Advertisement

- Japan

- /

- Food and Staples Retail

- /

- TSE:2742

Unveiling Three Undiscovered Gems with Strong Financial Foundations

Simply Wall St

Reviewed by Simply Wall St

Amidst a backdrop of cautious sentiment driven by the Federal Reserve's rate cuts and looming political uncertainties, small-cap stocks have been particularly vulnerable, as evidenced by declines in key indices like the Russell 2000. Despite these challenges, the U.S. economy has shown resilience with stronger-than-expected growth and retail sales data, suggesting opportunities for discerning investors to identify stocks with robust financial foundations that can weather market volatility. In such an environment, identifying companies with strong balance sheets and consistent cash flows becomes crucial for those seeking stability and potential growth in their investment portfolios.

Top 10 Undiscovered Gems With Strong Fundamentals

| Name | Debt To Equity | Revenue Growth | Earnings Growth | Health Rating |

|---|---|---|---|---|

| Central Forest Group | NA | 6.85% | 15.11% | ★★★★★★ |

| Ovostar Union | 0.01% | 10.19% | 49.85% | ★★★★★★ |

| Standard Bank | 0.13% | 27.78% | 30.36% | ★★★★★★ |

| Tianyun International Holdings | 10.09% | -5.59% | -9.92% | ★★★★★★ |

| PBA Holdings Bhd | 1.86% | 7.41% | 40.17% | ★★★★★☆ |

| First National Bank of Botswana | 24.77% | 10.64% | 15.30% | ★★★★★☆ |

| Pure Cycle | 5.31% | -4.44% | -5.74% | ★★★★★☆ |

| A2B Australia | 15.83% | -7.78% | 25.44% | ★★★★☆☆ |

| DIRTT Environmental Solutions | 58.73% | -5.34% | -5.43% | ★★★★☆☆ |

| Krom Bank Indonesia | NA | 40.04% | 35.44% | ★★★★☆☆ |

Here we highlight a subset of our preferred stocks from the screener.

ABG Sundal Collier Holding (OB:ABG)

Simply Wall St Value Rating: ★★★★★☆

Overview: ABG Sundal Collier Holding ASA is a company that offers investment banking, stock broking, and corporate advisory services across Norway, Sweden, Denmark, and internationally with a market capitalization of NOK3.69 billion.

Operations: ABG Sundal Collier generates revenue primarily from three segments: M&A and Advisory (NOK 621.77 million), Corporate Financing (NOK 673.99 million), and Brokerage and Research (NOK 553.98 million). The company focuses on these key areas to drive its financial performance across various markets.

ABG Sundal Collier Holding, a nimble player in the financial sector, shows promise with its robust financial health. The company boasts more cash than total debt and has seen a reduction in its debt-to-equity ratio from 35% to 18.1% over five years. Recent earnings growth of 24.7% outpaces the industry average of 23.6%, indicating strong performance, although earnings have declined by an average of 4.8% annually over five years. Trading at about 39% below estimated fair value suggests potential upside for investors seeking undervalued opportunities in this space, despite recent shareholder dilution concerns.

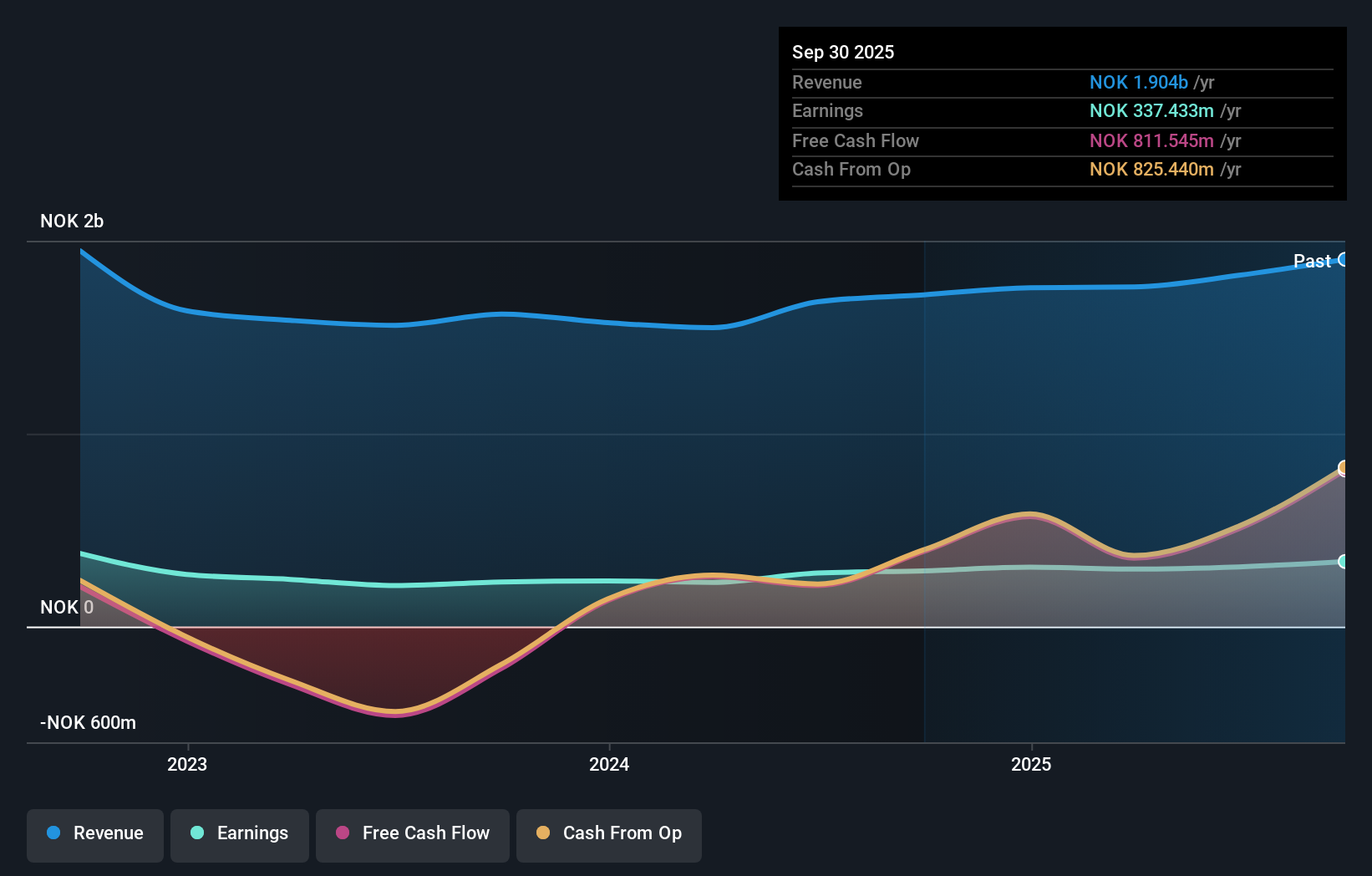

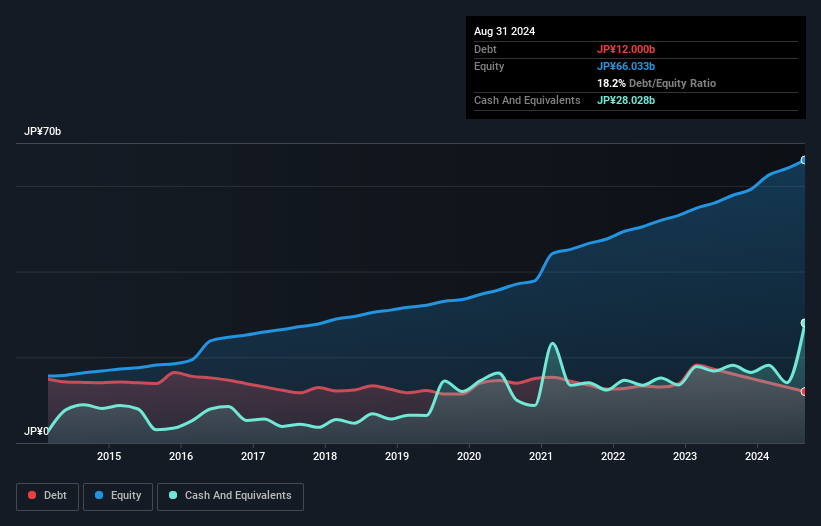

HalowsLtd (TSE:2742)

Simply Wall St Value Rating: ★★★★★☆

Overview: Halows Co., Ltd. operates a network of supermarket stores across several regions in Japan, including Hiroshima and Okayama, with a market capitalization of ¥85.95 billion.

Operations: HalowsLtd generates revenue primarily through its network of supermarket stores across several regions in Japan. The company's financial performance is highlighted by a focus on managing costs effectively to support its operations.

Halows Ltd. demonstrates notable financial health, with its debt to equity ratio decreasing from 34.5% to 18.2% over five years, indicating improved leverage management. The company is trading at a significant discount of 96.9% below its estimated fair value, suggesting potential undervaluation in the market. Recent earnings growth of 36.9% outpaces the Consumer Retailing industry average of 10.5%, highlighting robust performance relative to peers. Additionally, Halows has increased its dividend from JPY 20 to JPY 26 per share and forecasts a profit of JPY 7,420 million for the fiscal year ending February 2025, reflecting positive forward momentum in earnings and shareholder returns.

- Click here to discover the nuances of HalowsLtd with our detailed analytical health report.

Understand HalowsLtd's track record by examining our Past report.

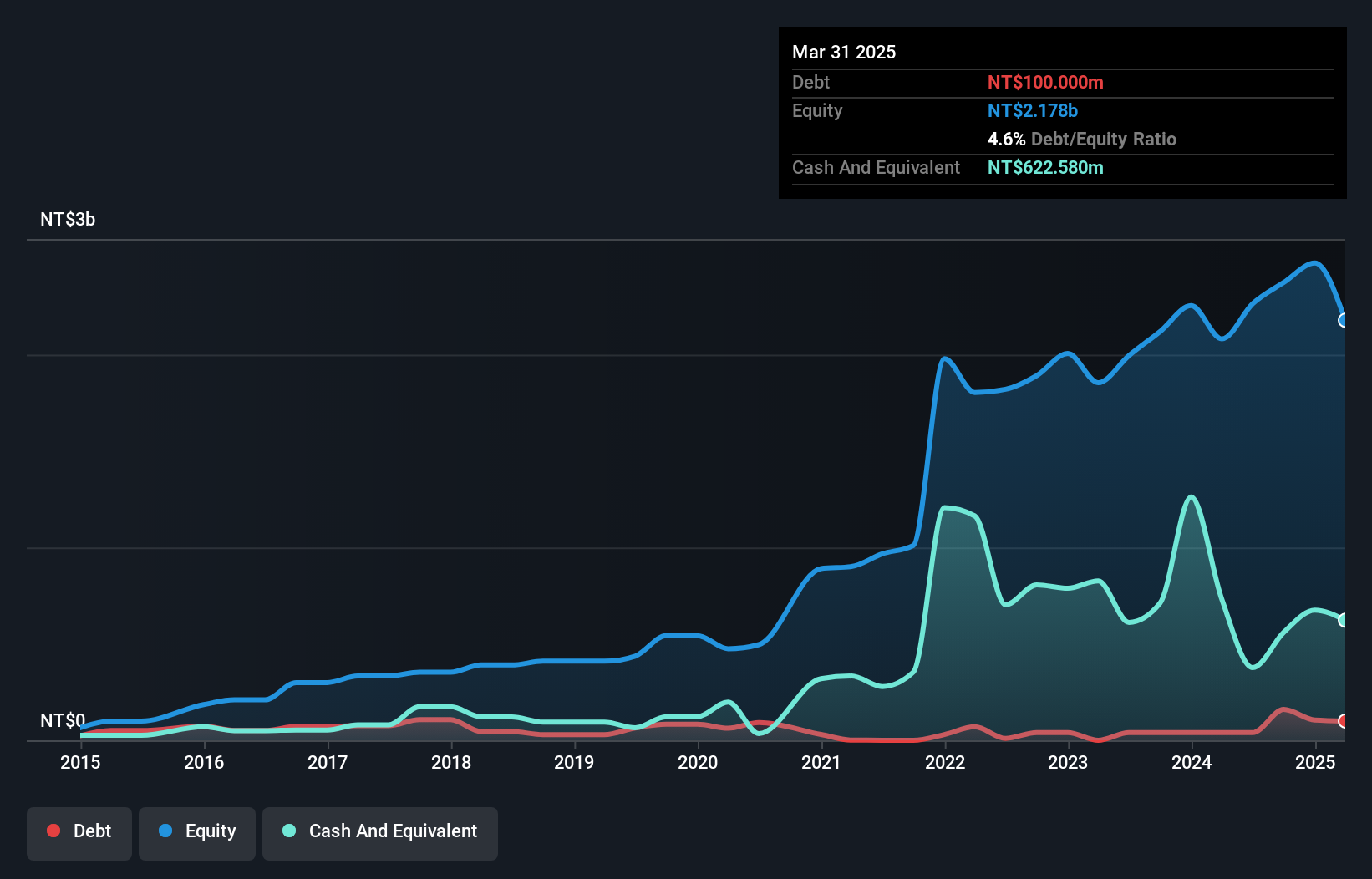

Transcom (TWSE:5222)

Simply Wall St Value Rating: ★★★★★★

Overview: Transcom, Inc. is a company specializing in microwave devices and subsystems with operations spanning Taiwan, Asia, Europe, North America, and other international markets, and it has a market cap of NT$10.17 billion.

Operations: Transcom derives its revenue primarily from the wireless communications equipment segment, generating NT$1.35 billion.

Transcom's recent financial performance shows promising signs for this small cap company. Over the past five years, its debt-to-equity ratio improved from 15.3% to 6.7%, indicating a more robust balance sheet. The company reported TWD 330.67 million in sales for Q3 2024, up from TWD 309.6 million the previous year, although net income slightly dipped to TWD 120.58 million from TWD 122.72 million last year. A share repurchase program worth TWD 1,461.33 million is underway, aiming to enhance shareholder value by buying back up to 1,500,000 shares within a price range of TWD 105-140 each.

- Get an in-depth perspective on Transcom's performance by reading our health report here.

Evaluate Transcom's historical performance by accessing our past performance report.

Turning Ideas Into Actions

- Investigate our full lineup of 4633 Undiscovered Gems With Strong Fundamentals right here.

- Already own these companies? Bring clarity to your investment decisions by linking up your portfolio with Simply Wall St, where you can monitor all the vital signs of your stocks effortlessly.

- Unlock the power of informed investing with Simply Wall St, your free guide to navigating stock markets worldwide.

Searching for a Fresh Perspective?

- Explore high-performing small cap companies that haven't yet garnered significant analyst attention.

- Fuel your portfolio with companies showing strong growth potential, backed by optimistic outlooks both from analysts and management.

- Find companies with promising cash flow potential yet trading below their fair value.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Valuation is complex, but we're here to simplify it.

Discover if HalowsLtd might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About TSE:2742

HalowsLtd

Operates a network of supermarket stores in Hiroshima, Okayama, Kagawa, Ehime, Tokushima, and Hyogo of Japan.

Excellent balance sheet and good value.

Market Insights

Advertisement

Community Narratives

Groundbreaking therapies that could change the treatment landscape for PTSD, fibromyalgia, MS & Alzheimer’s

Fair Value US$6.20|86.9% undervalued

CM

Community Contributor

DigitalOcean Will Grow 14% by Embracing AI with Paperspace Acquisition

Fair Value US$50.00|42.8% undervalued

NE

Community Contributor

Viant Technology: A Rising AdTech Challenger in the AI-Powered CTV Market

Fair Value US$38.61|66.0% undervalued

BL

Community Contributor

Volvo will Accelerate Forward into Electric and Autonomous Leadership in Five Years

Fair Value SEK 438.80|40.8% undervalued

UN

Community Contributor