Advertisement

VIA Holdings,Inc. (TSE:7918) announced strong profits, but the stock was stagnant. We did some digging, and we found some concerning factors in the details.

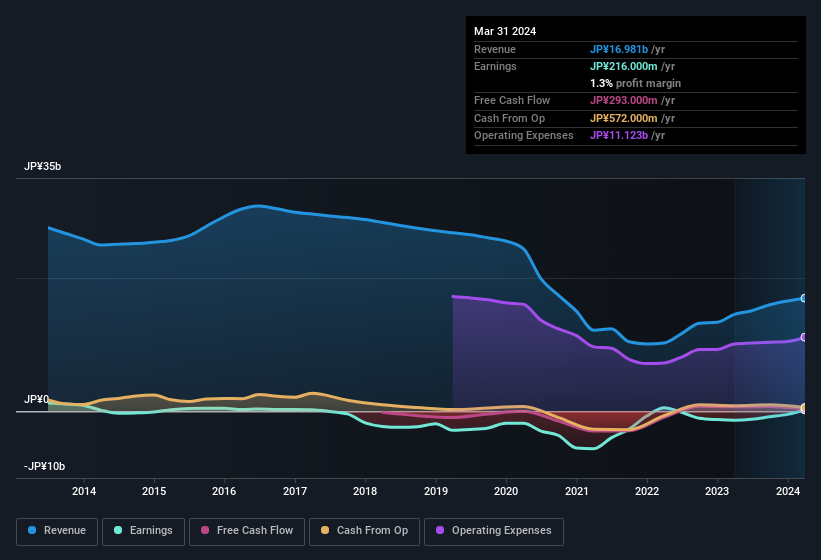

Check out our latest analysis for VIA HoldingsInc

One essential aspect of assessing earnings quality is to look at how much a company is diluting shareholders. VIA HoldingsInc expanded the number of shares on issue by 15% over the last year. Therefore, each share now receives a smaller portion of profit. Per share metrics like EPS help us understand how much actual shareholders are benefitting from the company's profits, while the net income level gives us a better view of the company's absolute size. You can see a chart of VIA HoldingsInc's EPS by clicking here.

How Is Dilution Impacting VIA HoldingsInc's Earnings Per Share (EPS)?

VIA HoldingsInc was losing money three years ago. And even focusing only on the last twelve months, we don't have a meaningful growth rate because it made a loss a year ago, too. But mathematics aside, it is always good to see when a formerly unprofitable business come good (though we accept profit would have been higher if dilution had not been required). So you can see that the dilution has had a bit of an impact on shareholders.

In the long term, if VIA HoldingsInc's earnings per share can increase, then the share price should too. However, if its profit increases while its earnings per share stay flat (or even fall) then shareholders might not see much benefit. For the ordinary retail shareholder, EPS is a great measure to check your hypothetical "share" of the company's profit.

Note: we always recommend investors check balance sheet strength. Click here to be taken to our balance sheet analysis of VIA HoldingsInc.

How Do Unusual Items Influence Profit?

On top of the dilution, we should also consider the JP¥55m impact of unusual items in the last year, which had the effect of suppressing profit. It's never great to see unusual items costing the company profits, but on the upside, things might improve sooner rather than later. We looked at thousands of listed companies and found that unusual items are very often one-off in nature. And that's hardly a surprise given these line items are considered unusual. Assuming those unusual expenses don't come up again, we'd therefore expect VIA HoldingsInc to produce a higher profit next year, all else being equal.

Our Take On VIA HoldingsInc's Profit Performance

To sum it all up, VIA HoldingsInc took a hit from unusual items which pushed its profit down; without that, it would have made more money. But unfortunately the dilution means that shareholders now own a smaller proportion of the company (assuming they maintained the same number of shares). That will weigh on earnings per share, even if it is not reflected in net income. Based on these factors, it's hard to tell if VIA HoldingsInc's profits are a reasonable reflection of its underlying profitability. So while earnings quality is important, it's equally important to consider the risks facing VIA HoldingsInc at this point in time. For example, VIA HoldingsInc has 4 warning signs (and 1 which is a bit concerning) we think you should know about.

Our examination of VIA HoldingsInc has focussed on certain factors that can make its earnings look better than they are. But there is always more to discover if you are capable of focussing your mind on minutiae. Some people consider a high return on equity to be a good sign of a quality business. So you may wish to see this free collection of companies boasting high return on equity, or this list of stocks with high insider ownership.

New: Manage All Your Stock Portfolios in One Place

We've created the ultimate portfolio companion for stock investors, and it's free.

• Connect an unlimited number of Portfolios and see your total in one currency

• Be alerted to new Warning Signs or Risks via email or mobile

• Track the Fair Value of your stocks

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About TSE:7918

Low with questionable track record.

Market Insights

Advertisement

Community Narratives

BMW cruising ahead with new EVs and premium models to boost revenue 5%

Fair Value €135.07|44.5% undervalued

UN

Community Contributor

EU#2 - From Humble Beginnings to Global Powerhouse

Fair Value DKK 851.04|46.1% undervalued

TO

Community Contributor