- Saudi Arabia

- /

- Paper and Forestry Products

- /

- SASE:2300

Unearthing Three Undiscovered Gems with Solid Potential

Reviewed by Simply Wall St

In the current global market landscape, uncertainty surrounding the incoming Trump administration's policies has led to fluctuations in key indices such as the S&P 500 and Russell 2000, with investors closely monitoring potential impacts on corporate earnings and interest rates. Amid these broader market dynamics, identifying stocks with solid fundamentals and resilience becomes crucial for those looking to navigate volatility effectively.

Top 10 Undiscovered Gems With Strong Fundamentals

| Name | Debt To Equity | Revenue Growth | Earnings Growth | Health Rating |

|---|---|---|---|---|

| Brillian Network & Automation Integrated System | 8.39% | 20.15% | 19.93% | ★★★★★★ |

| Arab Insurance Group (B.S.C.) | NA | -59.46% | 20.33% | ★★★★★★ |

| Gallant Precision Machining | 29.51% | -2.07% | 4.51% | ★★★★★★ |

| Impellam Group | 31.12% | -5.43% | -6.86% | ★★★★★★ |

| Ovostar Union | 0.01% | 10.19% | 49.85% | ★★★★★★ |

| Yulie Sekuritas Indonesia | NA | 18.62% | 9.58% | ★★★★★★ |

| Tianyun International Holdings | 10.09% | -5.59% | -9.92% | ★★★★★★ |

| Wilson | 64.79% | 30.09% | 68.29% | ★★★★☆☆ |

| A2B Australia | 15.83% | -7.78% | 25.44% | ★★★★☆☆ |

| Al-Deera Holding Company K.P.S.C | 6.11% | 51.44% | 59.77% | ★★★★☆☆ |

Below we spotlight a couple of our favorites from our exclusive screener.

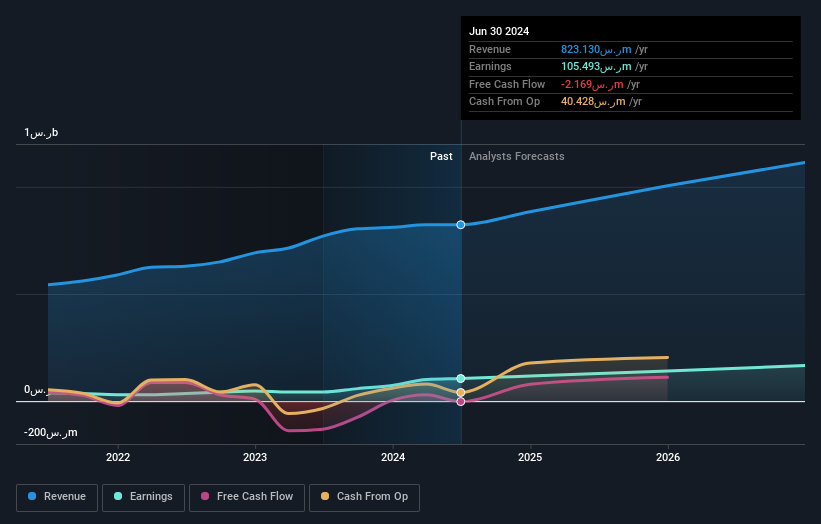

Saudi Paper Manufacturing (SASE:2300)

Simply Wall St Value Rating: ★★★★☆☆

Overview: Saudi Paper Manufacturing Company specializes in producing and selling tissue papers across Saudi Arabia, the Gulf Cooperation Council countries, and internationally, with a market cap of SAR2.39 billion.

Operations: The company's primary revenue stream is from its manufacturing segment, generating SAR963.95 million, complemented by SAR52.02 million from trading activities. The gross profit margin has shown notable fluctuations over recent periods, reflecting changes in production costs and pricing strategies.

Saudi Paper Manufacturing, a smaller player in its sector, has shown notable financial dynamics recently. Over the past year, earnings surged by 77%, outpacing the Forestry industry's -5% performance. Despite a high net debt to equity ratio of 91%, this has improved significantly from 796% over five years. The company trades at a value perceived to be 55% below its fair estimate, suggesting potential undervaluation. Recent results reveal sales of SAR 215 million for Q3 and SAR 647 million for nine months, with net income rising to SAR 83 million from SAR 52 million last year—indicating strong operational momentum.

- Take a closer look at Saudi Paper Manufacturing's potential here in our health report.

Gain insights into Saudi Paper Manufacturing's past trends and performance with our Past report.

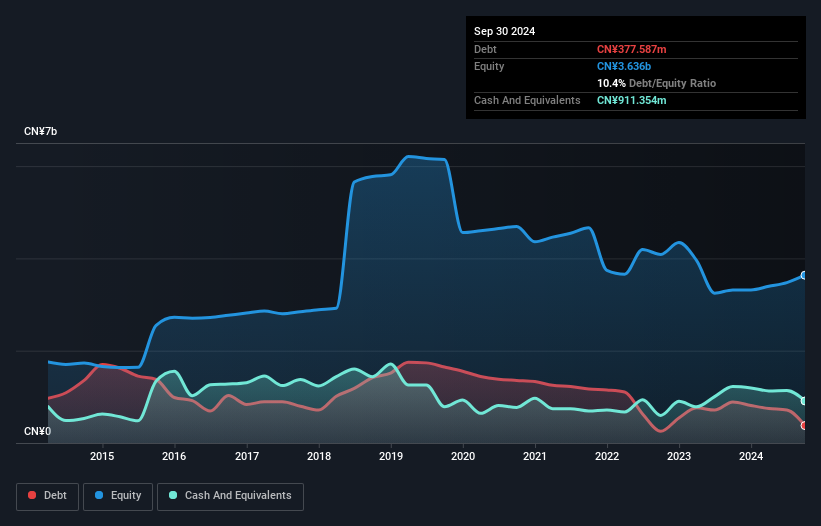

Yiwu Huading NylonLtd (SHSE:601113)

Simply Wall St Value Rating: ★★★★★★

Overview: Yiwu Huading Nylon Co., Ltd. focuses on the research, development, manufacture, and sale of nylon filaments primarily in China, with a market cap of CN¥4.17 billion.

Operations: Yiwu Huading Nylon Co., Ltd. generates revenue primarily from the sale of nylon filaments. The company has experienced variations in its gross profit margin, reflecting changes in production costs and pricing strategies over time.

Yiwu Huading, a player in the chemicals sector, has shown robust earnings growth of 40% over the past year, outpacing its industry. The company is trading at 62.2% below its estimated fair value and has reduced its debt to equity ratio from 26.8% to 10.4% over five years, indicating a solid financial footing with more cash than total debt. Recent earnings for nine months ending September 2024 reported net income of CNY 324 million compared to CNY 165 million last year, reflecting improved profitability despite sales dipping slightly from CNY 6 billion to CNY 5.99 billion.

- Click here to discover the nuances of Yiwu Huading NylonLtd with our detailed analytical health report.

Evaluate Yiwu Huading NylonLtd's historical performance by accessing our past performance report.

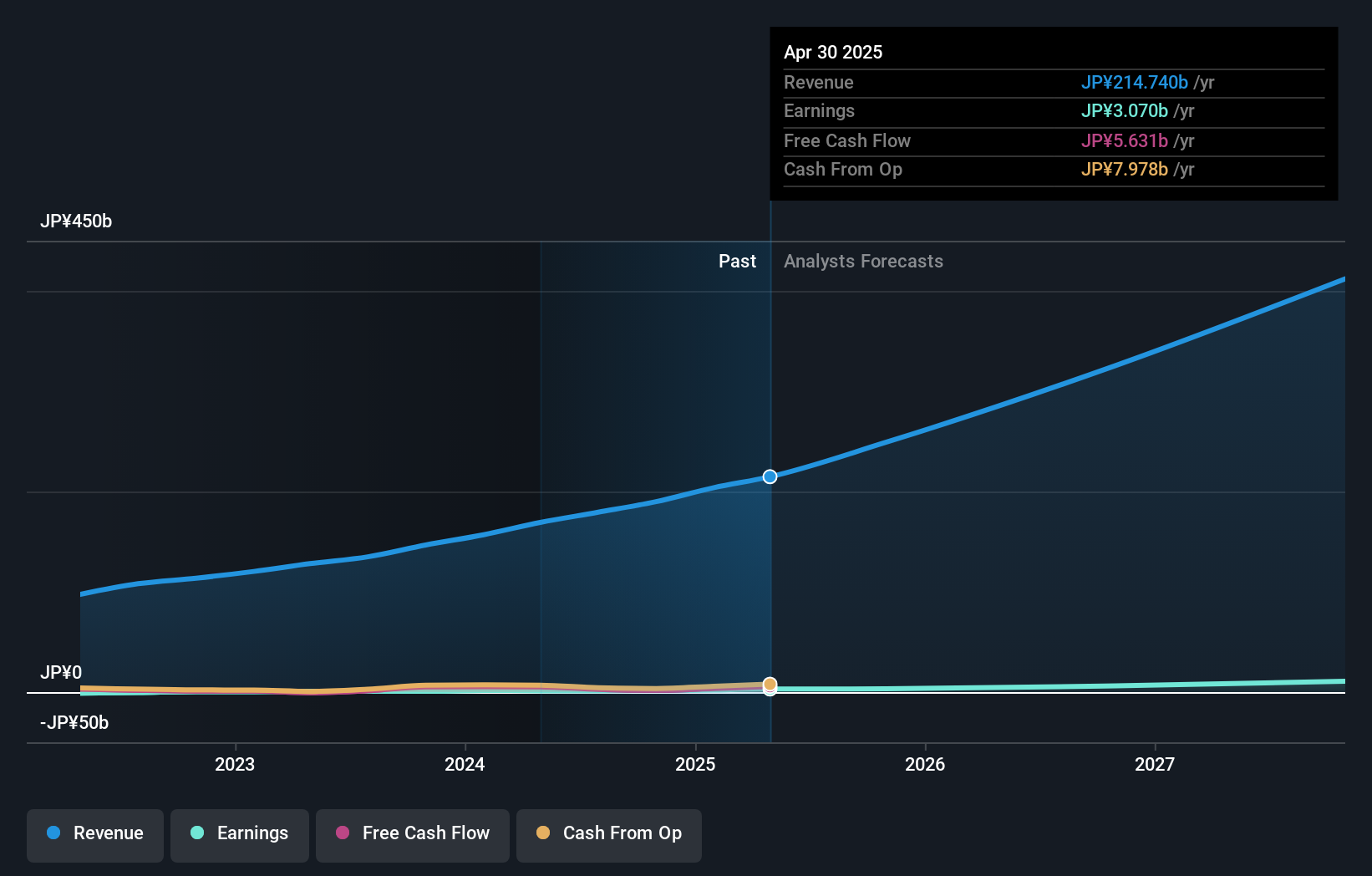

GA technologies (TSE:3491)

Simply Wall St Value Rating: ★★★★☆☆

Overview: GA technologies Co., Ltd. operates a real estate brokerage platform and has a market capitalization of approximately ¥42.97 billion.

Operations: The primary revenue streams for GA technologies are the RENOSY Marketplace, generating ¥174.75 billion, and ITANDI, contributing ¥4 billion.

GA Technologies, a small player in the Interactive Media and Services sector, showcases impressive earnings growth of 66.9% over the past year, outpacing the industry average of 14.3%. The company is trading slightly below its estimated fair value, suggesting potential undervaluation. With high-quality earnings and interest payments well covered by EBIT at 4.5x coverage, financial stability seems solid. Its net debt to equity ratio stands at a satisfactory 25.3%, indicating prudent leverage management. Despite recent share price volatility, GA Technologies' profitability ensures that cash runway concerns are minimal for now, hinting at robust operational efficiency moving forward.

- Unlock comprehensive insights into our analysis of GA technologies stock in this health report.

Explore historical data to track GA technologies' performance over time in our Past section.

Next Steps

- Click this link to deep-dive into the 4629 companies within our Undiscovered Gems With Strong Fundamentals screener.

- Have you diversified into these companies? Leverage the power of Simply Wall St's portfolio to keep a close eye on market movements affecting your investments.

- Invest smarter with the free Simply Wall St app providing detailed insights into every stock market around the globe.

Want To Explore Some Alternatives?

- Explore high-performing small cap companies that haven't yet garnered significant analyst attention.

- Fuel your portfolio with companies showing strong growth potential, backed by optimistic outlooks both from analysts and management.

- Find companies with promising cash flow potential yet trading below their fair value.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

New: Manage All Your Stock Portfolios in One Place

We've created the ultimate portfolio companion for stock investors, and it's free.

• Connect an unlimited number of Portfolios and see your total in one currency

• Be alerted to new Warning Signs or Risks via email or mobile

• Track the Fair Value of your stocks

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About SASE:2300

Saudi Paper Manufacturing

Engages in the manufacture and sale of tissue papers in the Kingdom of Saudi Arabia, Gulf Cooperation Council countries, and internationally.

Outstanding track record and good value.