is cut, the company could see its value fall precipitously. For this reason, we're glad to see Tazmo's earnings per share have risen 17% per annum over the last five years. Earnings per share have been growing rapidly and the company is retaining a majority of its earnings within the business. This will make it easier to fund future growth efforts and we think this is an attractive combination - plus the dividend can always be increased later.

Many investors will assess a company's dividend performance by evaluating how much the dividend payments have changed over time. Since the start of our data, 10 years ago, Tazmo has lifted its dividend by approximately 34% a year on average. Both per-share earnings and dividends have both been growing rapidly in recent times, which is great to see.

Final Takeaway

Is Tazmo worth buying for its dividend? We love that Tazmo is growing earnings per share while simultaneously paying out a low percentage of both its earnings and cash flow. These characteristics suggest the company is reinvesting in growing its business, while the conservative payout ratio also implies a reduced risk of the dividend being cut in the future. There's a lot to like about Tazmo, and we would prioritise taking a closer look at it.

While it's tempting to invest in Tazmo for the dividends alone, you should always be mindful of the risks involved. Our analysis shows 1 warning sign for Tazmo and you should be aware of it before buying any shares.

A common investing mistake is buying the first interesting stock you see. Here you can find a full list of high-yield dividend stocks.

Valuation is complex, but we're here to simplify it.

Discover if Tazmo might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About TSE:6266

Tazmo

Together with subsidiaries, develops, manufactures, and sells semiconductor manufacturing equipment in Japan, Taiwan, China, South Korea, Vietnam, rest of Asia, North America, and Europe.

Very undervalued with flawless balance sheet and pays a dividend.

Similar Companies

Market Insights

Advertisement

Weekly Picks

RO

RockeTeller on Santacruz Silver Mining ·

Crazy Undervalued 42 Baggers Silver Play (Active & Running Mine)

Fair Value:CA$8696.7% undervalued

59 followersusers have followed this narrative

7 commentsusers have commented on this narrative

17 likesusers have liked this narrative

RO

Robbo on Fiducian Group ·

Fiducian: Compliance Clouds or Value Opportunity?

Fair Value:AU$122.0% undervalued

9 followersusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

WO

woodworthfund on Willamette Valley Vineyards ·

Willamette Valley Vineyards (WVVI): Not-So-Great Value

Fair Value:US$242.5% overvalued

10 followersusers have followed this narrative

0 commentsusers have commented on this narrative

1 likeusers have liked this narrative

Recently Updated Narratives

WO

woodworthfund on MGP Ingredients ·

THE KINGDOM OF BROWN GOODS: WHY MGPI IS BEING CRUSHED BY INVENTORY & PRIMED FOR RESURRECTION

Fair Value:US$4035.8% undervalued

2 followersusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

DA

davidlsander on Beam Therapeutics ·

The "Molecular Pencil": Why Beam's Technology is Built to Win

Fair Value:US$15081.9% undervalued

50 followersusers have followed this narrative

3 commentsusers have commented on this narrative

1 likeusers have liked this narrative

MO

mo7md on ADNOC Gas ·

ADNOC Gas future shines with a 21.4% revenue surge

Fair Value:د.إ3.728.9% undervalued

3 followersusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

Popular Narratives

TH

TheWallstreetKing on MicroVision ·

MicroVision will explode future revenue by 380.37% with a vision towards success

Fair Value:US$6098.5% undervalued

117 followersusers have followed this narrative

11 commentsusers have commented on this narrative

22 likesusers have liked this narrative

AN

AnalystConsensusTarget on NVIDIA ·

NVDA: Expanding AI Demand Will Drive Major Data Center Investments Through 2026

Fair Value:US$250.3927.2% undervalued

959 followersusers have followed this narrative

6 commentsusers have commented on this narrative

25 likesusers have liked this narrative

RO

RockeTeller on Santacruz Silver Mining ·

Crazy Undervalued 42 Baggers Silver Play (Active & Running Mine)

Fair Value:CA$8696.7% undervalued

59 followersusers have followed this narrative

7 commentsusers have commented on this narrative

17 likesusers have liked this narrative