Advertisement

Pan Pacific International Holdings (TSE:7532): Assessing Valuation Following Strong September 2025 Sales Growth

Simply Wall St

Reviewed by Simply Wall St

Pan Pacific International Holdings (TSE:7532) has just released its September 2025 sales figures, revealing year-over-year growth across domestic retail, discount store, and UNY business segments. These numbers point to continued demand and steady operational momentum.

See our latest analysis for Pan Pacific International Holdings.

After a strong stretch of sales growth, Pan Pacific International Holdings’ share price momentum has recently cooled. The 1-year total shareholder return of 26.6% still handily outpaces the market, and its longer term multi-year gains remain impressive. Investors seem to be absorbing the latest set of numbers while looking for signals of further upside or shifts in the company’s growth trajectory.

If Pan Pacific’s resilient growth caught your attention, now is an ideal moment to broaden your search and discover fast growing stocks with high insider ownership

With healthy sales growth and a recent dip in share price, is Pan Pacific International Holdings now trading at a discount? Or are markets already factoring in the company’s robust growth for the years ahead?

Price-to-Earnings of 31.1: Is it justified?

At a price-to-earnings (P/E) ratio of 31.1, Pan Pacific International Holdings is trading at a premium to both its peer group and industry averages. This is despite its robust sales figures and operational momentum. The last close price of ¥943.4 stands well above where sector valuation typically sits.

The price-to-earnings ratio measures how much investors are willing to pay for each yen of current earnings. For retailers, this metric reflects market confidence in future earnings resilience and growth potential.

For Pan Pacific, the current P/E not only exceeds the peer average of 20.2 but also significantly surpasses the JP Multiline Retail industry average of 16.7. Compared to the company’s own estimated fair P/E of 23.8, the market is demanding a sizable premium. Unless expectations for future earnings see a sizable uplift, there is a strong possibility the share price could ultimately trend toward the fair ratio level.

Explore the SWS fair ratio for Pan Pacific International Holdings

Result: Price-to-Earnings of 31.1 (OVERVALUED)

However, slowing momentum in quarterly returns and exposure to broader market shifts could quickly reshape the outlook for Pan Pacific International Holdings.

Find out about the key risks to this Pan Pacific International Holdings narrative.

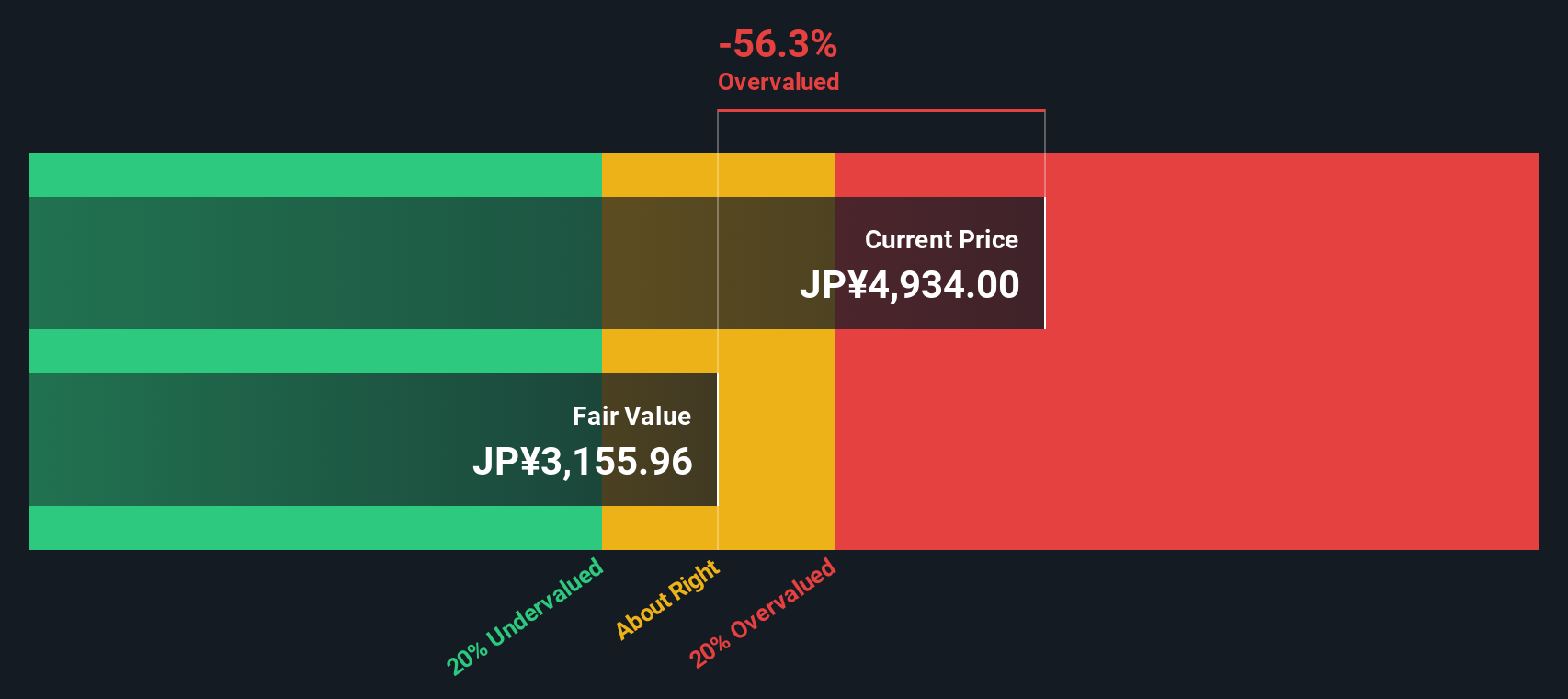

Another View: What Does Our DCF Model Say?

While multiples suggest Pan Pacific International Holdings is trading at a premium, our SWS DCF model offers a different perspective. The DCF estimate of fair value is ¥652.97, which is well below the current price of ¥943.4. This indicates the stock may be overvalued when judged by future cash flows. Which valuation lens will prove right in the long run?

Look into how the SWS DCF model arrives at its fair value.

Simply Wall St performs a discounted cash flow (DCF) on every stock in the world every day (check out Pan Pacific International Holdings for example). We show the entire calculation in full. You can track the result in your watchlist or portfolio and be alerted when this changes, or use our stock screener to discover undervalued stocks based on their cash flows. If you save a screener we even alert you when new companies match - so you never miss a potential opportunity.

Build Your Own Pan Pacific International Holdings Narrative

Don’t just take these conclusions at face value. If you’d rather dive into the numbers and shape your own perspective, it only takes a few minutes. Do it your way

A good starting point is our analysis highlighting 3 key rewards investors are optimistic about regarding Pan Pacific International Holdings.

Looking for More Investment Opportunities?

Don’t settle for just one perspective when you could be at the forefront of exciting market trends. Let yourself uncover strategies with real growth potential.

- Tap into under-the-radar growth by checking out these 3588 penny stocks with strong financials. Emerging opportunities here can create outsized results for bold investors.

- Capitalize on big trends in healthcare innovation through these 33 healthcare AI stocks and see which companies are fueling the future of medicine with AI breakthroughs.

- Unlock portfolio stability and steady returns by evaluating these 17 dividend stocks with yields > 3%. This curated group features high-yield stocks designed for consistent income.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

New: Manage All Your Stock Portfolios in One Place

We've created the ultimate portfolio companion for stock investors, and it's free.

• Connect an unlimited number of Portfolios and see your total in one currency

• Be alerted to new Warning Signs or Risks via email or mobile

• Track the Fair Value of your stocks

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About TSE:7532

Flawless balance sheet with moderate growth potential.

Similar Companies

Market Insights

Advertisement

Community Narratives

Finding The True Value Of A Logistics Powerhouse

Fair Value US$95.21|7.5% undervalued

NV

Community Contributor

Paradigm Biopharmaceuticals Will Lead Osteoarthritis Treatment with Zilosul's FDA Success

Fair Value AU$5.50|93.3% undervalued

AM

Community Contributor

Barrick Mining (ABX:CA): A Gold Hedge against a U.S. Shutdown

Fair Value CA$60.00|26.4% undervalued

GM

Community Contributor