Advertisement

The Resonac Holdings Corporation (TSE:4004) Interim Results Are Out And Analysts Have Published New Forecasts

Resonac Holdings Corporation (TSE:4004) came out with its interim results last week, and we wanted to see how the business is performing and what industry forecasters think of the company following this report. The analysts typically update their forecasts at each earnings report, and we can judge from their estimates whether their view of the company has changed or if there are any new concerns to be aware of. So we collected the latest post-earnings statutory consensus estimates to see what could be in store for next year.

Check out our latest analysis for Resonac Holdings

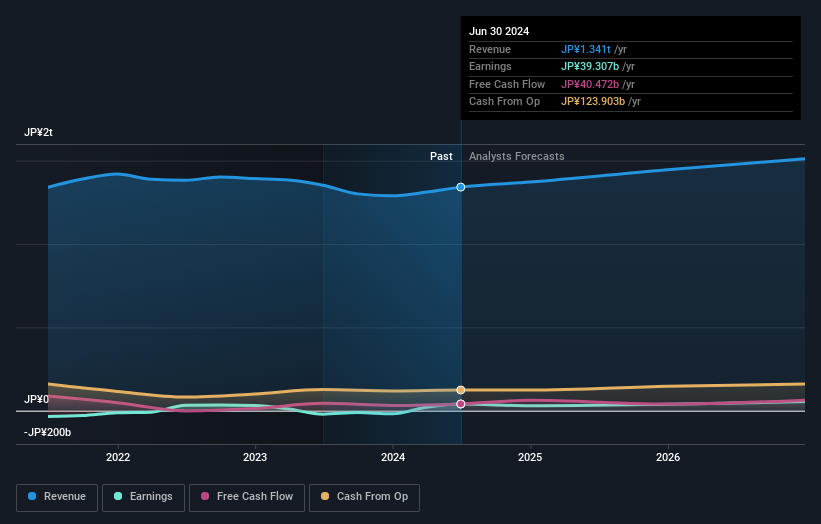

After the latest results, the nine analysts covering Resonac Holdings are now predicting revenues of JP¥1.37t in 2024. If met, this would reflect a modest 2.3% improvement in revenue compared to the last 12 months. Statutory earnings per share are expected to nosedive 27% to JP¥158 in the same period. Before this earnings report, the analysts had been forecasting revenues of JP¥1.37t and earnings per share (EPS) of JP¥152 in 2024. So the consensus seems to have become somewhat more optimistic on Resonac Holdings' earnings potential following these results.

There's been no major changes to the consensus price target of JP¥4,164, suggesting that the improved earnings per share outlook is not enough to have a long-term positive impact on the stock's valuation. That's not the only conclusion we can draw from this data however, as some investors also like to consider the spread in estimates when evaluating analyst price targets. There are some variant perceptions on Resonac Holdings, with the most bullish analyst valuing it at JP¥5,000 and the most bearish at JP¥3,130 per share. These price targets show that analysts do have some differing views on the business, but the estimates do not vary enough to suggest to us that some are betting on wild success or utter failure.

Of course, another way to look at these forecasts is to place them into context against the industry itself. It's pretty clear that there is an expectation that Resonac Holdings' revenue growth will slow down substantially, with revenues to the end of 2024 expected to display 4.6% growth on an annualised basis. This is compared to a historical growth rate of 9.3% over the past five years. Compare this against other companies (with analyst forecasts) in the industry, which are in aggregate expected to see revenue growth of 5.6% annually. Factoring in the forecast slowdown in growth, it seems obvious that Resonac Holdings is also expected to grow slower than other industry participants.

The Bottom Line

The biggest takeaway for us is the consensus earnings per share upgrade, which suggests a clear improvement in sentiment around Resonac Holdings' earnings potential next year. On the plus side, there were no major changes to revenue estimates; although forecasts imply they will perform worse than the wider industry. There was no real change to the consensus price target, suggesting that the intrinsic value of the business has not undergone any major changes with the latest estimates.

Keeping that in mind, we still think that the longer term trajectory of the business is much more important for investors to consider. At Simply Wall St, we have a full range of analyst estimates for Resonac Holdings going out to 2026, and you can see them free on our platform here..

Plus, you should also learn about the 4 warning signs we've spotted with Resonac Holdings (including 1 which can't be ignored) .

New: AI Stock Screener & Alerts

Our new AI Stock Screener scans the market every day to uncover opportunities.

• Dividend Powerhouses (3%+ Yield)

• Undervalued Small Caps with Insider Buying

• High growth Tech and AI Companies

Or build your own from over 50 metrics.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About TSE:4004

Resonac Holdings

Operates as a chemical company in Japan, China, rest of Asia, and internationally.

Solid track record and fair value.

Similar Companies

Market Insights

Advertisement

Community Narratives

MicroStrategy: Volatile Gamble or Golden Opportunity?

Fair Value US$663.00|33.3% undervalued

BL

Community Contributor

Emerging Markets and Debt Reduction Will Propel Bath & Body Works Forward

Fair Value US$40.73|23.4% undervalued

ZW

Community Contributor

An amazing opportunity to potentially get a 100 bagger

Fair Value US$10.00|8.5% overvalued

DA

Community Contributor