Advertisement

- Japan

- /

- Consumer Services

- /

- TSE:7366

What You Need To Know About The LITALICO Inc. (TSE:7366) Analyst Downgrade Today

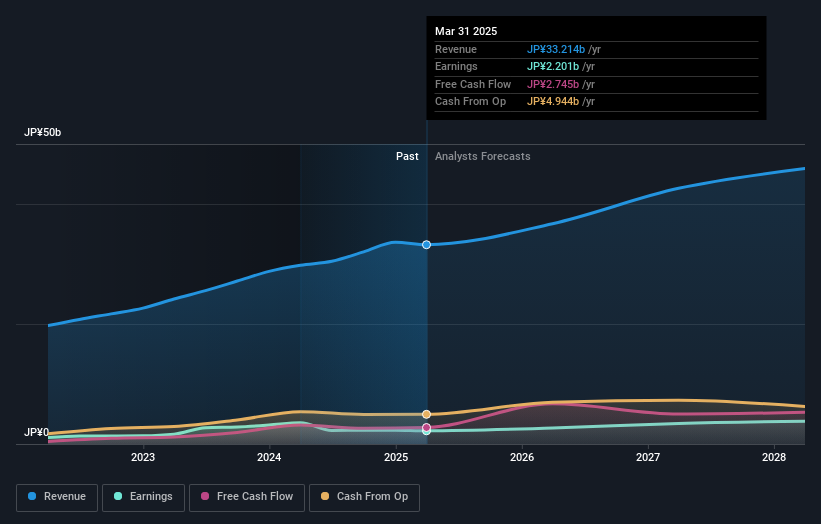

One thing we could say about the analysts on LITALICO Inc. (TSE:7366) - they aren't optimistic, having just made a major negative revision to their near-term (statutory) forecasts for the organization. There was a fairly draconian cut to their revenue estimates, perhaps an implicit admission that previous forecasts were much too optimistic. The stock price has risen 5.3% to JP¥1,316 over the past week. It will be interesting to see if this downgrade motivates investors to start selling their holdings.

Following the downgrade, the latest consensus from LITALICO's three analysts is for revenues of JP¥37b in 2026, which would reflect a notable 11% improvement in sales compared to the last 12 months. Statutory earnings per share are presumed to surge 21% to JP¥74.70. Previously, the analysts had been modelling revenues of JP¥41b and earnings per share (EPS) of JP¥75.43 in 2026. So there's been a clear change in analyst sentiment in the recent update, with the analysts making a substantial drop in revenues and reconfirming their earnings per share estimates.

View our latest analysis for LITALICO

The average price target was steady at JP¥1,570 even though revenue estimates declined; likely suggesting the analysts place a higher value on earnings.

Another way we can view these estimates is in the context of the bigger picture, such as how the forecasts stack up against past performance, and whether forecasts are more or less bullish relative to other companies in the industry. It's pretty clear that there is an expectation that LITALICO's revenue growth will slow down substantially, with revenues to the end of 2026 expected to display 11% growth on an annualised basis. This is compared to a historical growth rate of 19% over the past five years. Juxtapose this against the other companies in the industry with analyst coverage, which are forecast to grow their revenues (in aggregate) 9.3% annually. Factoring in the forecast slowdown in growth, it looks like LITALICO is forecast to grow at about the same rate as the wider industry.

The Bottom Line

The most obvious conclusion from this consensus update is that there's been no major change in the business' prospects in recent times, with analysts holding earnings per share steady, in line with previous estimates. There was also a drop in their revenue estimates, although as we saw earlier, forecast growth is only expected to be about the same as the wider market. Overall, given the drastic downgrade to this year's forecasts, we'd be feeling a little more wary of LITALICO going forwards.

Unfortunately, the earnings downgrade - if accurate - may also place pressure on LITALICO's mountain of debt, which could lead to some belt tightening for shareholders. To see more of our financial analysis, you can click through to our free platform to learn more about its balance sheet and specific concerns we've identified.

Another thing to consider is whether management and directors have been buying or selling stock recently. We provide an overview of all open market stock trades for the last twelve months on our platform, here.

New: AI Stock Screener & Alerts

Our new AI Stock Screener scans the market every day to uncover opportunities.

• Dividend Powerhouses (3%+ Yield)

• Undervalued Small Caps with Insider Buying

• High growth Tech and AI Companies

Or build your own from over 50 metrics.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About TSE:7366

LITALICO

Engages in the employment support, child welfare, platform, and overseas business in Japan.

Good value with reasonable growth potential.

Market Insights

Advertisement

Community Narratives

MINISO's fair value is projected at 26.69 with an anticipated PE ratio shift of 20x

Fair Value US$24.03|11.0% undervalued

BE

Community Contributor

Procter & Gamble: A Dividend Giant Facing Slowing Growth

Fair Value US$119.81|23.3% overvalued

AN

Community Contributor

Eli Lilly's Future Growth Driven by Tirzepatide and Favorable Market Conditions

Fair Value US$1.19k|13.8% undervalued

EA

Community Contributor