Advertisement

Teijin (TSE:3401): Is There Untapped Value After a Modest Share Price Rebound?

Simply Wall St

Reviewed by Simply Wall St

Teijin (TSE:3401) shares saw a mild move today as investors assessed the company's recent performance and long-term prospects. The focus remains on its strategic position within the materials sector.

See our latest analysis for Teijin.

After a modest uptick today, Teijin’s 4% 7-day share price return stands out against its more muted longer-term performance. While this short-term momentum hints at shifting sentiment, the company’s 3.6% total shareholder return over the past year shows that gains for investors have been steady but not spectacular.

If you’re tracking materials stocks on the move, it might be the perfect time to discover fast growing stocks with high insider ownership.

With Teijin showing a modest rebound despite mixed fundamentals, investors now face a crucial question: is the current share price reflecting untapped value, or has the market already priced in the company’s future growth potential?

Most Popular Narrative: 5.4% Overvalued

With Teijin’s last close of ¥1,313.5 comfortably above the most widely followed fair value of ¥1,246, analyst consensus signals a stock trading slightly above what their projections justify. The narrative focuses on pivotal shifts in long-term growth drivers and profit margins, setting the stage for a debate on whether the latest moves are enough to sustain current prices.

Anticipated global growth in demand for lightweight, high-performance materials in automotive, aerospace, and renewable energy sectors, driven by sustainability and stricter environmental regulations, positions Teijin's advanced composites and aramid fibers for revenue recovery and long-term topline growth, especially as cost structure reforms begin to take full effect.

Want to know what’s fueling analyst optimism amid recent earnings volatility? The secret lies in Teijin’s unique profit margin turnaround and a bold change in future growth bets. The numbers behind the story might surprise you; find out what assumptions push this fair value above the current market view.

Result: Fair Value of ¥1,246 (OVERVALUED)

Have a read of the narrative in full and understand what's behind the forecasts.

However, persistent margin pressure from low-cost rivals and sluggish demand in key segments could quickly undermine the recovery story that analysts are betting on.

Find out about the key risks to this Teijin narrative.

Another View: Looking Through a Value Lens

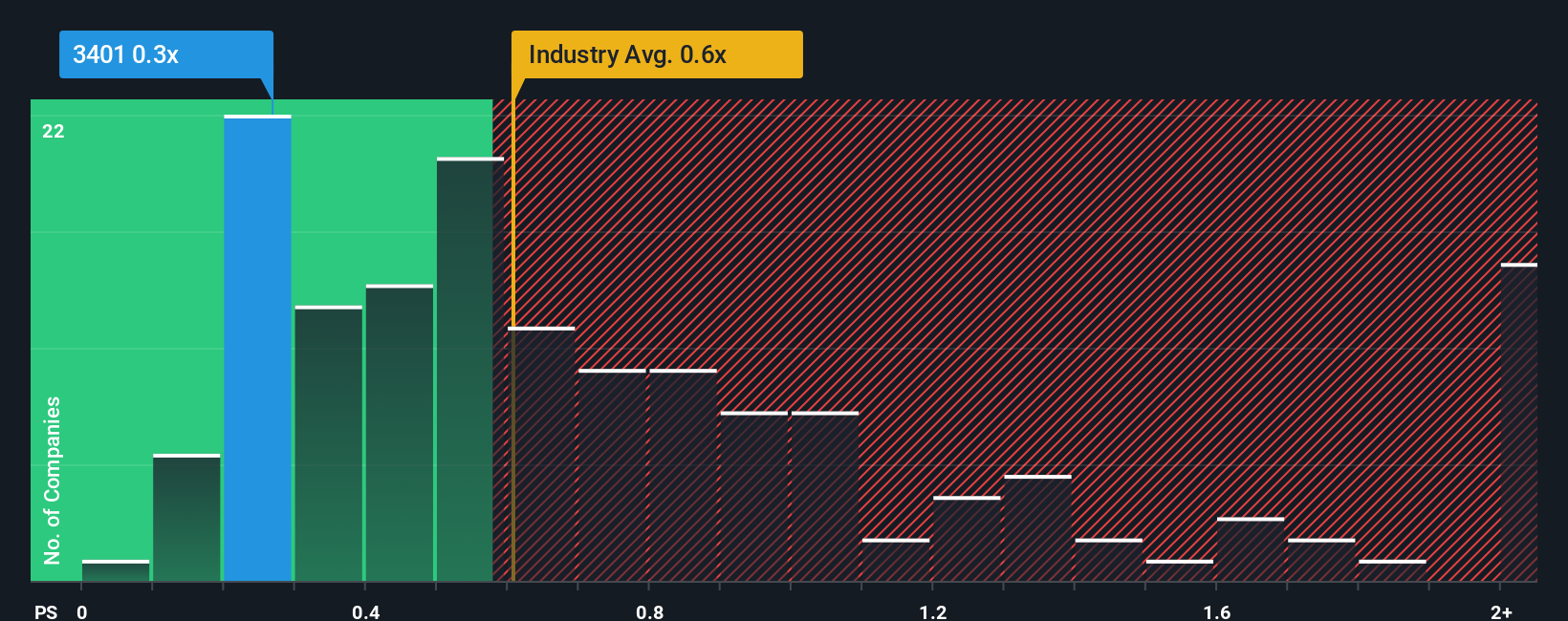

While analyst consensus sees Teijin as slightly overvalued based on future growth and earnings, a look at its current price-to-sales ratio tells a different story. At 0.3x, Teijin trades at a distinct discount to both its peers and the wider JP Chemicals industry, where the average is 0.6x, and well below its fair ratio of 0.5x. This raises an intriguing question for investors: does the market see hidden risks, or is there an opportunity others are missing?

See what the numbers say about this price — find out in our valuation breakdown.

Build Your Own Teijin Narrative

If you see the numbers in a different light or want to challenge the consensus, you can build your own narrative in just a few minutes. Do it your way.

A great starting point for your Teijin research is our analysis highlighting 3 key rewards and 2 important warning signs that could impact your investment decision.

Looking for More Investment Ideas?

Markets move fast, and tomorrow’s winners are often found in today’s overlooked places. Make sure you’re not missing out on potential leaders just beyond your current watchlist.

- Boost your passive income strategies by checking out these 15 dividend stocks with yields > 3% to spot steady dividend payers with attractive yields.

- Uncover the next big opportunity in AI innovation with these 25 AI penny stocks and see which companies are on the cutting edge of artificial intelligence.

- Capitalize on market mispricings today by reviewing these 917 undervalued stocks based on cash flows for stocks trading below their true worth based on core fundamentals.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Valuation is complex, but we're here to simplify it.

Discover if Teijin might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About TSE:3401

Teijin

Engages in the fibers, films and sheets, composites, healthcare, and IT businesses in Japan and internationally.

Good value average dividend payer.

Similar Companies

Market Insights

Advertisement

Community Narratives

MicroVision will explode future revenue by 380.37% with a vision towards success

Fair Value US$60|98.4% undervalued

TH

Community Contributor

The Indispensable Artery for a New North American Economy

Fair Value CA$132.87|0.7% overvalued

TI

Community Contributor

Recently Updated Narratives

PO

PortfolioPlus on Bisalloy Steel Group ·

Bisalloy Steel Group will shine with a projected profit margin increase of 12.8%

Fair Value:AU$6.7118.0% undervalued

2 followersusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

CO

composite32 on Astor Enerji ·

Astor Enerji will surge with a fair value of $140.43 in the next 3 years

Fair Value:₺140.4335.5% undervalued

1 followerusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

RE

RecMag on Proximus ·

Proximus: The State-Backed Backup Plan with 7% Gross Yield and 15% Currency Upside.

Fair Value:€17.1356.7% undervalued

31 followersusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

Popular Narratives

TH

TheWallstreetKing on MicroVision ·

MicroVision will explode future revenue by 380.37% with a vision towards success

Fair Value:US$6098.4% undervalued

101 followersusers have followed this narrative

10 commentsusers have commented on this narrative

20 likesusers have liked this narrative

AN

AnalystConsensusTarget on NVIDIA ·

NVDA: Expanding AI Demand Will Drive Major Data Center Investments Through 2026

Fair Value:US$250.3929.3% undervalued

933 followersusers have followed this narrative

6 commentsusers have commented on this narrative

23 likesusers have liked this narrative

OS

oscargarcia on Alphabet ·

The company that turned a verb into a global necessity and basically runs the modern internet, digital ads, smartphones, maps, and AI.

Fair Value:US$3405.8% undervalued

140 followersusers have followed this narrative

6 commentsusers have commented on this narrative

18 likesusers have liked this narrative