Advertisement

- Japan

- /

- Food and Staples Retail

- /

- TSE:9259

Capital Investments At TAKAYOSHI Holdings (TSE:9259) Point To A Promising Future

Did you know there are some financial metrics that can provide clues of a potential multi-bagger? Firstly, we'll want to see a proven return on capital employed (ROCE) that is increasing, and secondly, an expanding base of capital employed. Put simply, these types of businesses are compounding machines, meaning they are continually reinvesting their earnings at ever-higher rates of return. So, when we ran our eye over TAKAYOSHI Holdings' (TSE:9259) trend of ROCE, we really liked what we saw.

Return On Capital Employed (ROCE): What Is It?

If you haven't worked with ROCE before, it measures the 'return' (pre-tax profit) a company generates from capital employed in its business. The formula for this calculation on TAKAYOSHI Holdings is:

Return on Capital Employed = Earnings Before Interest and Tax (EBIT) ÷ (Total Assets - Current Liabilities)

0.21 = JP¥912m ÷ (JP¥7.9b - JP¥3.6b) (Based on the trailing twelve months to June 2024).

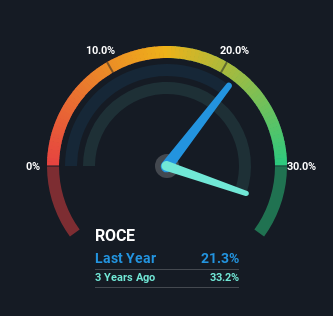

So, TAKAYOSHI Holdings has an ROCE of 21%. That's a fantastic return and not only that, it outpaces the average of 9.0% earned by companies in a similar industry.

See our latest analysis for TAKAYOSHI Holdings

Above you can see how the current ROCE for TAKAYOSHI Holdings compares to its prior returns on capital, but there's only so much you can tell from the past. If you'd like, you can check out the forecasts from the analysts covering TAKAYOSHI Holdings for free.

What Can We Tell From TAKAYOSHI Holdings' ROCE Trend?

It's hard not to be impressed by TAKAYOSHI Holdings' returns on capital. The company has consistently earned 21% for the last four years, and the capital employed within the business has risen 154% in that time. Returns like this are the envy of most businesses and given it has repeatedly reinvested at these rates, that's even better. You'll see this when looking at well operated businesses or favorable business models.

On a side note, TAKAYOSHI Holdings has done well to reduce current liabilities to 46% of total assets over the last four years. This can eliminate some of the risks inherent in the operations because the business has less outstanding obligations to their suppliers and or short-term creditors than they did previously. Although because current liabilities are still 46%, some of that risk is still prevalent.

What We Can Learn From TAKAYOSHI Holdings' ROCE

In summary, we're delighted to see that TAKAYOSHI Holdings has been compounding returns by reinvesting at consistently high rates of return, as these are common traits of a multi-bagger. However, despite the favorable fundamentals, the stock has fallen 33% over the last year, so there might be an opportunity here for astute investors. That's why we think it'd be worthwhile to look further into this stock given the fundamentals are appealing.

On a final note, we've found 2 warning signs for TAKAYOSHI Holdings that we think you should be aware of.

TAKAYOSHI Holdings is not the only stock earning high returns. If you'd like to see more, check out our free list of companies earning high returns on equity with solid fundamentals.

Valuation is complex, but we're here to simplify it.

Discover if TAKAYOSHI Holdings might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About TSE:9259

Excellent balance sheet and good value.

Market Insights

Advertisement

Community Narratives

BMW cruising ahead with new EVs and premium models to boost revenue 5%

Fair Value €135.07|44.5% undervalued

UN

Community Contributor

EU#2 - From Humble Beginnings to Global Powerhouse

Fair Value DKK 851.04|46.1% undervalued

TO

Community Contributor