Advertisement

- Japan

- /

- Hospitality

- /

- TSE:7581

Saizeriya (TSE:7581) Valuation in Focus After Higher Dividend and Fresh Earnings Forecasts

Simply Wall St

Reviewed by Kshitija Bhandaru

SaizeriyaLtd (TSE:7581) just updated investors with new earnings forecasts and announced a higher cash dividend for the latest fiscal year. This provides a fresh perspective on both its financial performance and upcoming shareholder returns.

See our latest analysis for SaizeriyaLtd.

SaizeriyaLtd’s share price recently surged nearly 12% for the week, with momentum building following fresh earnings forecasts and a newly announced dividend hike. While the stock’s year-to-date price return is slightly down, its three-year total shareholder return of 101% highlights impressive longer-term gains and continued confidence in its outlook.

If this kind of momentum gets you thinking about what else is out there, why not see which other companies are being snapped up by insiders and showing rapid growth using our fast growing stocks with high insider ownership

But with bullish forecasts and a strong three-year run now out in the open, is SaizeriyaLtd still trading below its true value? Or has the recent rally already factored in the company’s growth story?

Price-to-Earnings of 23.8x: Is it justified?

SaizeriyaLtd's shares are trading at a price-to-earnings (P/E) ratio of 23.8x, placing it below both the peer average (56x) and the hospitality industry average (24.2x). With the last close at ¥5,400, this suggests investors are paying less per unit of earnings than they would for comparable stocks, potentially indicating relative undervaluation.

The P/E ratio compares a company's current share price to its earnings per share, providing a quick measure of how much investors are willing to pay for future earnings. For hospitality companies like SaizeriyaLtd, this ratio is crucial since it reflects expectations for profitability and growth against industry standards.

Trading at 23.8x earnings appears compelling given its recent profitability surge and steady growth profile. The figure is not only lower than peers, which may signal an overlooked opportunity, but is also just slightly below the estimated fair P/E ratio of 24.4x. This could serve as the level the market gravitates toward if positive momentum continues.

Explore the SWS fair ratio for SaizeriyaLtd

Result: Price-to-Earnings of 23.8x (UNDERVALUED)

However, revenue and net income growth remain modest. As a result, any slowdown or industry headwinds could quickly challenge the current momentum.

Find out about the key risks to this SaizeriyaLtd narrative.

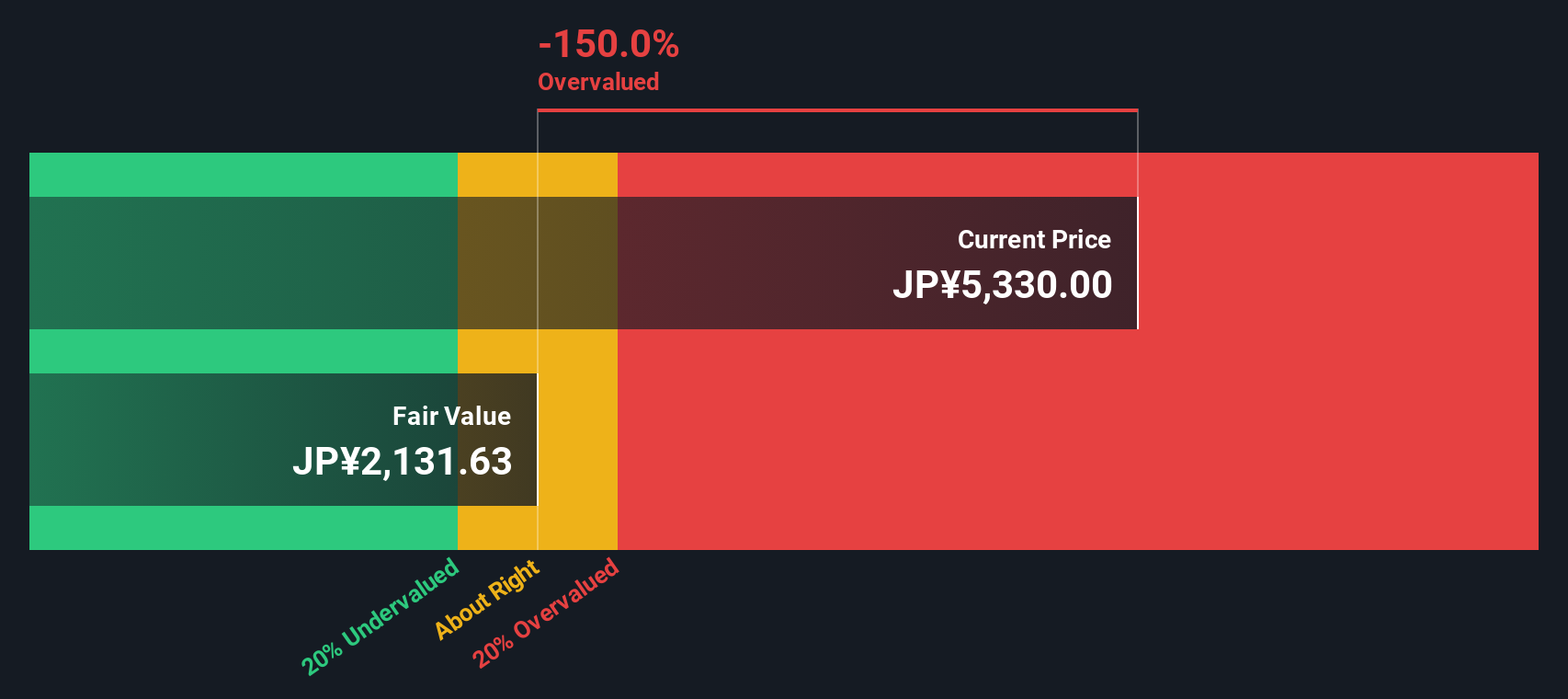

Another View: Discounted Cash Flow Says the Stock is Overvalued

While SaizeriyaLtd looks attractively priced by its earnings ratio, our DCF model estimates the current share price is actually above its fair value. According to the model, the fair value is ¥3,606.48. This method suggests investors might be paying a premium for expected growth. Could the market be too optimistic?

Look into how the SWS DCF model arrives at its fair value.

Simply Wall St performs a discounted cash flow (DCF) on every stock in the world every day (check out SaizeriyaLtd for example). We show the entire calculation in full. You can track the result in your watchlist or portfolio and be alerted when this changes, or use our stock screener to discover undervalued stocks based on their cash flows. If you save a screener we even alert you when new companies match - so you never miss a potential opportunity.

Build Your Own SaizeriyaLtd Narrative

If you'd rather dive deeper and reach your own conclusions, you can analyze the data yourself and craft a personalized view in just minutes, so why not Do it your way

A great starting point for your SaizeriyaLtd research is our analysis highlighting 4 key rewards and 1 important warning sign that could impact your investment decision.

Looking for more investment ideas?

Smart investors never limit their watchlist to just one stock. Make sure you catch tomorrow’s biggest winners by searching across different strategies right now.

- Tap into high-yield opportunities when you scan these 18 dividend stocks with yields > 3% for reliable income streams above 3% in today’s market.

- Spot the potential breakthroughs driving healthcare innovation with these 33 healthcare AI stocks as medicine and AI intersect for better patient outcomes.

- Stay ahead of the tech curve and ride the AI wave by selecting these 24 AI penny stocks with promising growth in artificial intelligence applications.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

New: Manage All Your Stock Portfolios in One Place

We've created the ultimate portfolio companion for stock investors, and it's free.

• Connect an unlimited number of Portfolios and see your total in one currency

• Be alerted to new Warning Signs or Risks via email or mobile

• Track the Fair Value of your stocks

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About TSE:7581

Flawless balance sheet with proven track record.

Similar Companies

Market Insights

Advertisement

Community Narratives

Kodiak AI - a potential 100 bagger opportunity?

Fair Value US$14.00|44.7% undervalued

DA

Community Contributor

A Fair Price for a Great Business Facing Real Threats

Fair Value US$383.06|13.0% undervalued

IM

Community Contributor

AXON And Shopify Integration Will Unlock Global Mobile Advertising

Fair Value US$646.30|7.3% undervalued

AN

Based on Analyst Price Targets