Advertisement

- Japan

- /

- Diversified Financial

- /

- TSE:8771

With A 25% Price Drop For eGuarantee, Inc. (TSE:8771) You'll Still Get What You Pay For

Unfortunately for some shareholders, the eGuarantee, Inc. (TSE:8771) share price has dived 25% in the last thirty days, prolonging recent pain. Instead of being rewarded, shareholders who have already held through the last twelve months are now sitting on a 32% share price drop.

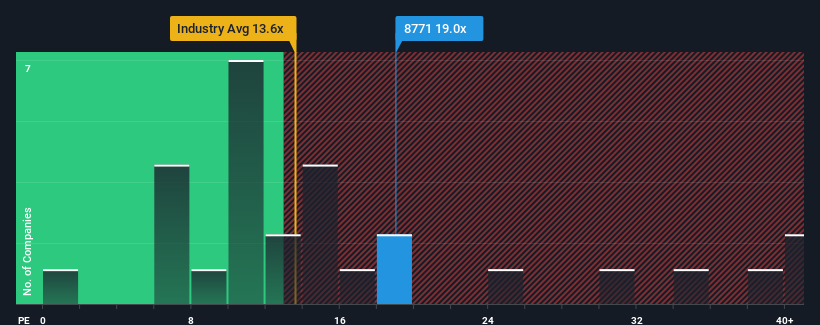

Even after such a large drop in price, given around half the companies in Japan have price-to-earnings ratios (or "P/E's") below 14x, you may still consider eGuarantee as a stock to potentially avoid with its 19x P/E ratio. Although, it's not wise to just take the P/E at face value as there may be an explanation why it's as high as it is.

eGuarantee's earnings growth of late has been pretty similar to most other companies. It might be that many expect the mediocre earnings performance to strengthen positively, which has kept the P/E from falling. You'd really hope so, otherwise you're paying a pretty hefty price for no particular reason.

See our latest analysis for eGuarantee

Is There Enough Growth For eGuarantee?

There's an inherent assumption that a company should outperform the market for P/E ratios like eGuarantee's to be considered reasonable.

Taking a look back first, we see that the company managed to grow earnings per share by a handy 13% last year. Pleasingly, EPS has also lifted 52% in aggregate from three years ago, partly thanks to the last 12 months of growth. Therefore, it's fair to say the earnings growth recently has been superb for the company.

Turning to the outlook, the next three years should generate growth of 12% per year as estimated by the three analysts watching the company. Meanwhile, the rest of the market is forecast to only expand by 9.6% per annum, which is noticeably less attractive.

In light of this, it's understandable that eGuarantee's P/E sits above the majority of other companies. Apparently shareholders aren't keen to offload something that is potentially eyeing a more prosperous future.

The Key Takeaway

There's still some solid strength behind eGuarantee's P/E, if not its share price lately. Generally, our preference is to limit the use of the price-to-earnings ratio to establishing what the market thinks about the overall health of a company.

As we suspected, our examination of eGuarantee's analyst forecasts revealed that its superior earnings outlook is contributing to its high P/E. At this stage investors feel the potential for a deterioration in earnings isn't great enough to justify a lower P/E ratio. Unless these conditions change, they will continue to provide strong support to the share price.

You should always think about risks. Case in point, we've spotted 1 warning sign for eGuarantee you should be aware of.

If P/E ratios interest you, you may wish to see this free collection of other companies with strong earnings growth and low P/E ratios.

New: Manage All Your Stock Portfolios in One Place

We've created the ultimate portfolio companion for stock investors, and it's free.

• Connect an unlimited number of Portfolios and see your total in one currency

• Be alerted to new Warning Signs or Risks via email or mobile

• Track the Fair Value of your stocks

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About TSE:8771

eGuarantee

Engages in credit risk entrustment and securitization business in Japan.

Flawless balance sheet established dividend payer.

Market Insights

Advertisement

Community Narratives

Finding The True Value Of A Logistics Powerhouse

Fair Value US$95.21|8.4% undervalued

NV

Community Contributor

Paradigm Biopharmaceuticals Will Lead Osteoarthritis Treatment with Zilosul's FDA Success

Fair Value AU$5.50|92.1% undervalued

AM

Community Contributor

Barrick Mining (ABX:CA): A Gold Hedge against a U.S. Shutdown

Fair Value CA$60.00|24.2% undervalued

GM

Community Contributor