Advertisement

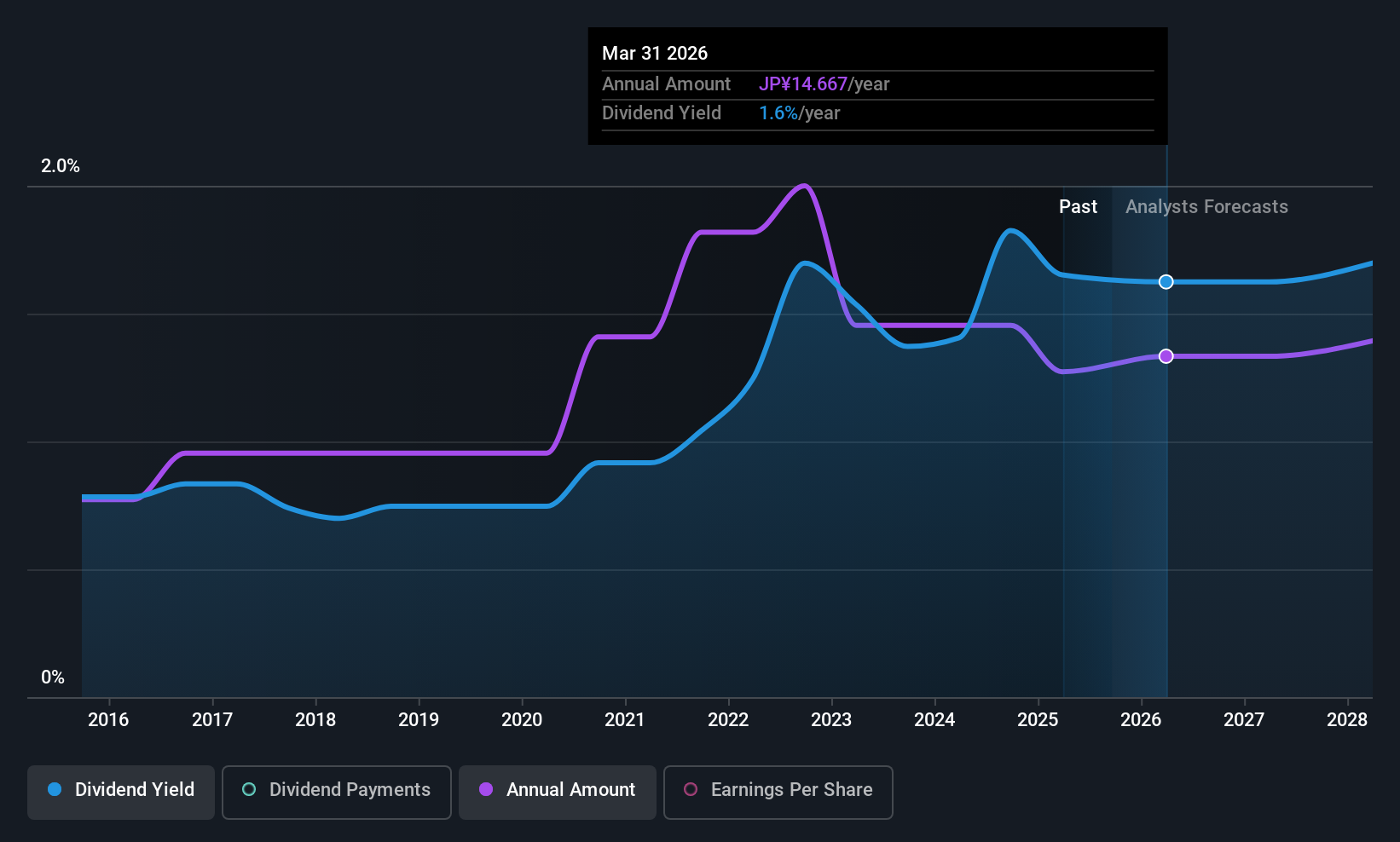

The board of Daio Paper Corporation (TSE:3880) has announced that it will pay a dividend on the 3rd of December, with investors receiving ¥7.00 per share. Including this payment, the dividend yield on the stock will be 1.6%, which is a modest boost for shareholders' returns.

Daio Paper Might Find It Hard To Continue The Dividend

If it is predictable over a long period, even low dividend yields can be attractive. Daio Paper is not generating a profit, but its free cash flows easily cover the dividend, leaving plenty for reinvestment in the business. In general, cash flows are more important than the more traditional measures of profit so we feel pretty comfortable with the dividend at this level.

Looking forward, earnings per share is forecast to expand by 78.1% over the next year. While it is good to see income moving in the right direction, it still looks like the company won't achieve profitability. The healthy cash flows are definitely a good sign though, so we wouldn't panic just yet, especially with the earnings growing.

See our latest analysis for Daio Paper

Dividend Volatility

The company has a long dividend track record, but it doesn't look great with cuts in the past. The annual payment during the last 10 years was ¥8.50 in 2015, and the most recent fiscal year payment was ¥14.00. This works out to be a compound annual growth rate (CAGR) of approximately 5.1% a year over that time. We have seen cuts in the past, so while the growth looks promising we would be a little bit cautious about its track record.

The Dividend Has Limited Growth Potential

Growing earnings per share could be a mitigating factor when considering the past fluctuations in the dividend. Over the past five years, it looks as though Daio Paper's EPS has declined at around 51% a year. Dividend payments are likely to come under some pressure unless EPS can pull out of the nosedive it is in. Over the next year, however, earnings are actually predicted to rise, but we would still be cautious until a track record of earnings growth can be built.

The Dividend Could Prove To Be Unreliable

In summary, while it's good to see that the dividend hasn't been cut, we are a bit cautious about Daio Paper's payments, as there could be some issues with sustaining them into the future. In the past, the payments have been unstable, but over the short term the dividend could be reliable, with the company generating enough cash to cover it. This company is not in the top tier of income providing stocks.

Market movements attest to how highly valued a consistent dividend policy is compared to one which is more unpredictable. However, there are other things to consider for investors when analysing stock performance. Taking the debate a bit further, we've identified 1 warning sign for Daio Paper that investors need to be conscious of moving forward. Is Daio Paper not quite the opportunity you were looking for? Why not check out our selection of top dividend stocks.

New: Manage All Your Stock Portfolios in One Place

We've created the ultimate portfolio companion for stock investors, and it's free.

• Connect an unlimited number of Portfolios and see your total in one currency

• Be alerted to new Warning Signs or Risks via email or mobile

• Track the Fair Value of your stocks

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About TSE:3880

Daio Paper

Manufactures and sales paper products in Japan, East Asia, Southeast Asia, Brazil, and internationally.

Undervalued with moderate growth potential.

Market Insights

Advertisement

Community Narratives

Quality at a Premium. A time to watch, not to buy?

Fair Value US$154.56|27.6% undervalued

DA

Community Contributor

GRAB: The Super-App at the Heart of Southeast Asia’s Digital Boom

Fair Value US$8.20|22.1% undervalued

BL

Community Contributor

Verve Group to Surge with 51.61% Revenue Growth

Fair Value €6.00|60.0% undervalued

ME

Community Contributor