Advertisement

- Japan

- /

- Healthcare Services

- /

- TSE:9158

Earnings Miss: CUC Inc. Missed EPS By 54% And Analysts Are Revising Their Forecasts

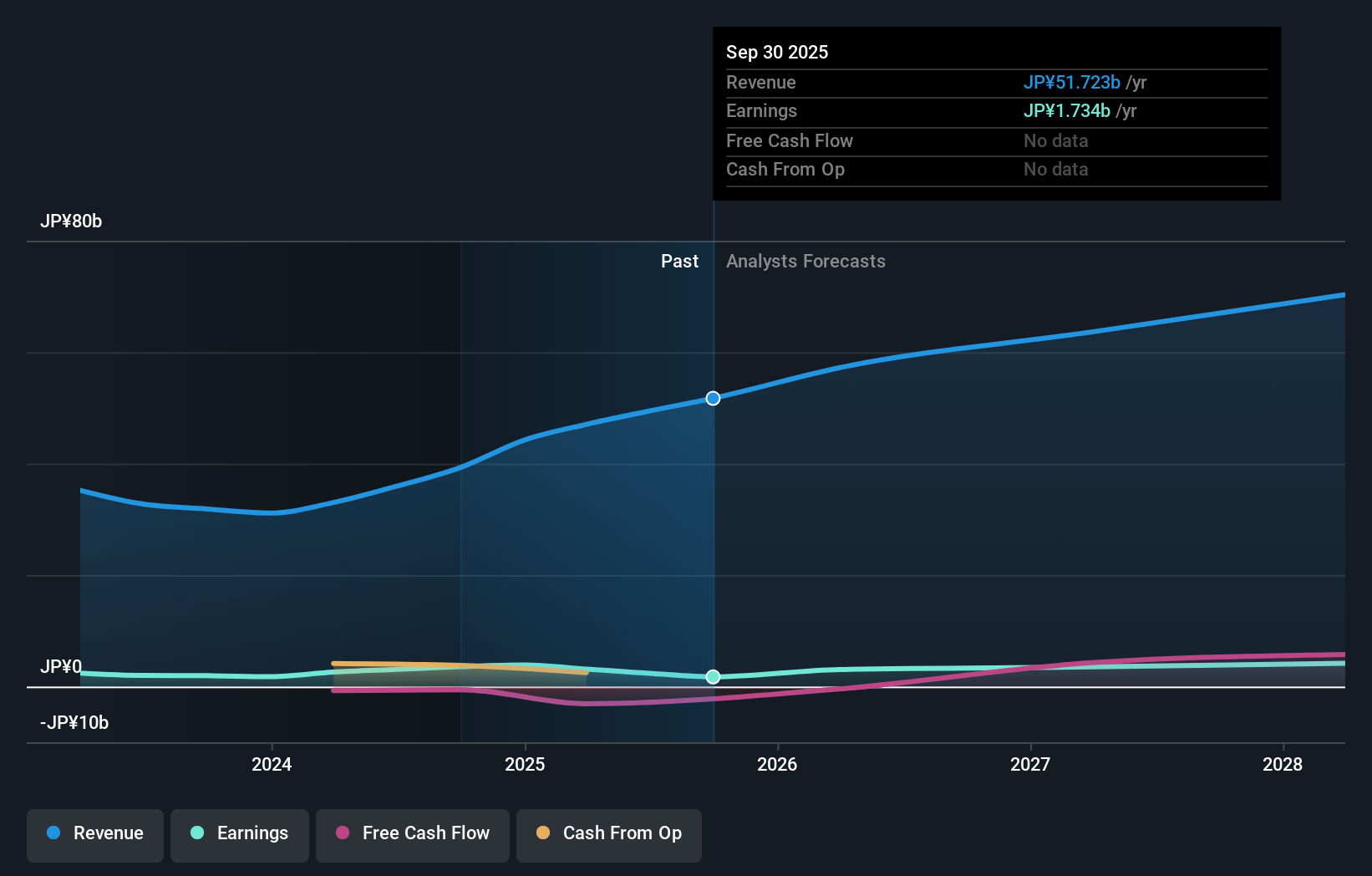

The analysts might have been a bit too bullish on CUC Inc. (TSE:9158), given that the company fell short of expectations when it released its half-yearly results last week. Results showed a clear earnings miss, with JP¥26b revenue coming in 3.6% lower than what the analystsexpected. Statutory earnings per share (EPS) of JP¥13.79 missed the mark badly, arriving some 54% below what was expected. This is an important time for investors, as they can track a company's performance in its report, look at what experts are forecasting for next year, and see if there has been any change to expectations for the business. We thought readers would find it interesting to see the analysts latest (statutory) post-earnings forecasts for next year.

Taking into account the latest results, the consensus forecast from CUC's three analysts is for revenues of JP¥57.2b in 2026. This reflects a notable 11% improvement in revenue compared to the last 12 months. Statutory earnings per share are predicted to leap 76% to JP¥104. In the lead-up to this report, the analysts had been modelling revenues of JP¥57.3b and earnings per share (EPS) of JP¥104 in 2026. The consensus analysts don't seem to have seen anything in these results that would have changed their view on the business, given there's been no major change to their estimates.

Check out our latest analysis for CUC

There were no changes to revenue or earnings estimates or the price target of JP¥1,200, suggesting that the company has met expectations in its recent result.

One way to get more context on these forecasts is to look at how they compare to both past performance, and how other companies in the same industry are performing. It's pretty clear that there is an expectation that CUC's revenue growth will slow down substantially, with revenues to the end of 2026 expected to display 22% growth on an annualised basis. This is compared to a historical growth rate of 32% over the past year. By way of comparison, the other companies in this industry with analyst coverage are forecast to grow their revenue at 4.3% annually. So it's pretty clear that, while CUC's revenue growth is expected to slow, it's still expected to grow faster than the industry itself.

The Bottom Line

The most obvious conclusion is that there's been no major change in the business' prospects in recent times, with the analysts holding their earnings forecasts steady, in line with previous estimates. Happily, there were no major changes to revenue forecasts, with the business still expected to grow faster than the wider industry. The consensus price target held steady at JP¥1,200, with the latest estimates not enough to have an impact on their price targets.

With that in mind, we wouldn't be too quick to come to a conclusion on CUC. Long-term earnings power is much more important than next year's profits. We have estimates - from multiple CUC analysts - going out to 2028, and you can see them free on our platform here.

Don't forget that there may still be risks. For instance, we've identified 3 warning signs for CUC (2 shouldn't be ignored) you should be aware of.

New: AI Stock Screener & Alerts

Our new AI Stock Screener scans the market every day to uncover opportunities.

• Dividend Powerhouses (3%+ Yield)

• Undervalued Small Caps with Insider Buying

• High growth Tech and AI Companies

Or build your own from over 50 metrics.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About TSE:9158

Reasonable growth potential and fair value.

Market Insights

Advertisement

Community Narratives

MINISO's fair value is projected at 26.69 with an anticipated PE ratio shift of 20x

Fair Value US$24.03|9.0% undervalued

BE

Community Contributor

Procter & Gamble: A Dividend Giant Facing Slowing Growth

Fair Value US$119.81|23.5% overvalued

AN

Community Contributor

Eli Lilly's Future Growth Driven by Tirzepatide and Favorable Market Conditions

Fair Value US$1.19k|14.4% undervalued

EA

Community Contributor