- Japan

- /

- Consumer Durables

- /

- TSE:3284

Top Japanese Growth Companies With Insider Ownership In October 2024

Reviewed by Simply Wall St

Japan's stock markets have shown resilience, with the Nikkei 225 Index climbing 2.45% and the TOPIX Index increasing by 0.45% amid yen weakness, which has bolstered the profit outlook for exporters. As investors navigate this favorable backdrop, identifying growth companies with significant insider ownership could be a strategic approach, as these firms may align management interests closely with shareholders and potentially capitalize on current market conditions.

Top 10 Growth Companies With High Insider Ownership In Japan

| Name | Insider Ownership | Earnings Growth |

| Micronics Japan (TSE:6871) | 15.3% | 31.5% |

| Hottolink (TSE:3680) | 26.1% | 61.5% |

| Kasumigaseki CapitalLtd (TSE:3498) | 34.7% | 40.2% |

| Medley (TSE:4480) | 34% | 30.4% |

| Inforich (TSE:9338) | 19.1% | 29.8% |

| Kanamic NetworkLTD (TSE:3939) | 25% | 28.3% |

| ExaWizards (TSE:4259) | 22% | 75.2% |

| Money Forward (TSE:3994) | 21.4% | 68.1% |

| Loadstar Capital K.K (TSE:3482) | 33.8% | 24.3% |

| Soracom (TSE:147A) | 16.5% | 54.1% |

Let's dive into some prime choices out of the screener.

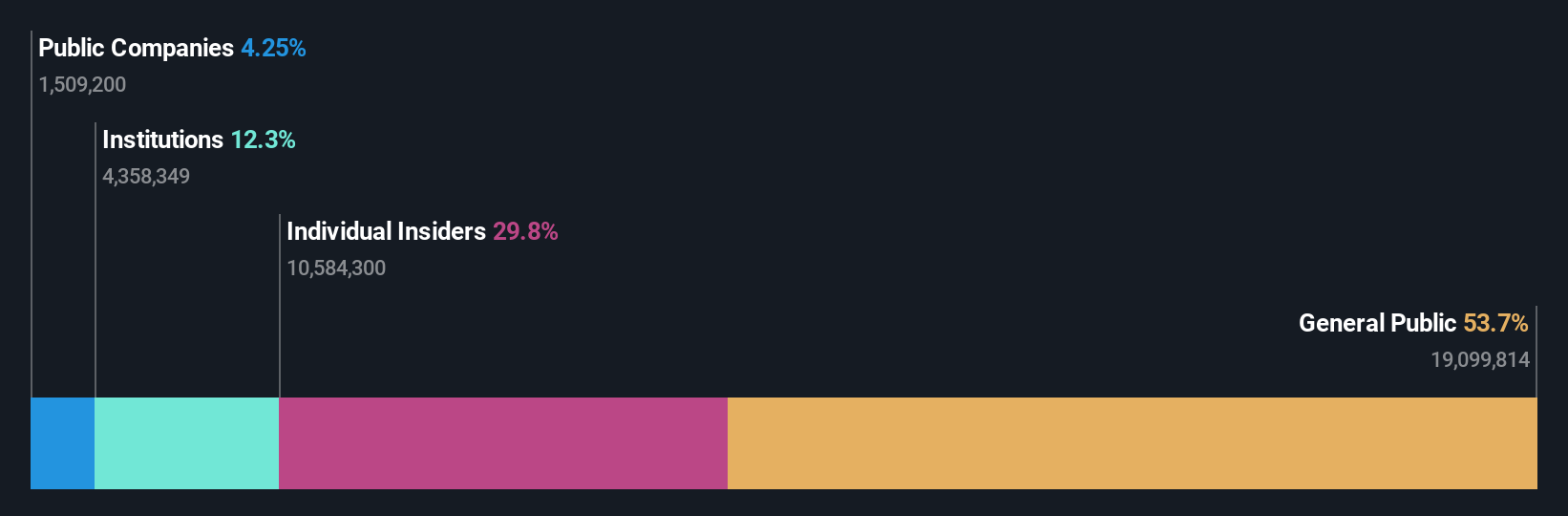

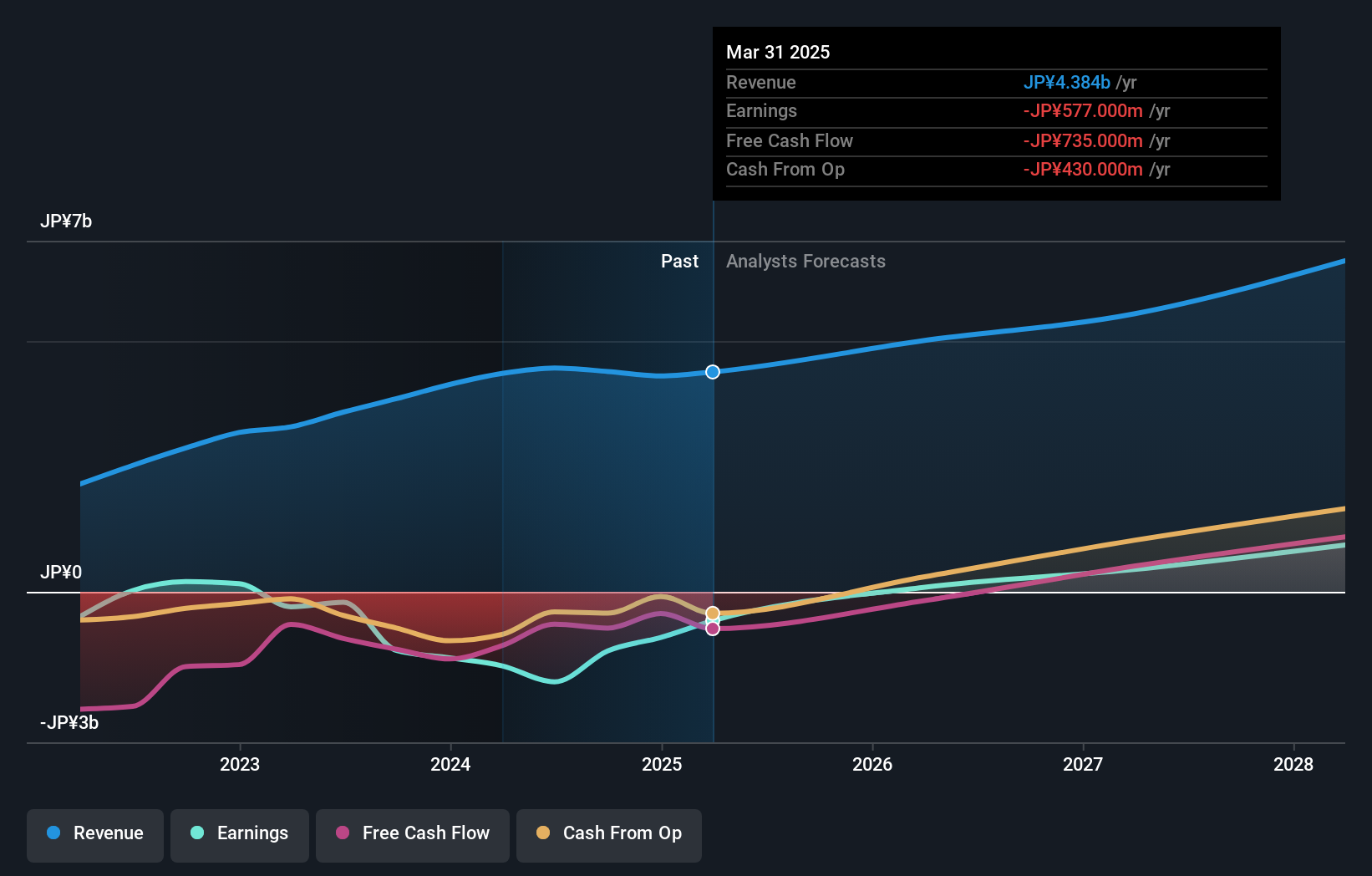

Hoosiers Holdings (TSE:3284)

Simply Wall St Growth Rating: ★★★★☆☆

Overview: Hoosiers Holdings Co., Ltd. is a Japanese holding company that operates, manages, and sells real estate properties, with a market cap of ¥37.44 billion.

Operations: The company's revenue segments comprise ¥11.47 billion from the CCRC Business, ¥15.93 billion from Real Estate Investment, ¥47.01 billion from Real Estate Development Business, and ¥8.13 billion from Real Estate Related Service Business.

Insider Ownership: 29.8%

Revenue Growth Forecast: 10.6% p.a.

Hoosiers Holdings shows promising growth potential with earnings expected to grow significantly at 21.1% annually, outpacing the Japanese market's 8.8%. Although revenue growth is projected at a slower pace of 10.6%, it still surpasses the market average of 4.3%. The company offers good value with a price-to-earnings ratio of 10.4x below the market average, but its dividend yield of ¥5.51% is not well covered by free cash flows, indicating financial constraints in sustaining payouts.

- Unlock comprehensive insights into our analysis of Hoosiers Holdings stock in this growth report.

- Our comprehensive valuation report raises the possibility that Hoosiers Holdings is priced higher than what may be justified by its financials.

WealthNavi (TSE:7342)

Simply Wall St Growth Rating: ★★★★★☆

Overview: WealthNavi Inc. develops and delivers an online asset management and risk management platform, with a market cap of ¥66.71 billion.

Operations: WealthNavi Inc.'s revenue segments are not specified in the provided text.

Insider Ownership: 18%

Revenue Growth Forecast: 20.8% p.a.

WealthNavi is experiencing significant growth, with earnings expected to increase 75.8% annually, far surpassing the Japanese market's average of 8.8%. Revenue is also projected to grow rapidly at 20.8% per year. Despite past shareholder dilution and a decline in profit margins from 5.8% to 3.3%, WealthNavi's strategic office relocation supports its expansion goals in the robo-advisor sector, aiming for enhanced business operations and increased employee capacity.

- Click to explore a detailed breakdown of our findings in WealthNavi's earnings growth report.

- Insights from our recent valuation report point to the potential overvaluation of WealthNavi shares in the market.

CYBERDYNE (TSE:7779)

Simply Wall St Growth Rating: ★★★★☆☆

Overview: CYBERDYNE Inc. is engaged in the research, development, production, sale, leasing, and maintenance of robotic equipment and systems for medical and welfare applications across various regions including Japan, the United States, Europe, the Middle East, Africa, and Asia Pacific countries with a market cap of ¥38.43 billion.

Operations: The company's revenue primarily originates from its robot-related business, which generated ¥4.46 billion.

Insider Ownership: 39%

Revenue Growth Forecast: 17.7% p.a.

Cyberdyne's earnings are forecast to grow significantly at 64.03% annually, outpacing the Japanese market's average growth rate. Although revenue is projected to increase at 17.7% per year, which is slower than the desired 20%, it still exceeds the market average of 4.3%. Despite a low expected return on equity of 0.9% in three years, Cyberdyne's path to profitability within this timeframe suggests strong growth potential without substantial recent insider trading activity.

- Click here to discover the nuances of CYBERDYNE with our detailed analytical future growth report.

- Our expertly prepared valuation report CYBERDYNE implies its share price may be too high.

Turning Ideas Into Actions

- Dive into all 101 of the Fast Growing Japanese Companies With High Insider Ownership we have identified here.

- Are you invested in these stocks already? Keep abreast of every twist and turn by setting up a portfolio with Simply Wall St, where we make it simple for investors like you to stay informed and proactive.

- Unlock the power of informed investing with Simply Wall St, your free guide to navigating stock markets worldwide.

Ready To Venture Into Other Investment Styles?

- Explore high-performing small cap companies that haven't yet garnered significant analyst attention.

- Diversify your portfolio with solid dividend payers offering reliable income streams to weather potential market turbulence.

- Find companies with promising cash flow potential yet trading below their fair value.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.The analysis only considers stock directly held by insiders. It does not include indirectly owned stock through other vehicles such as corporate and/or trust entities. All forecast revenue and earnings growth rates quoted are in terms of annualised (per annum) growth rates over 1-3 years.

If you're looking to trade Hoosiers Holdings, open an account with the lowest-cost platform trusted by professionals, Interactive Brokers.

With clients in over 200 countries and territories, and access to 160 markets, IBKR lets you trade stocks, options, futures, forex, bonds and funds from a single integrated account.

Enjoy no hidden fees, no account minimums, and FX conversion rates as low as 0.03%, far better than what most brokers offer.

Sponsored ContentValuation is complex, but we're here to simplify it.

Discover if Hoosiers Holdings might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About TSE:3284

Hoosiers Holdings

A holding company, operates, manages, and sells real estate properties in Japan.

Proven track record average dividend payer.

Market Insights

Community Narratives