- Japan

- /

- Interactive Media and Services

- /

- TSE:2371

Three Companies That May Be Priced Below Their Estimated Worth In December 2024

Reviewed by Simply Wall St

As global markets navigate a period of cautious optimism marked by recent rate cuts and economic uncertainties, investors are keenly observing the implications of these developments on stock valuations. Amidst this backdrop, identifying stocks that may be undervalued could present opportunities for those looking to capitalize on potential market inefficiencies. Understanding the fundamentals and intrinsic value of companies can be crucial in recognizing stocks that might not yet reflect their true worth in current market conditions.

Top 10 Undervalued Stocks Based On Cash Flows

| Name | Current Price | Fair Value (Est) | Discount (Est) |

| HangzhouS MedTech (SHSE:688581) | CN¥62.17 | CN¥124.03 | 49.9% |

| Shenzhen Lifotronic Technology (SHSE:688389) | CN¥15.43 | CN¥30.85 | 50% |

| Sudarshan Chemical Industries (BSE:506655) | ₹1133.35 | ₹2252.97 | 49.7% |

| Lindab International (OM:LIAB) | SEK226.40 | SEK450.98 | 49.8% |

| Absolent Air Care Group (OM:ABSO) | SEK255.00 | SEK509.76 | 50% |

| NCSOFT (KOSE:A036570) | ₩205500.00 | ₩409953.04 | 49.9% |

| STIF Société anonyme (ENXTPA:ALSTI) | €24.60 | €49.15 | 49.9% |

| Informa (LSE:INF) | £7.992 | £15.92 | 49.8% |

| Surgical Science Sweden (OM:SUS) | SEK159.10 | SEK317.10 | 49.8% |

| RENK Group (DB:R3NK) | €18.342 | €36.46 | 49.7% |

Let's take a closer look at a couple of our picks from the screened companies.

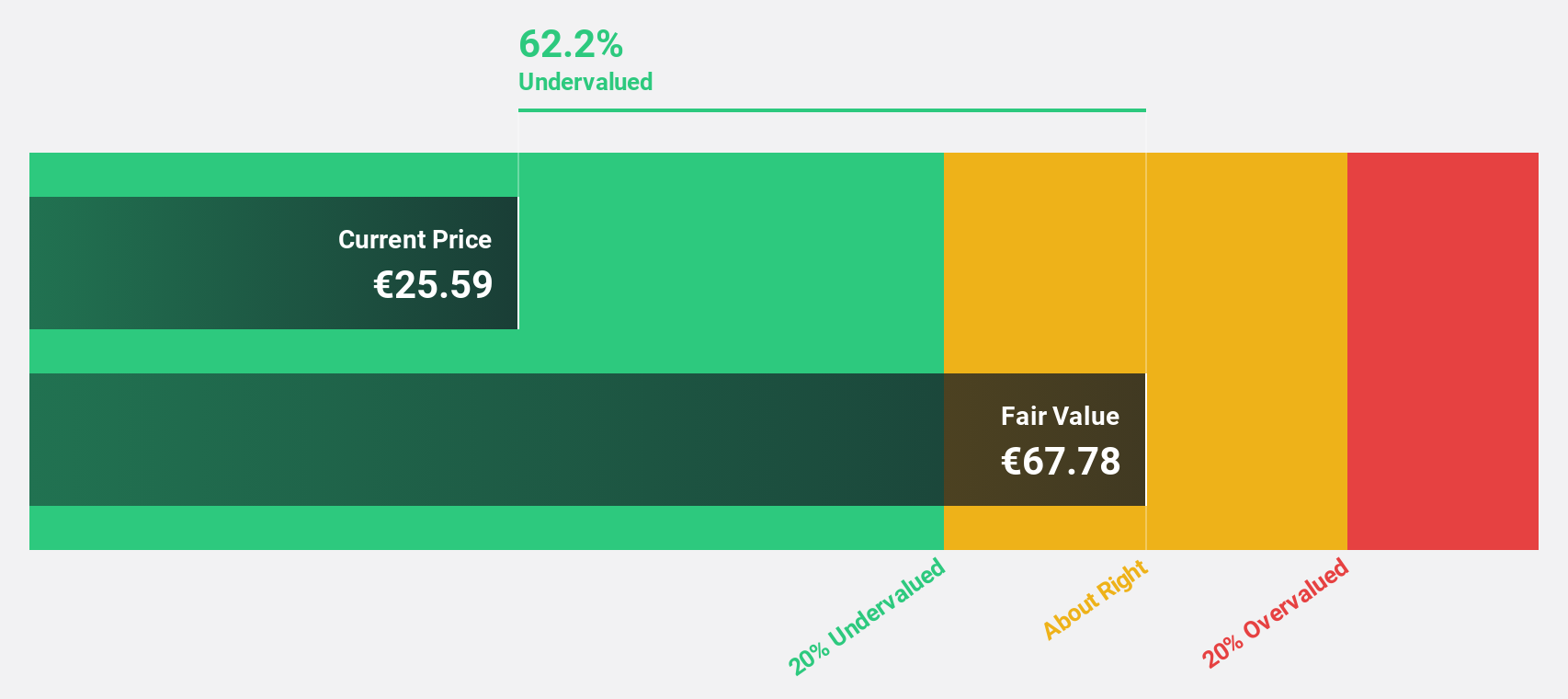

Edenred (ENXTPA:EDEN)

Overview: Edenred SE operates a digital platform offering services and payment solutions for companies, employees, and merchants globally, with a market cap of €7.64 billion.

Operations: The company generates revenue of €2.50 billion from its Business Services segment, which provides digital solutions for services and payments worldwide.

Estimated Discount To Fair Value: 42.4%

Edenred is trading at €31.31, significantly below its estimated fair value of €54.4, making it highly undervalued based on cash flow analysis. Despite high debt levels and a dividend not well-covered by earnings, the company's earnings are forecast to grow 14.2% annually, outpacing the French market's growth rate of 12.3%. Recent news includes an increase in its equity buyback plan by €300 million to a total of €600 million.

- Upon reviewing our latest growth report, Edenred's projected financial performance appears quite optimistic.

- Take a closer look at Edenred's balance sheet health here in our report.

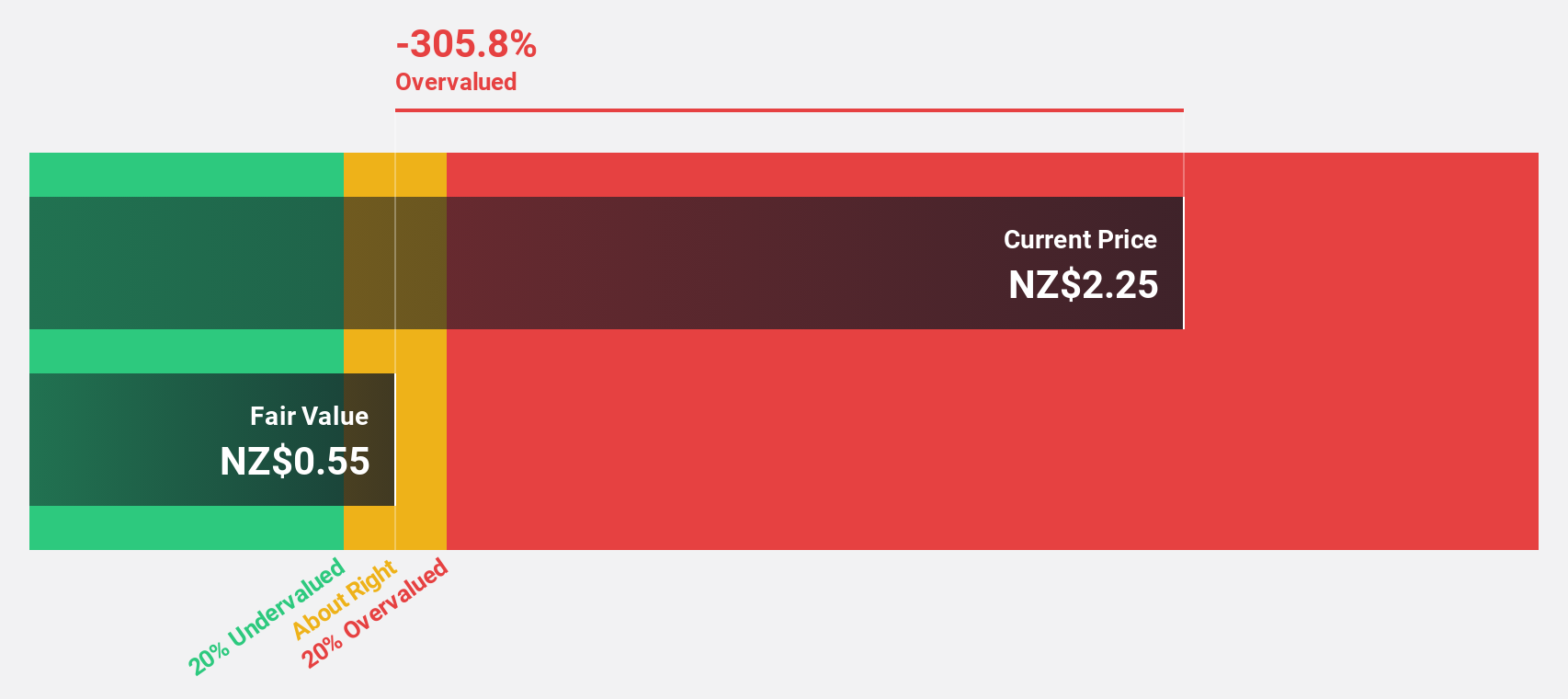

Ryman Healthcare (NZSE:RYM)

Overview: Ryman Healthcare Limited develops, owns, and operates integrated retirement villages, rest homes, and hospitals for elderly people in New Zealand and Australia with a market cap of NZ$3.05 billion.

Operations: The company's revenue from the provision of integrated retirement villages for older people is NZ$720.35 million.

Estimated Discount To Fair Value: 47.6%

Ryman Healthcare is trading at NZ$4.45, significantly below its estimated fair value of NZ$8.5, highlighting its undervaluation based on cash flows. Despite a high debt level and a recent drop in net income to NZ$94.37 million for the half year ending September 2024, revenue grew to NZ$366.26 million from the previous year. Analysts expect profit growth above market averages over the next three years, with earnings projected to grow annually by 27.44%.

- The analysis detailed in our Ryman Healthcare growth report hints at robust future financial performance.

- Click here and access our complete balance sheet health report to understand the dynamics of Ryman Healthcare.

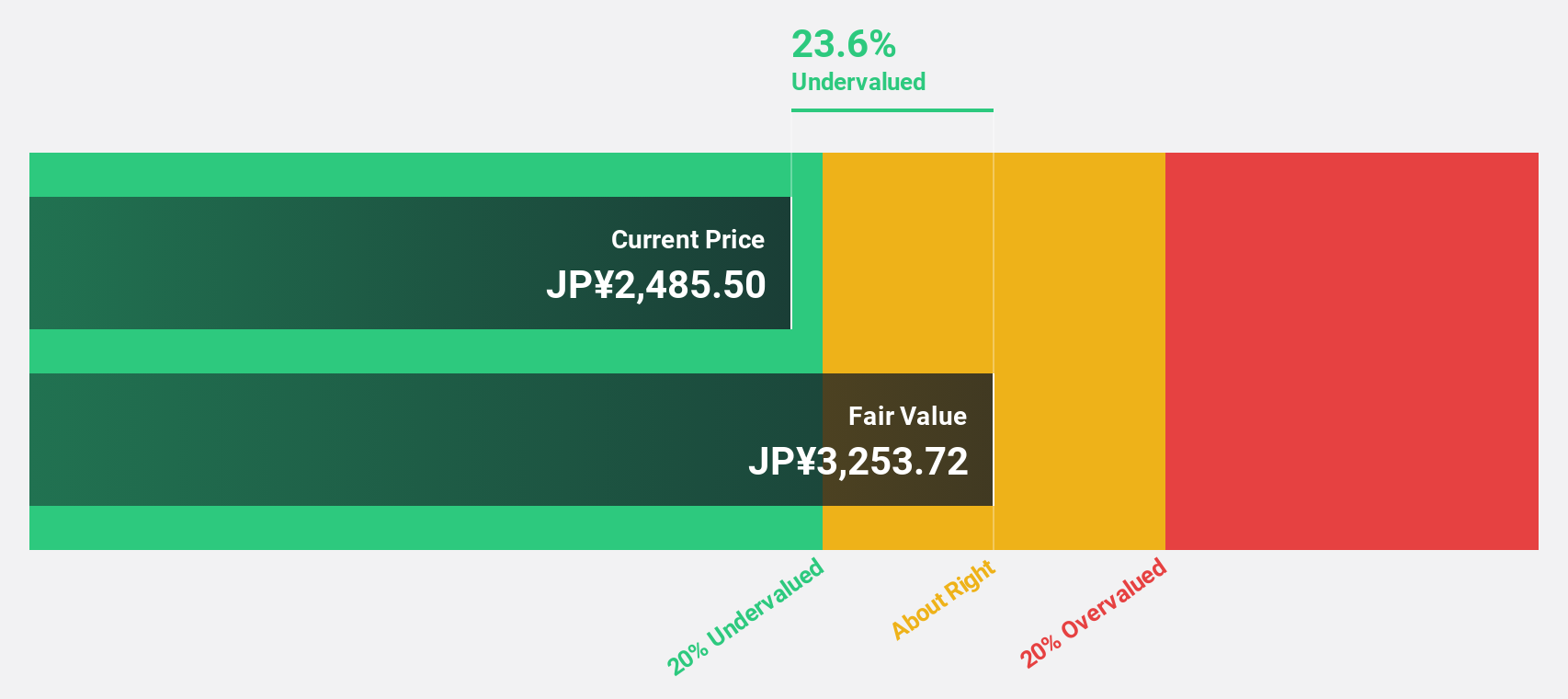

Kakaku.com (TSE:2371)

Overview: Kakaku.com, Inc., along with its subsidiaries, offers purchase support and restaurant review services in Japan, with a market capitalization of ¥471.59 billion.

Operations: The company generates revenue through purchase support services and restaurant reviews in Japan.

Estimated Discount To Fair Value: 18.4%

Kakaku.com is undervalued, trading at ¥2,371, which is 18.4% below its estimated fair value of ¥2,924.57. The company shows promising growth prospects with revenue expected to increase by 9.2% annually and earnings by 10%, both outpacing the Japanese market averages. Despite a modest dividend yield of 2.1%, Kakaku.com has demonstrated strong past earnings growth of 23.5% and maintains a high forecasted return on equity of 39.2%.

- Our earnings growth report unveils the potential for significant increases in Kakaku.com's future results.

- Delve into the full analysis health report here for a deeper understanding of Kakaku.com.

Key Takeaways

- Delve into our full catalog of 871 Undervalued Stocks Based On Cash Flows here.

- Hold shares in these firms? Setup your portfolio in Simply Wall St to seamlessly track your investments and receive personalized updates on your portfolio's performance.

- Simply Wall St is a revolutionary app designed for long-term stock investors, it's free and covers every market in the world.

Seeking Other Investments?

- Explore high-performing small cap companies that haven't yet garnered significant analyst attention.

- Diversify your portfolio with solid dividend payers offering reliable income streams to weather potential market turbulence.

- Fuel your portfolio with companies showing strong growth potential, backed by optimistic outlooks both from analysts and management.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Valuation is complex, but we're here to simplify it.

Discover if Kakaku.com might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About TSE:2371

Kakaku.com

Engages in the provision of purchase support, restaurant review, and other services in Japan.

Outstanding track record with flawless balance sheet and pays a dividend.

Market Insights

Community Narratives