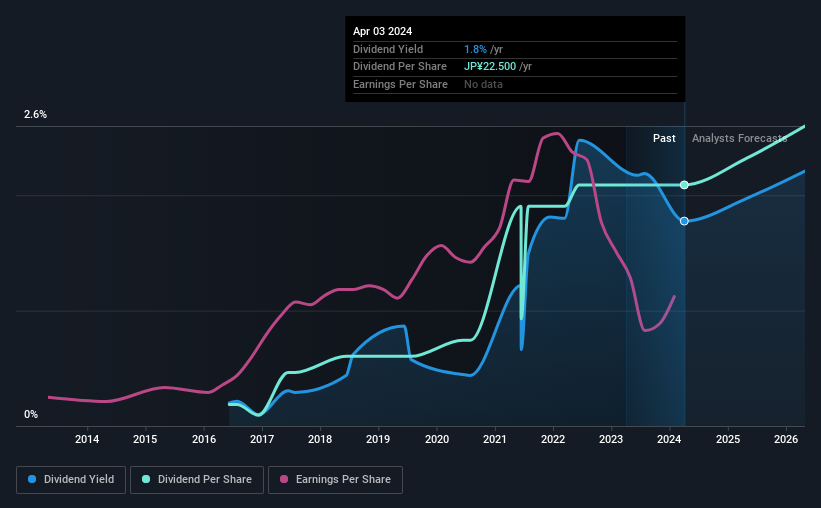

Hamee Corp.'s (TSE:3134) investors are due to receive a payment of ¥22.50 per share on 28th of July. The dividend yield will be 1.8% based on this payment which is still above the industry average.

Check out our latest analysis for Hamee

Hamee's Dividend Is Well Covered By Earnings

We like to see robust dividend yields, but that doesn't matter if the payment isn't sustainable. The last payment was quite easily covered by earnings, but it made up 505% of cash flows. The company might be more focused on returning cash to shareholders, but paying out this much of its cash flow could expose the dividend to being cut in the future.

The next year is set to see EPS grow by 30.3%. If the dividend continues on this path, the payout ratio could be 43% by next year, which we think can be pretty sustainable going forward.

Hamee's Dividend Has Lacked Consistency

Even in its relatively short history, the company has reduced the dividend at least once. Due to this, we are a little bit cautious about the dividend consistency over a full economic cycle. The dividend has gone from an annual total of ¥2.00 in 2016 to the most recent total annual payment of ¥22.50. This works out to be a compound annual growth rate (CAGR) of approximately 35% a year over that time. Hamee has grown distributions at a rapid rate despite cutting the dividend at least once in the past. Companies that cut once often cut again, so we would be cautious about buying this stock solely for the dividend income.

The Dividend's Growth Prospects Are Limited

With a relatively unstable dividend, it's even more important to see if earnings per share is growing. Hamee hasn't seen much change in its earnings per share over the last five years.

Hamee's Dividend Doesn't Look Sustainable

In summary, while it's good to see that the dividend hasn't been cut, we are a bit cautious about Hamee's payments, as there could be some issues with sustaining them into the future. With cash flows lacking, it is difficult to see how the company can sustain a dividend payment. Overall, we don't think this company has the makings of a good income stock.

It's important to note that companies having a consistent dividend policy will generate greater investor confidence than those having an erratic one. At the same time, there are other factors our readers should be conscious of before pouring capital into a stock. As an example, we've identified 3 warning signs for Hamee that you should be aware of before investing. Looking for more high-yielding dividend ideas? Try our collection of strong dividend payers.

If you're looking to trade Hamee, open an account with the lowest-cost platform trusted by professionals, Interactive Brokers.

With clients in over 200 countries and territories, and access to 160 markets, IBKR lets you trade stocks, options, futures, forex, bonds and funds from a single integrated account.

Enjoy no hidden fees, no account minimums, and FX conversion rates as low as 0.03%, far better than what most brokers offer.

Sponsored ContentValuation is complex, but we're here to simplify it.

Discover if Hamee might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About TSE:3134

Hamee

Engages in the e-commerce and platform businesses in Japan, rest of Asia, North America, and internationally.

Undervalued with proven track record.

Market Insights

Community Narratives