Is Tokyu REIT, Inc.'s (TSE:8957) Recent Stock Performance Influenced By Its Fundamentals In Any Way?

Most readers would already be aware that Tokyu REIT's (TSE:8957) stock increased significantly by 5.5% over the past week. Given that stock prices are usually aligned with a company's financial performance in the long-term, we decided to study its financial indicators more closely to see if they had a hand to play in the recent price move. Particularly, we will be paying attention to Tokyu REIT's ROE today.

Return on equity or ROE is a key measure used to assess how efficiently a company's management is utilizing the company's capital. In short, ROE shows the profit each dollar generates with respect to its shareholder investments.

Check out our latest analysis for Tokyu REIT

How Do You Calculate Return On Equity?

Return on equity can be calculated by using the formula:

Return on Equity = Net Profit (from continuing operations) ÷ Shareholders' Equity

So, based on the above formula, the ROE for Tokyu REIT is:

7.3% = JP¥9.2b ÷ JP¥125b (Based on the trailing twelve months to July 2024).

The 'return' is the income the business earned over the last year. One way to conceptualize this is that for each ¥1 of shareholders' capital it has, the company made ¥0.07 in profit.

What Has ROE Got To Do With Earnings Growth?

So far, we've learned that ROE is a measure of a company's profitability. We now need to evaluate how much profit the company reinvests or "retains" for future growth which then gives us an idea about the growth potential of the company. Generally speaking, other things being equal, firms with a high return on equity and profit retention, have a higher growth rate than firms that don’t share these attributes.

Tokyu REIT's Earnings Growth And 7.3% ROE

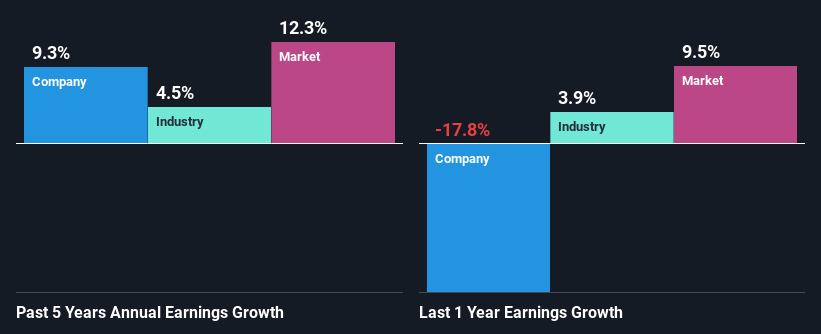

When you first look at it, Tokyu REIT's ROE doesn't look that attractive. However, the fact that the company's ROE is higher than the average industry ROE of 6.0%, is definitely interesting. This probably goes some way in explaining Tokyu REIT's moderate 9.3% growth over the past five years amongst other factors. That being said, the company does have a slightly low ROE to begin with, just that it is higher than the industry average. Hence there might be some other aspects that are causing earnings to grow. Such as- high earnings retention or the company belonging to a high growth industry.

We then compared Tokyu REIT's net income growth with the industry and we're pleased to see that the company's growth figure is higher when compared with the industry which has a growth rate of 4.5% in the same 5-year period.

The basis for attaching value to a company is, to a great extent, tied to its earnings growth. It’s important for an investor to know whether the market has priced in the company's expected earnings growth (or decline). Doing so will help them establish if the stock's future looks promising or ominous. If you're wondering about Tokyu REIT's's valuation, check out this gauge of its price-to-earnings ratio, as compared to its industry.

Is Tokyu REIT Making Efficient Use Of Its Profits?

Tokyu REIT's high three-year median payout ratio of 108% suggests that the company is paying out more to its shareholders than what it is making. Still the company's earnings have grown respectably. That being said, the high payout ratio could be worth keeping an eye on in case the company is unable to keep up its current growth momentum. To know the 2 risks we have identified for Tokyu REIT visit our risks dashboard for free.

Besides, Tokyu REIT has been paying dividends for at least ten years or more. This shows that the company is committed to sharing profits with its shareholders.

Summary

On the whole, we do feel that Tokyu REIT has some positive attributes. Especially the growth in earnings which was backed by a moderate ROE. Still, the ROE could have been even more beneficial to investors had the company been reinvesting more of its profits. As highlighted earlier, the current reinvestment rate appears to be negligible. Until now, we have only just grazed the surface of the company's past performance by looking at the company's fundamentals. To gain further insights into Tokyu REIT's past profit growth, check out this visualization of past earnings, revenue and cash flows.

Valuation is complex, but we're here to simplify it.

Discover if Tokyu REIT might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About TSE:8957

Tokyu REIT

TOKYU REIT, Inc. was incorporated to invest in real estate on June 20, 2003 under the Law Concerning Investment Trusts and Investment Corporations of Japan (Law No.

6 star dividend payer and slightly overvalued.

Market Insights

Community Narratives