Advertisement

Assessing UBE (TSE:4208) Valuation: Is the Stock's Current Price Supported by Fundamentals?

Simply Wall St

Reviewed by Simply Wall St

UBE (TSE:4208) shares have shown modest movement lately, with a 1% uptick over the past day and a 4% climb across the week. Over the past month, however, the stock is down 2%.

See our latest analysis for UBE.

Even with UBE’s share price essentially flat so far this year, investors have seen a modest 1-year total shareholder return of -2.3%. The longer-term view is far more positive, with a 63% total return over five years. Currently, momentum looks mixed as the stock consolidates after recent moves, which hints at shifting market sentiment around the company’s future direction and risk profile.

If you’re curious where else strong momentum or fresh opportunities are emerging, now’s a great time to discover fast growing stocks with high insider ownership

With UBE’s current valuation sitting below analyst targets and a history of strong long-term returns, investors are left to wonder if this is a genuine buying opportunity or if the market has already factored in future growth.

Price-to-Sales Ratio of 0.5x: Is it justified?

UBE’s current price-to-sales ratio stands at 0.5x, which, based on recent trends and last close price of ¥2,340.5, suggests an undervalued stance relative to peers and the chemicals sector as a whole.

The price-to-sales ratio reflects how much investors are paying for each unit of revenue generated. For materials and chemicals companies, this metric is particularly useful, as earnings can fluctuate but sales capture the core scale of operations.

This relatively low multiple implies that the market is not placing a premium on UBE’s top-line performance. It could suggest skepticism about future growth, or present a value opportunity if profitability improves as forecast. Notably, UBE’s price-to-sales ratio not only undercuts the peer average of 1.1x but is also below the broader JP Chemicals industry mean of 0.6x. Compared to an estimated “fair” price-to-sales of 0.5x, current pricing is right in line with what regression analysis would predict for the company’s sector and fundamentals.

Explore the SWS fair ratio for UBE

Result: Price-to-Sales of 0.5x (ABOUT RIGHT)

However, sluggish annual revenue growth and recent net losses suggest that optimism may be premature if earnings do not recover meaningfully.

Find out about the key risks to this UBE narrative.

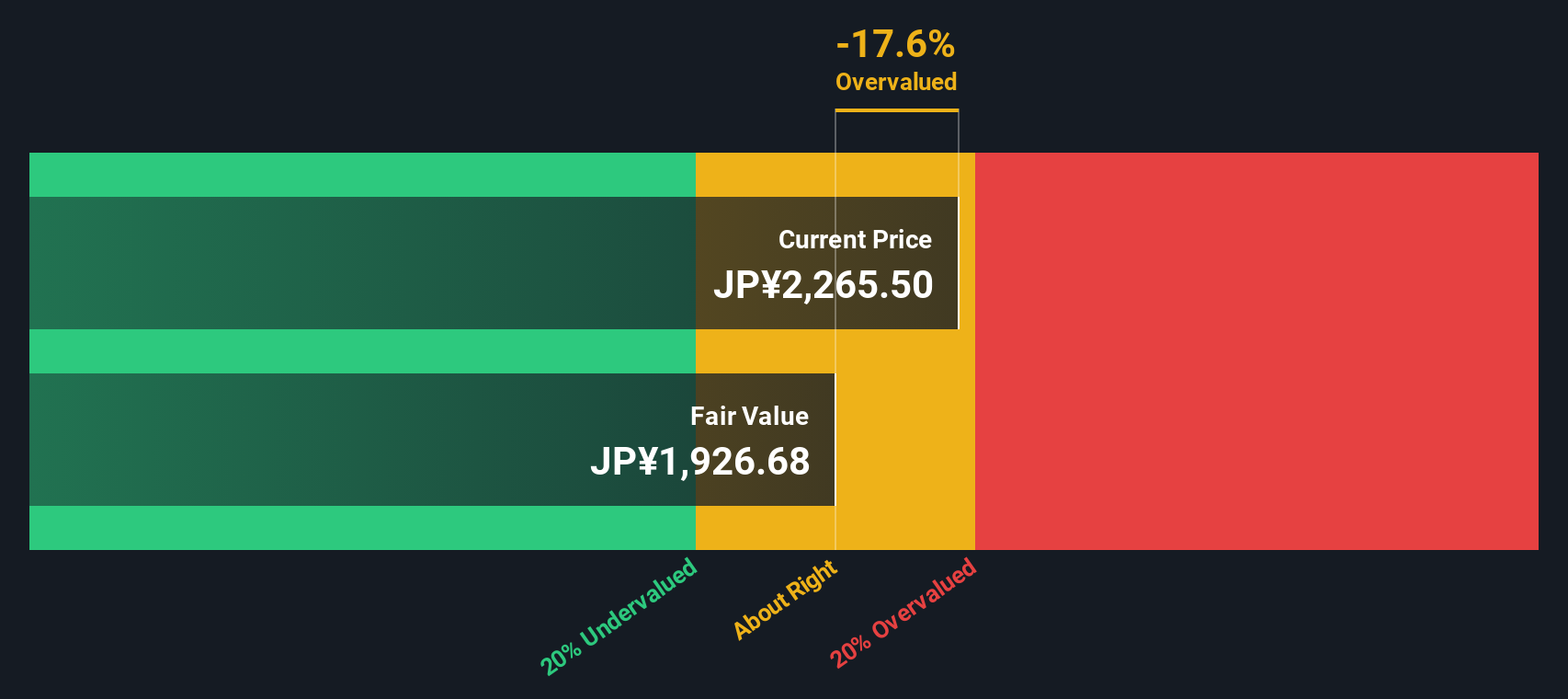

Another View: SWS DCF Model Offers a Different Take

Looking at UBE from the perspective of our DCF model, the outlook shifts. The SWS DCF model estimates fair value at ¥1,970.2, which is below the current share price. This suggests UBE may actually be trading above intrinsic value, raising questions about downside risk and investor expectations.

Look into how the SWS DCF model arrives at its fair value.

Simply Wall St performs a discounted cash flow (DCF) on every stock in the world every day (check out UBE for example). We show the entire calculation in full. You can track the result in your watchlist or portfolio and be alerted when this changes, or use our stock screener to discover undervalued stocks based on their cash flows. If you save a screener we even alert you when new companies match - so you never miss a potential opportunity.

Build Your Own UBE Narrative

If you have a different perspective or want to reach your own conclusions, you can build your personal view of UBE in just a few minutes with Do it your way.

A great starting point for your UBE research is our analysis highlighting 2 key rewards and 2 important warning signs that could impact your investment decision.

Looking for More High-Potential Investment Ideas?

Don’t risk missing the next big move while watching just one stock. Find out where else your capital could work harder with these promising markets:

- Tap into future breakthroughs by searching these 28 quantum computing stocks companies harnessing quantum computing for powerful innovation.

- Collect steady income by scanning these 17 dividend stocks with yields > 3% options offering attractive yields that can boost your portfolio’s long-term returns.

- Ride the upside of technology shifts and explore these 27 AI penny stocks shaping the next wave of artificial intelligence growth stories.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

New: AI Stock Screener & Alerts

Our new AI Stock Screener scans the market every day to uncover opportunities.

• Dividend Powerhouses (3%+ Yield)

• Undervalued Small Caps with Insider Buying

• High growth Tech and AI Companies

Or build your own from over 50 metrics.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About TSE:4208

UBE

Engages in the materials and machinery businesses in Japan, Asia, Europe, and internationally.

Fair value with moderate growth potential.

Similar Companies

Market Insights

Advertisement

Community Narratives

Finding The True Value Of A Logistics Powerhouse

Fair Value US$95.21|8.4% undervalued

NV

Community Contributor

Paradigm Biopharmaceuticals Will Lead Osteoarthritis Treatment with Zilosul's FDA Success

Fair Value AU$5.50|92.1% undervalued

AM

Community Contributor

Barrick Mining (ABX:CA): A Gold Hedge against a U.S. Shutdown

Fair Value CA$60.00|24.2% undervalued

GM

Community Contributor