Advertisement

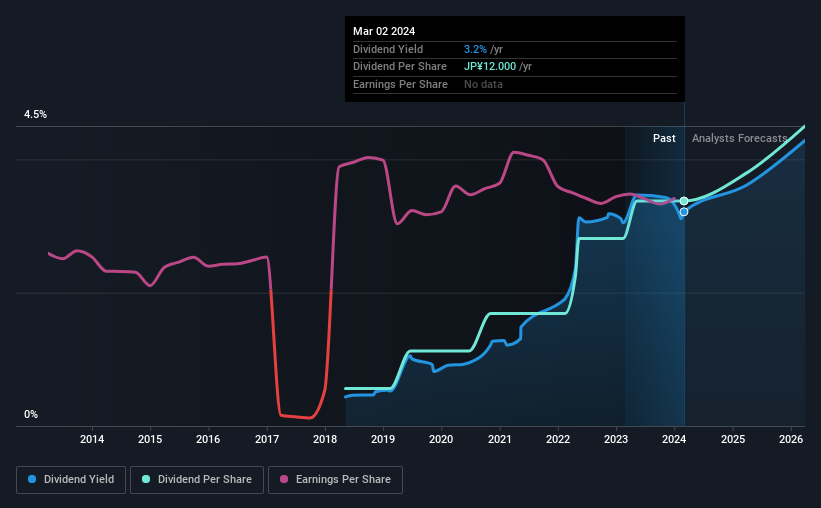

The board of Acom Co., Ltd. (TSE:8572) has announced that it will pay a dividend on the 26th of June, with investors receiving ¥6.00 per share. The payment will take the dividend yield to 3.2%, which is in line with the average for the industry.

See our latest analysis for Acom

Acom's Dividend Is Well Covered By Earnings

While it is always good to see a solid dividend yield, we should also consider whether the payment is feasible. Based on the last payment, Acom was earning enough to cover the dividend, but free cash flows weren't positive. In general, we consider cash flow to be more important than earnings, so we would be cautious about relying on the sustainability of this dividend.

Over the next year, EPS is forecast to expand by 8.6%. Assuming the dividend continues along recent trends, we think the payout ratio could be 44% by next year, which is in a pretty sustainable range.

Acom Is Still Building Its Track Record

Even though the company has been paying a consistent dividend for a while, we would like to see a few more years before we feel comfortable relying on it. Since 2018, the annual payment back then was ¥2.00, compared to the most recent full-year payment of ¥12.00. This implies that the company grew its distributions at a yearly rate of about 35% over that duration. We're not overly excited about the relatively short history of dividend payments, however the dividend is growing at a nice rate and we might take a closer look.

Dividend Growth Is Doubtful

Investors could be attracted to the stock based on the quality of its payment history. However, initial appearances might be deceiving. Over the past five years, it looks as though Acom's EPS has declined at around 6.8% a year. Declining earnings will inevitably lead to the company paying a lower dividend in line with lower profits. However, the next year is actually looking up, with earnings set to rise. We would just wait until it becomes a pattern before getting too excited.

Acom's Dividend Doesn't Look Sustainable

Overall, we always like to see the dividend being raised, but we don't think Acom will make a great income stock. While Acom is earning enough to cover the payments, the cash flows are lacking. We would probably look elsewhere for an income investment.

Investors generally tend to favour companies with a consistent, stable dividend policy as opposed to those operating an irregular one. At the same time, there are other factors our readers should be conscious of before pouring capital into a stock. To that end, Acom has 2 warning signs (and 1 which doesn't sit too well with us) we think you should know about. Looking for more high-yielding dividend ideas? Try our collection of strong dividend payers.

New: Manage All Your Stock Portfolios in One Place

We've created the ultimate portfolio companion for stock investors, and it's free.

• Connect an unlimited number of Portfolios and see your total in one currency

• Be alerted to new Warning Signs or Risks via email or mobile

• Track the Fair Value of your stocks

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About TSE:8572

Acom

Offers loans, credit cards, and loan guarantee services in Japan and internationally.

Adequate balance sheet with moderate growth potential.

Market Insights

Advertisement

Community Narratives

A case for TSXV:USA to reach USD $5.00 - $9.00 (CAD $7.30–$12.29) by 2029.

Fair Value CA$12.29|91.2% undervalued

AG

Community Contributor

DLocal's Future Growth Fueled by 35% Revenue and Profit Margin Boosts

Fair Value US$195.39|94.1% undervalued

WY

Community Contributor

Historically Cheap, but the Margin of Safety Is Still Thin

Fair Value SEK 232.58|13.2% undervalued

MA

Community Contributor