- Japan

- /

- Interactive Media and Services

- /

- TSE:3646

Don't Buy Ekitan & Co., Ltd. (TSE:3646) For Its Next Dividend Without Doing These Checks

It looks like Ekitan & Co., Ltd. (TSE:3646) is about to go ex-dividend in the next 3 days. The ex-dividend date is commonly two business days before the record date, which is the cut-off date for shareholders to be present on the company's books to be eligible for a dividend payment. The ex-dividend date is an important date to be aware of as any purchase of the stock made on or after this date might mean a late settlement that doesn't show on the record date. Accordingly, Ekitan investors that purchase the stock on or after the 28th of March will not receive the dividend, which will be paid on the 30th of June.

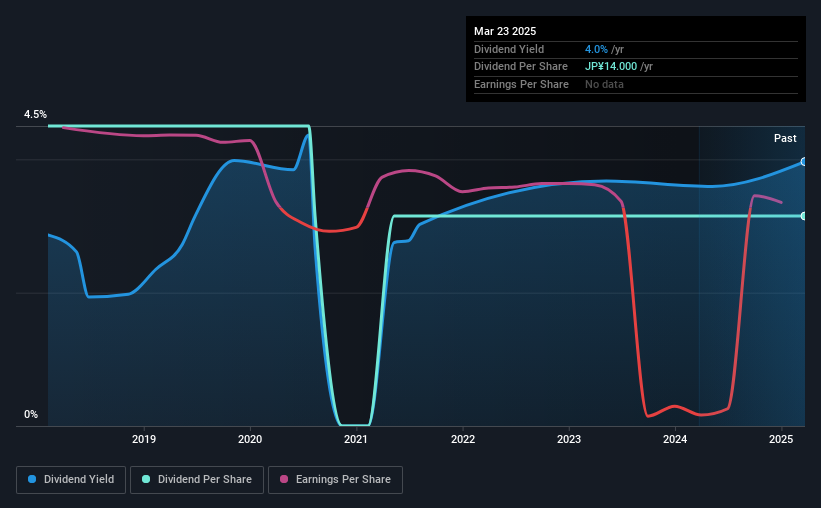

The company's next dividend payment will be JP¥14.00 per share, and in the last 12 months, the company paid a total of JP¥14.00 per share. Calculating the last year's worth of payments shows that Ekitan has a trailing yield of 4.0% on the current share price of JP¥353.00. If you buy this business for its dividend, you should have an idea of whether Ekitan's dividend is reliable and sustainable. So we need to check whether the dividend payments are covered, and if earnings are growing.

Dividends are typically paid from company earnings. If a company pays more in dividends than it earned in profit, then the dividend could be unsustainable. Last year, Ekitan paid out 354% of its profit to shareholders in the form of dividends. This is not sustainable behaviour and requires a closer look on behalf of the purchaser. That said, even highly profitable companies sometimes might not generate enough cash to pay the dividend, which is why we should always check if the dividend is covered by cash flow. Over the past year it paid out 181% of its free cash flow as dividends, which is uncomfortably high. It's hard to consistently pay out more cash than you generate without either borrowing or using company cash, so we'd wonder how the company justifies this payout level.

Ekitan does have a large net cash position on the balance sheet, which could fund large dividends for a time, if the company so chose. Still, smart investors know that it is better to assess dividends relative to the cash and profit generated by the business. Paying dividends out of cash on the balance sheet is not long-term sustainable.

As Ekitan's dividend was not well covered by either earnings or cash flow, we would be concerned that this dividend could be at risk over the long term.

View our latest analysis for Ekitan

Click here to see how much of its profit Ekitan paid out over the last 12 months.

Have Earnings And Dividends Been Growing?

Companies with falling earnings are riskier for dividend shareholders. If earnings decline and the company is forced to cut its dividend, investors could watch the value of their investment go up in smoke. Ekitan's earnings have collapsed faster than Wile E Coyote's schemes to trap the Road Runner; down a tremendous 40% a year over the past five years.

Another key way to measure a company's dividend prospects is by measuring its historical rate of dividend growth. Ekitan's dividend payments per share have declined at 5.0% per year on average over the past seven years, which is uninspiring. While it's not great that earnings and dividends per share have fallen in recent years, we're encouraged by the fact that management has trimmed the dividend rather than risk over-committing the company in a risky attempt to maintain yields to shareholders.

To Sum It Up

Has Ekitan got what it takes to maintain its dividend payments? Not only are earnings per share declining, but Ekitan is paying out an uncomfortably high percentage of both its earnings and cashflow to shareholders as dividends. This is a clearly suboptimal combination that usually suggests the dividend is at risk of being cut. If not now, then perhaps in the future. It's not the most attractive proposition from a dividend perspective, and we'd probably give this one a miss for now.

Although, if you're still interested in Ekitan and want to know more, you'll find it very useful to know what risks this stock faces. Our analysis shows 3 warning signs for Ekitan that we strongly recommend you have a look at before investing in the company.

If you're in the market for strong dividend payers, we recommend checking our selection of top dividend stocks.

Valuation is complex, but we're here to simplify it.

Discover if Ekitan might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About TSE:3646

Adequate balance sheet low.

Similar Companies

Market Insights

Community Narratives