Advertisement

- Japan

- /

- Retail Distributors

- /

- TSE:8123

Investors Appear Satisfied With T.Kawabe & Co., Ltd.'s (TSE:8123) Prospects As Shares Rocket 41%

The T.Kawabe & Co., Ltd. (TSE:8123) share price has done very well over the last month, posting an excellent gain of 41%. Looking back a bit further, it's encouraging to see the stock is up 61% in the last year.

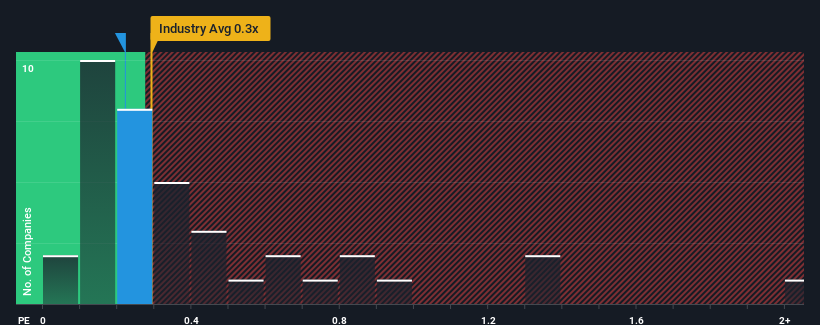

Although its price has surged higher, it's still not a stretch to say that T.Kawabe's price-to-sales (or "P/S") ratio of 0.2x right now seems quite "middle-of-the-road" compared to the Retail Distributors industry in Japan, where the median P/S ratio is around 0.3x. While this might not raise any eyebrows, if the P/S ratio is not justified investors could be missing out on a potential opportunity or ignoring looming disappointment.

View our latest analysis for T.Kawabe

How Has T.Kawabe Performed Recently?

T.Kawabe has been doing a decent job lately as it's been growing revenue at a reasonable pace. It might be that many expect the respectable revenue performance to only match most other companies over the coming period, which has kept the P/S from rising. If you like the company, you'd be hoping this isn't the case so that you could potentially pick up some stock while it's not quite in favour.

Although there are no analyst estimates available for T.Kawabe, take a look at this free data-rich visualisation to see how the company stacks up on earnings, revenue and cash flow.Is There Some Revenue Growth Forecasted For T.Kawabe?

The only time you'd be comfortable seeing a P/S like T.Kawabe's is when the company's growth is tracking the industry closely.

Retrospectively, the last year delivered a decent 6.7% gain to the company's revenues. The solid recent performance means it was also able to grow revenue by 10% in total over the last three years. Accordingly, shareholders would have probably been satisfied with the medium-term rates of revenue growth.

Weighing that recent medium-term revenue trajectory against the broader industry's one-year forecast for expansion of 3.0% shows it's about the same on an annualised basis.

In light of this, it's understandable that T.Kawabe's P/S sits in line with the majority of other companies. Apparently shareholders are comfortable to simply hold on assuming the company will continue keeping a low profile.

The Bottom Line On T.Kawabe's P/S

T.Kawabe's stock has a lot of momentum behind it lately, which has brought its P/S level with the rest of the industry. Typically, we'd caution against reading too much into price-to-sales ratios when settling on investment decisions, though it can reveal plenty about what other market participants think about the company.

As we've seen, T.Kawabe's three-year revenue trends seem to be contributing to its P/S, given they look similar to current industry expectations. Currently, with a past revenue trend that aligns closely wit the industry outlook, shareholders are confident the company's future revenue outlook won't contain any major surprises. Unless the recent medium-term conditions change, they will continue to support the share price at these levels.

We don't want to rain on the parade too much, but we did also find 3 warning signs for T.Kawabe (2 are concerning!) that you need to be mindful of.

If you're unsure about the strength of T.Kawabe's business, why not explore our interactive list of stocks with solid business fundamentals for some other companies you may have missed.

Valuation is complex, but we're here to simplify it.

Discover if T.Kawabe might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About TSE:8123

T.Kawabe

Manufactures, sells, imports, and exports handkerchiefs, scarves, mufflers, towels, and fabric products in Japan.

Solid track record with excellent balance sheet.

Market Insights

Advertisement

Community Narratives

BMW cruising ahead with new EVs and premium models to boost revenue 5%

Fair Value €135.07|44.5% undervalued

UN

Community Contributor

EU#2 - From Humble Beginnings to Global Powerhouse

Fair Value DKK 851.04|46.1% undervalued

TO

Community Contributor