Advertisement

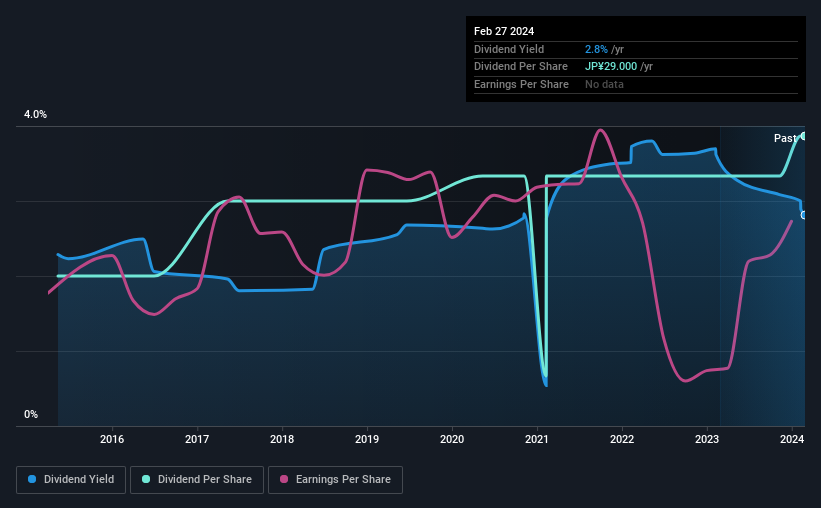

Feed One Co.,Ltd. (TSE:2060) will increase its dividend from last year's comparable payment on the 10th of June to ¥14.50. This takes the dividend yield to 2.8%, which shareholders will be pleased with.

While the dividend yield is important for income investors, it is also important to consider any large share price moves, as this will generally outweigh any gains from distributions. Investors will be pleased to see that Feed OneLtd's stock price has increased by 31% in the last 3 months, which is good for shareholders and can also explain a decrease in the dividend yield.

See our latest analysis for Feed OneLtd

Feed OneLtd's Dividend Is Well Covered By Earnings

We like to see robust dividend yields, but that doesn't matter if the payment isn't sustainable. Before making this announcement, Feed OneLtd was easily earning enough to cover the dividend. This means that most of its earnings are being retained to grow the business.

Looking forward, EPS could fall by 4.4% if the company can't turn things around from the last few years. Assuming the dividend continues along recent trends, we believe the payout ratio could be 31%, which we are pretty comfortable with and we think is feasible on an earnings basis.

Feed OneLtd's Dividend Has Lacked Consistency

It's comforting to see that Feed OneLtd has been paying a dividend for a number of years now, however it has been cut at least once in that time. This suggests that the dividend might not be the most reliable. Since 2015, the annual payment back then was ¥15.00, compared to the most recent full-year payment of ¥29.00. This works out to be a compound annual growth rate (CAGR) of approximately 7.6% a year over that time. A reasonable rate of dividend growth is good to see, but we're wary that the dividend history is not as solid as we'd like, having been cut at least once.

The Dividend's Growth Prospects Are Limited

With a relatively unstable dividend, it's even more important to evaluate if earnings per share is growing, which could point to a growing dividend in the future. Feed OneLtd has seen earnings per share falling at 4.4% per year over the last five years. If the company is making less over time, it naturally follows that it will also have to pay out less in dividends.

In Summary

Overall, this is probably not a great income stock, even though the dividend is being raised at the moment. The company is generating plenty of cash, which could maintain the dividend for a while, but the track record hasn't been great. We don't think Feed OneLtd is a great stock to add to your portfolio if income is your focus.

Companies possessing a stable dividend policy will likely enjoy greater investor interest than those suffering from a more inconsistent approach. However, there are other things to consider for investors when analysing stock performance. Just as an example, we've come across 2 warning signs for Feed OneLtd you should be aware of, and 1 of them is concerning. If you are a dividend investor, you might also want to look at our curated list of high yield dividend stocks.

New: AI Stock Screener & Alerts

Our new AI Stock Screener scans the market every day to uncover opportunities.

• Dividend Powerhouses (3%+ Yield)

• Undervalued Small Caps with Insider Buying

• High growth Tech and AI Companies

Or build your own from over 50 metrics.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About TSE:2060

Feed OneLtd

Feed One Co.,Ltd. procures, produces, processes, markets, and sells meat, egg, seafood, and compound feed in Japan and internationally.

Flawless balance sheet with solid track record and pays a dividend.

Market Insights

Advertisement

Community Narratives

Alphabet: The Under-appreciated Compounder Hiding in Plain Sight

Fair Value US$282.83|31.8% undervalued

BL

Community Contributor

Planet Labs: At The Heart Of The Emerging New Space Boom

Fair Value US$11.31|44.7% undervalued

AN

Community Contributor

Exxon in Guyana 5 year forecast Low $135 to High $189

Fair Value US$189.00|40.9% undervalued

AG

Community Contributor