Advertisement

The board of Okuwa Co., Ltd. (TSE:8217) has announced that it will pay a dividend on the 16th of May, with investors receiving ¥13.00 per share. The dividend yield will be 2.9% based on this payment which is still above the industry average.

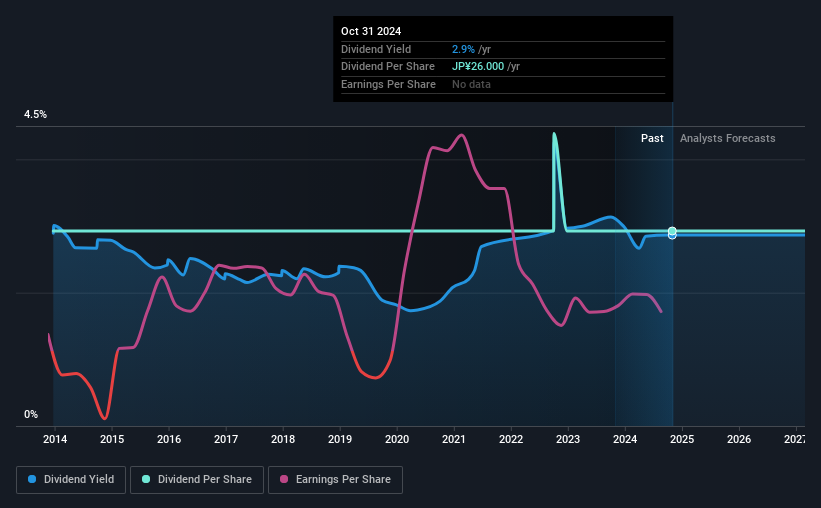

View our latest analysis for Okuwa

Estimates Indicate Okuwa's Could Struggle to Maintain Dividend Payments In The Future

A big dividend yield for a few years doesn't mean much if it can't be sustained. Based on the last payment, the company wasn't making enough to cover what it was paying to shareholders. Without profits and cash flows increasing, it would be difficult for the company to continue paying the dividend at this level.

Over the next year, EPS is forecast to expand by 24.3%. Assuming the dividend continues along recent trends, we think the payout ratio could reach 126%, which probably can't continue without putting some pressure on the balance sheet.

Dividend Volatility

The company has a long dividend track record, but it doesn't look great with cuts in the past. The last annual payment of ¥26.00 was flat on the annual payment from10 years ago. It's encouraging to see some dividend growth, but the dividend has been cut at least once, and the size of the cut would eliminate most of the growth anyway, which makes this less attractive as an income investment.

Dividend Growth Potential Is Shaky

With a relatively unstable dividend, it's even more important to evaluate if earnings per share is growing, which could point to a growing dividend in the future. Okuwa's earnings per share has shrunk at 16% a year over the past five years. A sharp decline in earnings per share is not great from from a dividend perspective. Even conservative payout ratios can come under pressure if earnings fall far enough. On the bright side, earnings are predicted to gain some ground over the next year, but until this turns into a pattern we wouldn't be feeling too comfortable.

We're Not Big Fans Of Okuwa's Dividend

In summary, while it is good to see that the dividend hasn't been cut, we think that at current levels the payment isn't particularly sustainable. The company's earnings aren't high enough to be making such big distributions, and it isn't backed up by strong growth or consistency either. Overall, the dividend is not reliable enough to make this a good income stock.

Investors generally tend to favour companies with a consistent, stable dividend policy as opposed to those operating an irregular one. However, there are other things to consider for investors when analysing stock performance. Case in point: We've spotted 2 warning signs for Okuwa (of which 1 makes us a bit uncomfortable!) you should know about. If you are a dividend investor, you might also want to look at our curated list of high yield dividend stocks.

New: AI Stock Screener & Alerts

Our new AI Stock Screener scans the market every day to uncover opportunities.

• Dividend Powerhouses (3%+ Yield)

• Undervalued Small Caps with Insider Buying

• High growth Tech and AI Companies

Or build your own from over 50 metrics.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About TSE:8217

Undervalued with excellent balance sheet.

Market Insights

Advertisement

Community Narratives

Alphabet: The Under-appreciated Compounder Hiding in Plain Sight

Fair Value US$268.43|27.9% undervalued

BL

Community Contributor

Planet Labs: At The Heart Of The Emerging New Space Boom

Fair Value US$11.31|43.8% undervalued

AN

Community Contributor

Exxon in Guyana 5 year forecast Low $135 to High $189

Fair Value US$189.00|41.0% undervalued

AG

Community Contributor