There's No Escaping MEGMILK SNOW BRAND Co.,Ltd.'s (TSE:2270) Muted Earnings Despite A 26% Share Price Rise

MEGMILK SNOW BRAND Co.,Ltd. (TSE:2270) shares have continued their recent momentum with a 26% gain in the last month alone. The last 30 days bring the annual gain to a very sharp 52%.

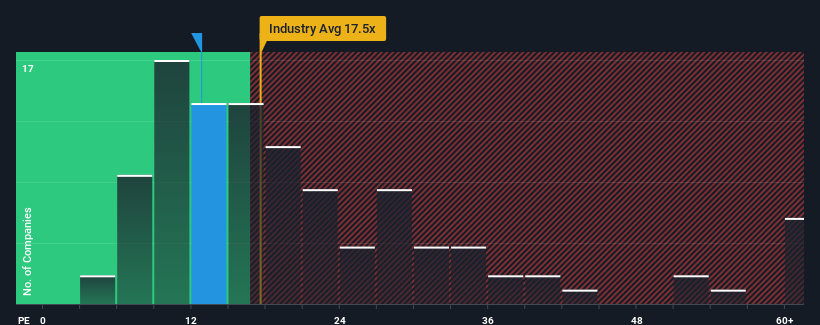

Although its price has surged higher, given about half the companies in Japan have price-to-earnings ratios (or "P/E's") above 15x, you may still consider MEGMILK SNOW BRANDLtd as an attractive investment with its 12.8x P/E ratio. Nonetheless, we'd need to dig a little deeper to determine if there is a rational basis for the reduced P/E.

MEGMILK SNOW BRANDLtd certainly has been doing a good job lately as it's been growing earnings more than most other companies. It might be that many expect the strong earnings performance to degrade substantially, which has repressed the P/E. If not, then existing shareholders have reason to be quite optimistic about the future direction of the share price.

See our latest analysis for MEGMILK SNOW BRANDLtd

Does Growth Match The Low P/E?

The only time you'd be truly comfortable seeing a P/E as low as MEGMILK SNOW BRANDLtd's is when the company's growth is on track to lag the market.

Taking a look back first, we see that the company grew earnings per share by an impressive 126% last year. As a result, it also grew EPS by 8.7% in total over the last three years. Therefore, it's fair to say the earnings growth recently has been respectable for the company.

Looking ahead now, EPS is anticipated to slump, contracting by 1.1% each year during the coming three years according to the four analysts following the company. That's not great when the rest of the market is expected to grow by 10% each year.

In light of this, it's understandable that MEGMILK SNOW BRANDLtd's P/E would sit below the majority of other companies. Nonetheless, there's no guarantee the P/E has reached a floor yet with earnings going in reverse. There's potential for the P/E to fall to even lower levels if the company doesn't improve its profitability.

The Final Word

MEGMILK SNOW BRANDLtd's stock might have been given a solid boost, but its P/E certainly hasn't reached any great heights. While the price-to-earnings ratio shouldn't be the defining factor in whether you buy a stock or not, it's quite a capable barometer of earnings expectations.

As we suspected, our examination of MEGMILK SNOW BRANDLtd's analyst forecasts revealed that its outlook for shrinking earnings is contributing to its low P/E. At this stage investors feel the potential for an improvement in earnings isn't great enough to justify a higher P/E ratio. Unless these conditions improve, they will continue to form a barrier for the share price around these levels.

There are also other vital risk factors to consider and we've discovered 2 warning signs for MEGMILK SNOW BRANDLtd (1 is a bit concerning!) that you should be aware of before investing here.

Of course, you might also be able to find a better stock than MEGMILK SNOW BRANDLtd. So you may wish to see this free collection of other companies that have reasonable P/E ratios and have grown earnings strongly.

If you're looking to trade MEGMILK SNOW BRANDLtd, open an account with the lowest-cost platform trusted by professionals, Interactive Brokers.

With clients in over 200 countries and territories, and access to 160 markets, IBKR lets you trade stocks, options, futures, forex, bonds and funds from a single integrated account.

Enjoy no hidden fees, no account minimums, and FX conversion rates as low as 0.03%, far better than what most brokers offer.

Sponsored ContentNew: Manage All Your Stock Portfolios in One Place

We've created the ultimate portfolio companion for stock investors, and it's free.

• Connect an unlimited number of Portfolios and see your total in one currency

• Be alerted to new Warning Signs or Risks via email or mobile

• Track the Fair Value of your stocks

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About TSE:2270

MEGMILK SNOW BRANDLtd

Manufactures and sells milk, milk products, and other food products in Japan and internationally.

Flawless balance sheet established dividend payer.

Market Insights

Community Narratives