- Japan

- /

- Specialty Stores

- /

- TSE:3134

Hamee Corp. (TSE:3134) Stocks Shoot Up 26% But Its P/E Still Looks Reasonable

Hamee Corp. (TSE:3134) shares have continued their recent momentum with a 26% gain in the last month alone. The last 30 days bring the annual gain to a very sharp 39%.

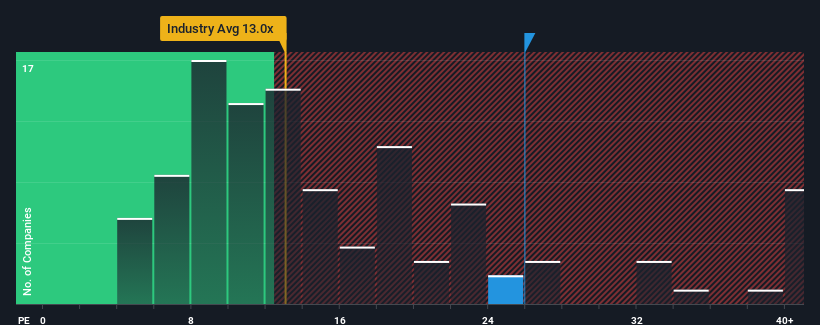

Since its price has surged higher, Hamee may be sending very bearish signals at the moment with a price-to-earnings (or "P/E") ratio of 26x, since almost half of all companies in Japan have P/E ratios under 14x and even P/E's lower than 10x are not unusual. However, the P/E might be quite high for a reason and it requires further investigation to determine if it's justified.

Hamee hasn't been tracking well recently as its declining earnings compare poorly to other companies, which have seen some growth on average. One possibility is that the P/E is high because investors think this poor earnings performance will turn the corner. You'd really hope so, otherwise you're paying a pretty hefty price for no particular reason.

See our latest analysis for Hamee

How Is Hamee's Growth Trending?

The only time you'd be truly comfortable seeing a P/E as steep as Hamee's is when the company's growth is on track to outshine the market decidedly.

Retrospectively, the last year delivered a frustrating 26% decrease to the company's bottom line. As a result, earnings from three years ago have also fallen 35% overall. So unfortunately, we have to acknowledge that the company has not done a great job of growing earnings over that time.

Looking ahead now, EPS is anticipated to climb by 87% during the coming year according to the sole analyst following the company. With the market only predicted to deliver 11%, the company is positioned for a stronger earnings result.

In light of this, it's understandable that Hamee's P/E sits above the majority of other companies. It seems most investors are expecting this strong future growth and are willing to pay more for the stock.

The Bottom Line On Hamee's P/E

Shares in Hamee have built up some good momentum lately, which has really inflated its P/E. Typically, we'd caution against reading too much into price-to-earnings ratios when settling on investment decisions, though it can reveal plenty about what other market participants think about the company.

As we suspected, our examination of Hamee's analyst forecasts revealed that its superior earnings outlook is contributing to its high P/E. At this stage investors feel the potential for a deterioration in earnings isn't great enough to justify a lower P/E ratio. It's hard to see the share price falling strongly in the near future under these circumstances.

Having said that, be aware Hamee is showing 3 warning signs in our investment analysis, you should know about.

You might be able to find a better investment than Hamee. If you want a selection of possible candidates, check out this free list of interesting companies that trade on a low P/E (but have proven they can grow earnings).

If you're looking to trade Hamee, open an account with the lowest-cost platform trusted by professionals, Interactive Brokers.

With clients in over 200 countries and territories, and access to 160 markets, IBKR lets you trade stocks, options, futures, forex, bonds and funds from a single integrated account.

Enjoy no hidden fees, no account minimums, and FX conversion rates as low as 0.03%, far better than what most brokers offer.

Sponsored ContentValuation is complex, but we're here to simplify it.

Discover if Hamee might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About TSE:3134

Hamee

Engages in the e-commerce and platform businesses in Japan, rest of Asia, North America, and internationally.

Undervalued with proven track record.

Market Insights

Community Narratives