- Japan

- /

- Medical Equipment

- /

- TSE:7817

Paramount Bed Holdings (TSE:7817) Will Pay A Larger Dividend Than Last Year At ¥49.00

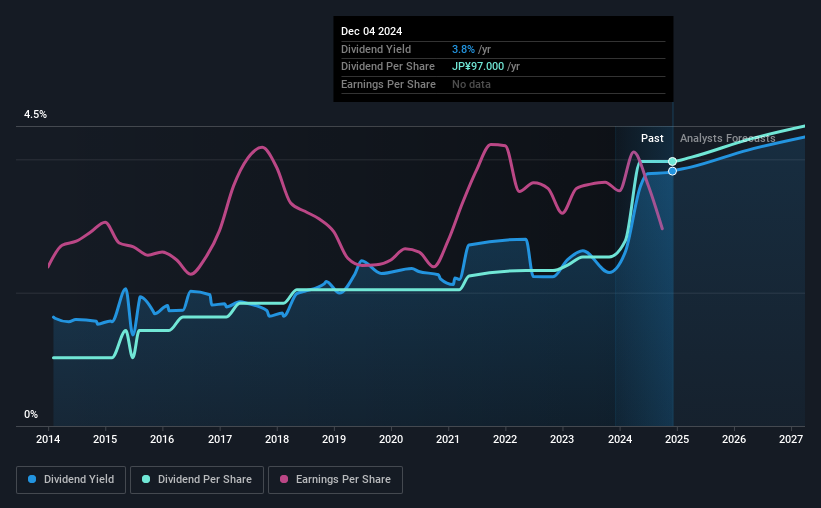

The board of Paramount Bed Holdings Co., Ltd. (TSE:7817) has announced that it will be paying its dividend of ¥49.00 on the 10th of June, an increased payment from last year's comparable dividend. This takes the dividend yield to 3.8%, which shareholders will be pleased with.

Check out our latest analysis for Paramount Bed Holdings

Paramount Bed Holdings' Projected Earnings Seem Likely To Cover Future Distributions

Impressive dividend yields are good, but this doesn't matter much if the payments can't be sustained. Before making this announcement, Paramount Bed Holdings was paying a whopping 120% as a dividend, but this only made up 26% of its overall earnings. While the business may be attempting to set a balanced dividend policy, a cash payout ratio this high might expose the dividend to being cut if the business ran into some challenges.

Over the next year, EPS is forecast to expand by 17.8%. If the dividend continues on this path, the payout ratio could be 67% by next year, which we think can be pretty sustainable going forward.

Paramount Bed Holdings Has A Solid Track Record

The company has been paying a dividend for a long time, and it has been quite stable which gives us confidence in the future dividend potential. The dividend has gone from an annual total of ¥25.00 in 2014 to the most recent total annual payment of ¥97.00. This means that it has been growing its distributions at 15% per annum over that time. We can see that payments have shown some very nice upward momentum without faltering, which provides some reassurance that future payments will also be reliable.

Paramount Bed Holdings May Find It Hard To Grow The Dividend

Some investors will be chomping at the bit to buy some of the company's stock based on its dividend history. Earnings have grown at around 4.2% a year for the past five years, which isn't massive but still better than seeing them shrink. Earnings growth is slow, but on the plus side, the dividend payout ratio is low and dividends could grow faster than earnings, if the company decides to increase its payout ratio.

In Summary

Overall, this is probably not a great income stock, even though the dividend is being raised at the moment. With cash flows lacking, it is difficult to see how the company can sustain a dividend payment. We would probably look elsewhere for an income investment.

Investors generally tend to favour companies with a consistent, stable dividend policy as opposed to those operating an irregular one. Still, investors need to consider a host of other factors, apart from dividend payments, when analysing a company. As an example, we've identified 1 warning sign for Paramount Bed Holdings that you should be aware of before investing. Looking for more high-yielding dividend ideas? Try our collection of strong dividend payers.

New: Manage All Your Stock Portfolios in One Place

We've created the ultimate portfolio companion for stock investors, and it's free.

• Connect an unlimited number of Portfolios and see your total in one currency

• Be alerted to new Warning Signs or Risks via email or mobile

• Track the Fair Value of your stocks

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About TSE:7817

Paramount Bed Holdings

Manufactures and sells beds, mattresses, and equipment for medical and nursing care in Japan.

Flawless balance sheet with solid track record and pays a dividend.

Similar Companies

Market Insights

Community Narratives