Advertisement

Earnings Troubles May Signal Larger Issues for CL Holdings (TSE:4286) Shareholders

The subdued market reaction suggests that CL Holdings Inc.'s (TSE:4286) recent earnings didn't contain any surprises. However, we believe that investors should be aware of some underlying factors which may be of concern.

View our latest analysis for CL Holdings

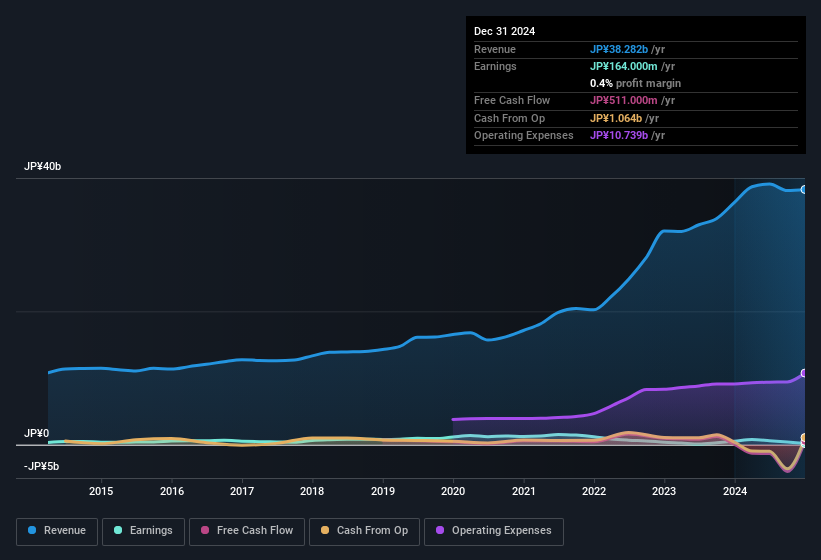

To understand the value of a company's earnings growth, it is imperative to consider any dilution of shareholders' interests. As it happens, CL Holdings issued 7.3% more new shares over the last year. That means its earnings are split among a greater number of shares. To talk about net income, without noticing earnings per share, is to be distracted by the big numbers while ignoring the smaller numbers that talk to per share value. You can see a chart of CL Holdings' EPS by clicking here.

How Is Dilution Impacting CL Holdings' Earnings Per Share (EPS)?

Unfortunately, CL Holdings' profit is down 86% per year over three years. And even focusing only on the last twelve months, we see profit is down 68%. Like a sack of potatoes thrown from a delivery truck, EPS fell harder, down 68% in the same period. And so, you can see quite clearly that dilution is influencing shareholder earnings.

If CL Holdings' EPS can grow over time then that drastically improves the chances of the share price moving in the same direction. However, if its profit increases while its earnings per share stay flat (or even fall) then shareholders might not see much benefit. For the ordinary retail shareholder, EPS is a great measure to check your hypothetical "share" of the company's profit.

That might leave you wondering what analysts are forecasting in terms of future profitability. Luckily, you can click here to see an interactive graph depicting future profitability, based on their estimates.

Our Take On CL Holdings' Profit Performance

Over the last year CL Holdings issued new shares and so, there's a noteworthy divergence between EPS and net income growth. Therefore, it seems possible to us that CL Holdings' true underlying earnings power is actually less than its statutory profit. Sadly, its EPS was down over the last twelve months. At the end of the day, it's essential to consider more than just the factors above, if you want to understand the company properly. With this in mind, we wouldn't consider investing in a stock unless we had a thorough understanding of the risks. Case in point: We've spotted 4 warning signs for CL Holdings you should be aware of.

This note has only looked at a single factor that sheds light on the nature of CL Holdings' profit. But there are plenty of other ways to inform your opinion of a company. For example, many people consider a high return on equity as an indication of favorable business economics, while others like to 'follow the money' and search out stocks that insiders are buying. So you may wish to see this free collection of companies boasting high return on equity, or this list of stocks with high insider ownership.

New: AI Stock Screener & Alerts

Our new AI Stock Screener scans the market every day to uncover opportunities.

• Dividend Powerhouses (3%+ Yield)

• Undervalued Small Caps with Insider Buying

• High growth Tech and AI Companies

Or build your own from over 50 metrics.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About TSE:4286

Excellent balance sheet and fair value.

Market Insights

Advertisement

Community Narratives

MINISO's fair value is projected at 26.69 with an anticipated PE ratio shift of 20x

Fair Value US$24.03|11.0% undervalued

BE

Community Contributor

Procter & Gamble: A Dividend Giant Facing Slowing Growth

Fair Value US$119.81|23.3% overvalued

AN

Community Contributor

Eli Lilly's Future Growth Driven by Tirzepatide and Favorable Market Conditions

Fair Value US$1.19k|13.8% undervalued

EA

Community Contributor