Stock Analysis

- Japan

- /

- Specialty Stores

- /

- TSE:3186

Analyzing 3 Japanese Exchange Growth Companies With High Insider Ownership And Up To 83% Earnings Growth

Reviewed by Simply Wall St

As global markets navigate through a period of fluctuating inflation and interest rates, the Japanese stock market has recently experienced a retreat from record highs, influenced by currency interventions aimed at supporting the yen. This backdrop sets an intriguing stage for investors looking at growth companies in Japan, particularly those with high insider ownership which can signal strong confidence in the company’s future from those who know it best.

Top 10 Growth Companies With High Insider Ownership In Japan

| Name | Insider Ownership | Earnings Growth |

| Hottolink (TSE:3680) | 27% | 59.7% |

| Kasumigaseki CapitalLtd (TSE:3498) | 34.8% | 42.9% |

| Medley (TSE:4480) | 34% | 28.7% |

| Micronics Japan (TSE:6871) | 15.3% | 39.8% |

| Kanamic NetworkLTD (TSE:3939) | 25% | 28.9% |

| SHIFT (TSE:3697) | 35.4% | 32.5% |

| ExaWizards (TSE:4259) | 21.9% | 91.1% |

| Money Forward (TSE:3994) | 21.4% | 66.9% |

| Astroscale Holdings (TSE:186A) | 20.9% | 90% |

| freee K.K (TSE:4478) | 23.9% | 72.9% |

Let's review some notable picks from our screened stocks.

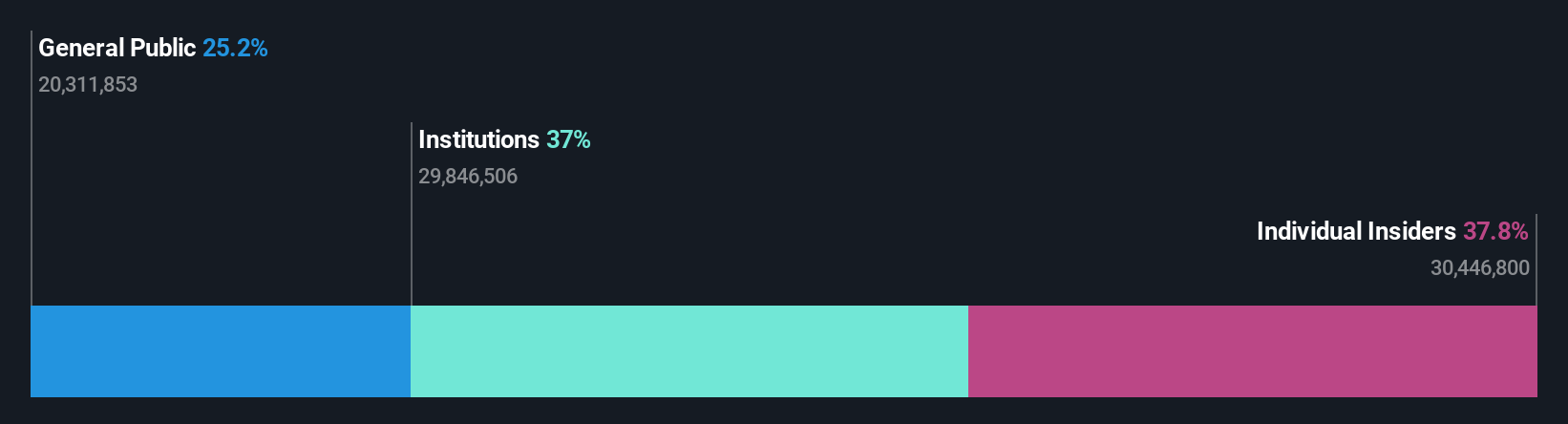

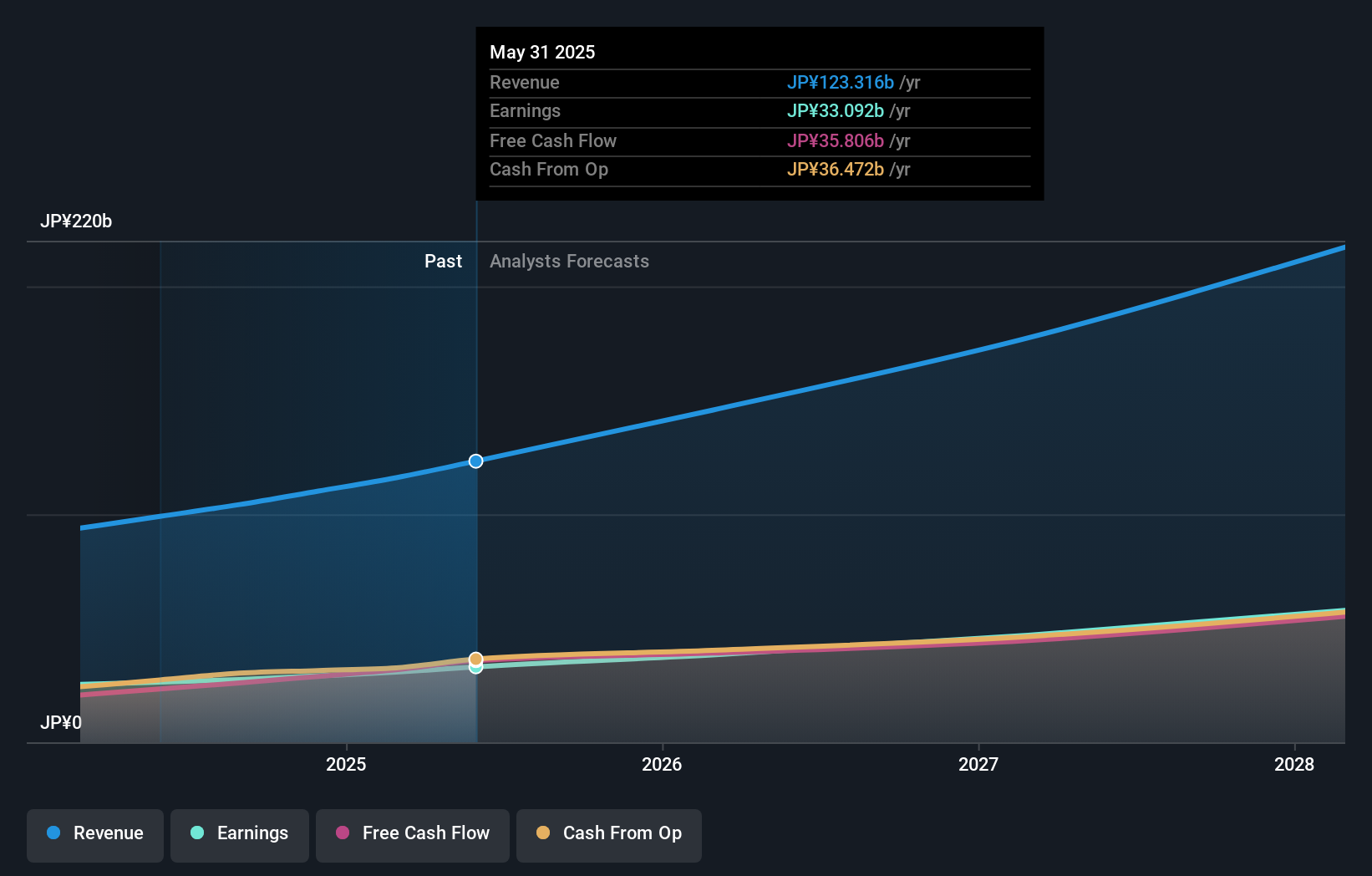

NEXTAGE (TSE:3186)

Simply Wall St Growth Rating: ★★★★☆☆

Overview: NEXTAGE Co., Ltd. is a company based in Japan that specializes in the sale of new and used cars, with a market capitalization of approximately ¥169.02 billion.

Operations: The firm operates primarily in the automotive sector, focusing on the sales of new and used vehicles within Japan.

Insider Ownership: 38.3%

Earnings Growth Forecast: 19.1% p.a.

NEXTAGE Co., Ltd. recently projected significant financial growth for the fiscal year ending November 2024, with expectations of JPY 545 billion in net sales and a JPY 20 billion operating profit. Despite this optimistic outlook, the company's debt is poorly covered by its operating cash flow, and its share price has been highly volatile recently. While NEXTAGE's earnings and revenue are forecasted to grow faster than the Japanese market average—19.1% and 11.2% per year respectively—the rates are below significant growth benchmarks. Additionally, there is no recent substantial insider buying or selling reported, which might affect investor confidence in terms of insider ownership dynamics.

- Click here and access our complete growth analysis report to understand the dynamics of NEXTAGE.

- The valuation report we've compiled suggests that NEXTAGE's current price could be inflated.

Rakuten Group (TSE:4755)

Simply Wall St Growth Rating: ★★★★☆☆

Overview: Rakuten Group, Inc. operates in e-commerce, fintech, digital content, and communications sectors globally, with a market capitalization of approximately ¥1.95 trillion.

Operations: The company generates revenue through its diverse operations in online retail, financial services, digital media, and telecommunications.

Insider Ownership: 17.3%

Earnings Growth Forecast: 83.1% p.a.

Rakuten Group, Inc. is poised for notable revenue expansion, with forecasts predicting a double-digit increase in 2024, excluding its securities segment. Despite trading at 78.1% below its estimated fair value and anticipated profitability within three years, growth in annual profit is expected to surpass average market trends significantly. However, its projected return on equity of 8.9% suggests modest future efficiency in capital utilization compared to some peers. Insider trading activity has remained static recently, indicating stable insider confidence.

- Take a closer look at Rakuten Group's potential here in our earnings growth report.

- Our valuation report unveils the possibility Rakuten Group's shares may be trading at a discount.

BayCurrent Consulting (TSE:6532)

Simply Wall St Growth Rating: ★★★★☆☆

Overview: BayCurrent Consulting, Inc. offers consulting services in Japan and has a market capitalization of approximately ¥659.53 billion.

Operations: The firm operates primarily in the consulting sector within Japan.

Insider Ownership: 13.9%

Earnings Growth Forecast: 18.7% p.a.

BayCurrent Consulting has demonstrated robust growth, with earnings expected to rise by 18.7% annually. Although its revenue growth of 18.2% per year is below the significant 20% threshold, it still outpaces the Japanese market average of 4.4%. The company's return on equity is projected to be a high 34.7% in three years, signaling strong future profitability. Recently, BayCurrent completed a share buyback program for ¥3.6 billion, underscoring its commitment to shareholder value despite a highly volatile share price in recent months.

- Get an in-depth perspective on BayCurrent Consulting's performance by reading our analyst estimates report here.

- Our valuation report here indicates BayCurrent Consulting may be undervalued.

Summing It All Up

- Embark on your investment journey to our 96 Fast Growing Japanese Companies With High Insider Ownership selection here.

- Are these companies part of your investment strategy? Use Simply Wall St to consolidate your holdings into a portfolio and gain insights with our comprehensive analysis tools.

- Discover a world of investment opportunities with Simply Wall St's free app and access unparalleled stock analysis across all markets.

Curious About Other Options?

- Explore high-performing small cap companies that haven't yet garnered significant analyst attention.

- Diversify your portfolio with solid dividend payers offering reliable income streams to weather potential market turbulence.

- Find companies with promising cash flow potential yet trading below their fair value.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.The analysis only considers stock directly held by insiders. It does not include indirectly owned stock through other vehicles such as corporate and/or trust entities. All forecast revenue and earnings growth rates quoted are in terms of annualised (per annum) growth rates over 1-3 years.

Valuation is complex, but we're helping make it simple.

Find out whether NEXTAGE is potentially over or undervalued by checking out our comprehensive analysis, which includes fair value estimates, risks and warnings, dividends, insider transactions and financial health.

View the Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About TSE:3186

Reasonable growth potential with mediocre balance sheet.