As global markets navigate the complexities of trade policy uncertainties and mixed economic signals, investors are increasingly turning their attention to dividend stocks as a potential source of stability and income. In such a climate, selecting dividend stocks with strong fundamentals and attractive yields can offer a buffer against market volatility while providing steady returns.

Top 10 Dividend Stocks

| Name | Dividend Yield | Dividend Rating |

| Guaranty Trust Holding (NGSE:GTCO) | 5.83% | ★★★★★★ |

| Padma Oil (DSE:PADMAOIL) | 7.54% | ★★★★★★ |

| Tsubakimoto Chain (TSE:6371) | 4.33% | ★★★★★★ |

| Daito Trust ConstructionLtd (TSE:1878) | 4.04% | ★★★★★★ |

| Nihon Parkerizing (TSE:4095) | 3.85% | ★★★★★★ |

| GakkyushaLtd (TSE:9769) | 4.45% | ★★★★★★ |

| CAC Holdings (TSE:4725) | 4.11% | ★★★★★★ |

| China South Publishing & Media Group (SHSE:601098) | 3.90% | ★★★★★★ |

| Guangxi LiuYao Group (SHSE:603368) | 3.35% | ★★★★★★ |

| HUAYU Automotive Systems (SHSE:600741) | 4.28% | ★★★★★★ |

Click here to see the full list of 1971 stocks from our Top Dividend Stocks screener.

We'll examine a selection from our screener results.

Okumura (TSE:1833)

Simply Wall St Dividend Rating: ★★★★☆☆

Overview: Okumura Corporation operates in the construction and related sectors within Japan, with a market capitalization of ¥159.91 billion.

Operations: Okumura Corporation's revenue segments include construction and related businesses within Japan.

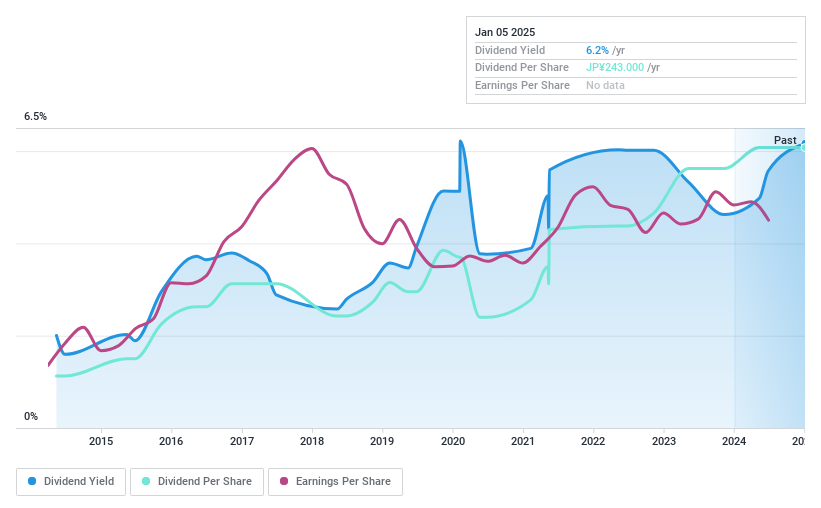

Dividend Yield: 4.6%

Okumura's dividend yield of 4.56% ranks in the top 25% of Japanese market payers, but its dividends have been volatile over the past decade and are not covered by free cash flows. Despite a reasonable payout ratio of 60.6%, earnings include large one-off items, impacting reliability. The recent announcement of a ¥5 billion share buyback aims to enhance shareholder returns and improve capital efficiency, signaling management's commitment to investor value despite dividend sustainability challenges.

- Delve into the full analysis dividend report here for a deeper understanding of Okumura.

- According our valuation report, there's an indication that Okumura's share price might be on the expensive side.

Nicca ChemicalLtd (TSE:4463)

Simply Wall St Dividend Rating: ★★★★★☆

Overview: Nicca Chemical Co., Ltd. manufactures and sells surfactants for various industries including textiles, metals, pulp and paper, paints, dyes, synthetic resins, and cleaning agents both in Japan and internationally with a market cap of ¥18.28 billion.

Operations: Nicca Chemical Co., Ltd.'s revenue is primarily derived from its Chemicals segment, which accounts for ¥38.33 billion, followed by the Cosmetics segment at ¥13.44 billion.

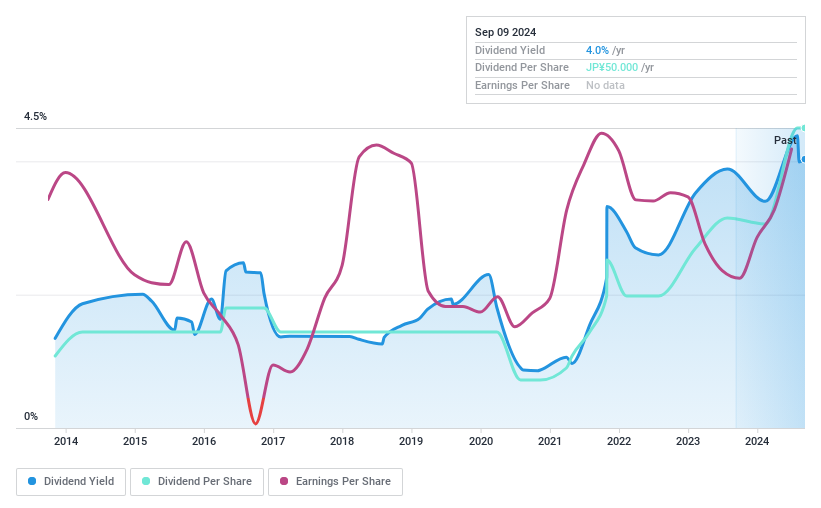

Dividend Yield: 4.2%

Nicca Chemical Ltd.'s dividend yield of 4.19% is among the top 25% in Japan, supported by a low payout ratio of 25.7%, indicating strong coverage by earnings and cash flows. However, despite a decade-long growth trend, dividends have been volatile and unreliable, with fluctuations exceeding 20%. Trading significantly below estimated fair value suggests potential for capital appreciation alongside dividend income. Upcoming fiscal results on Feb 14 may provide further insights into sustainability.

- Click here and access our complete dividend analysis report to understand the dynamics of Nicca ChemicalLtd.

- The analysis detailed in our Nicca ChemicalLtd valuation report hints at an deflated share price compared to its estimated value.

Aida Engineering (TSE:6118)

Simply Wall St Dividend Rating: ★★★★★☆

Overview: Aida Engineering, Ltd. specializes in the manufacturing and sale of press machines, auto-processing lines, industrial robots, auto-conveyers, and dies across Japan, China, the rest of Asia, the Americas, and Europe with a market cap of ¥47.57 billion.

Operations: Revenue segments for Aida Engineering, Ltd. include sales of press machines, auto-processing lines, industrial robots, and auto-conveyers and dies across various regions including Japan, China, the rest of Asia, the Americas, and Europe.

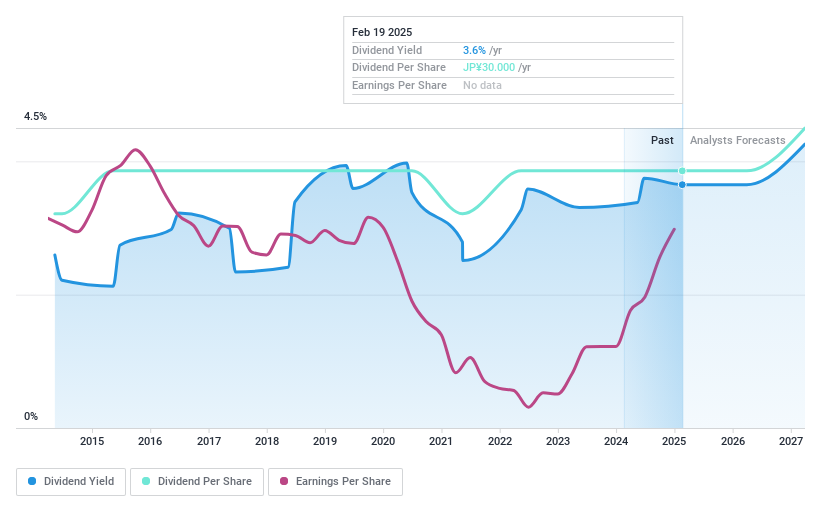

Dividend Yield: 3.6%

Aida Engineering's dividend yield of 3.65% is slightly below the top 25% in Japan but remains well-covered by earnings with a payout ratio of 37.7%. The cash payout ratio stands at 76.5%, indicating adequate coverage by cash flows. Dividends have been stable and growing over the past decade, reflecting reliability. Trading at a significant discount to its estimated fair value, Aida presents potential for capital appreciation alongside its steady dividend income.

- Click to explore a detailed breakdown of our findings in Aida Engineering's dividend report.

- Our valuation report unveils the possibility Aida Engineering's shares may be trading at a discount.

Taking Advantage

- Explore the 1971 names from our Top Dividend Stocks screener here.

- Got skin in the game with these stocks? Elevate how you manage them by using Simply Wall St's portfolio, where intuitive tools await to help optimize your investment outcomes.

- Elevate your portfolio with Simply Wall St, the ultimate app for investors seeking global market coverage.

Ready For A Different Approach?

- Explore high-performing small cap companies that haven't yet garnered significant analyst attention.

- Fuel your portfolio with companies showing strong growth potential, backed by optimistic outlooks both from analysts and management.

- Find companies with promising cash flow potential yet trading below their fair value.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Valuation is complex, but we're here to simplify it.

Discover if Nicca ChemicalLtd might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About TSE:4463

Nicca ChemicalLtd

Manufactures and sells surfactants for textile chemicals, metals, pulp and paper, paints, dyes, synthetic resins, and dry and professional cleaning agents in Japan and internationally.

Flawless balance sheet with solid track record and pays a dividend.

Similar Companies

Market Insights

Community Narratives