What are the early trends we should look for to identify a stock that could multiply in value over the long term? Typically, we'll want to notice a trend of growing return on capital employed (ROCE) and alongside that, an expanding base of capital employed. Put simply, these types of businesses are compounding machines, meaning they are continually reinvesting their earnings at ever-higher rates of return. So on that note, Art Vivant (TYO:7523) looks quite promising in regards to its trends of return on capital.

What is Return On Capital Employed (ROCE)?

Just to clarify if you're unsure, ROCE is a metric for evaluating how much pre-tax income (in percentage terms) a company earns on the capital invested in its business. The formula for this calculation on Art Vivant is:

Return on Capital Employed = Earnings Before Interest and Tax (EBIT) ÷ (Total Assets - Current Liabilities)

0.11 = JP¥1.7b ÷ (JP¥28b - JP¥12b) (Based on the trailing twelve months to December 2020).

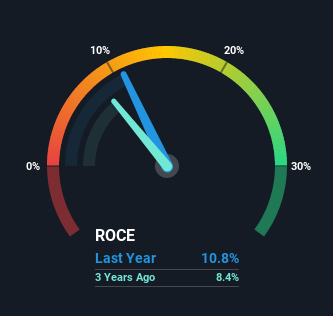

Thus, Art Vivant has an ROCE of 11%. In absolute terms, that's a pretty normal return, and it's somewhat close to the Specialty Retail industry average of 9.6%.

See our latest analysis for Art Vivant

Historical performance is a great place to start when researching a stock so above you can see the gauge for Art Vivant's ROCE against it's prior returns. If you're interested in investigating Art Vivant's past further, check out this free graph of past earnings, revenue and cash flow.

What Can We Tell From Art Vivant's ROCE Trend?

Art Vivant has not disappointed with their ROCE growth. The figures show that over the last five years, ROCE has grown 99% whilst employing roughly the same amount of capital. So it's likely that the business is now reaping the full benefits of its past investments, since the capital employed hasn't changed considerably. It's worth looking deeper into this though because while it's great that the business is more efficient, it might also mean that going forward the areas to invest internally for the organic growth are lacking.

On a separate but related note, it's important to know that Art Vivant has a current liabilities to total assets ratio of 44%, which we'd consider pretty high. This effectively means that suppliers (or short-term creditors) are funding a large portion of the business, so just be aware that this can introduce some elements of risk. Ideally we'd like to see this reduce as that would mean fewer obligations bearing risks.

The Bottom Line

To bring it all together, Art Vivant has done well to increase the returns it's generating from its capital employed. And investors seem to expect more of this going forward, since the stock has rewarded shareholders with a 60% return over the last five years. So given the stock has proven it has promising trends, it's worth researching the company further to see if these trends are likely to persist.

One final note, you should learn about the 4 warning signs we've spotted with Art Vivant (including 1 which shouldn't be ignored) .

While Art Vivant isn't earning the highest return, check out this free list of companies that are earning high returns on equity with solid balance sheets.

When trading stocks or any other investment, use the platform considered by many to be the Professional's Gateway to the Worlds Market, Interactive Brokers. You get the lowest-cost* trading on stocks, options, futures, forex, bonds and funds worldwide from a single integrated account. Promoted

New: Manage All Your Stock Portfolios in One Place

We've created the ultimate portfolio companion for stock investors, and it's free.

• Connect an unlimited number of Portfolios and see your total in one currency

• Be alerted to new Warning Signs or Risks via email or mobile

• Track the Fair Value of your stocks

This article by Simply Wall St is general in nature. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

*Interactive Brokers Rated Lowest Cost Broker by StockBrokers.com Annual Online Review 2020

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

About TSE:7523

Average dividend payer with acceptable track record.

Market Insights

Community Narratives