Advertisement

- Japan

- /

- Consumer Durables

- /

- TSE:7740

Tamron (TSE:7740): Revisiting Valuation After Updated Earnings Guidance and Announced 4-for-1 Stock Split

Simply Wall St

Reviewed by Simply Wall St

Tamron (TSE:7740) just updated its earnings guidance for the fiscal year ending December 2025, sharing new projections for sales, profit, and net income. The company also announced a 4-for-1 stock split that will take effect in July.

See our latest analysis for TamronLtd.

TamronLtd’s latest guidance and the upcoming stock split have arrived at a time when the company’s momentum has cooled somewhat. While the 90-day share price return is up 3%, the year-to-date move is -6.2%. For long-term holders, a 3-year total shareholder return of 185% and a remarkable 5-year return of 488% show just how strong the company’s performance has been versus where it started.

If TamronLtd’s evolving story makes you curious about what else investors are finding, it could be the perfect moment to broaden your search and discover fast growing stocks with high insider ownership

The question now is whether TamronLtd’s current valuation still offers room for upside or if recent guidance and the stock split have already set expectations for future growth, leaving little opportunity for outperformance.

Price-to-Earnings of 13.4x: Is it justified?

TamronLtd currently trades at a price-to-earnings ratio of 13.4x, which offers a compelling comparison point to both peers and its historical norms.

The price-to-earnings ratio (P/E) reflects how much investors are willing to pay for each unit of earnings and is a key benchmark for consumer durables companies, given their profit cycles and capital requirements. TamronLtd's P/E is significantly below the peer average and below its fair value ratio. This indicates the market may not be pricing in the company's earnings power as highly as its competitors.

However, when compared to the wider Japanese Consumer Durables industry, TamronLtd's multiple is actually higher than the sector average of 11.5x. This suggests a modest premium. Relative to a fair price-to-earnings ratio of 14.7x for the company, there is still some room for upward re-rating if the company can deliver on growth expectations and profitability.

Explore the SWS fair ratio for TamronLtd

Result: Price-to-Earnings of 13.4x (UNDERVALUED)

However, risks such as slowing revenue growth and recent underperformance compared to the sector could challenge the bullish outlook if not addressed in coming quarters.

Find out about the key risks to this TamronLtd narrative.

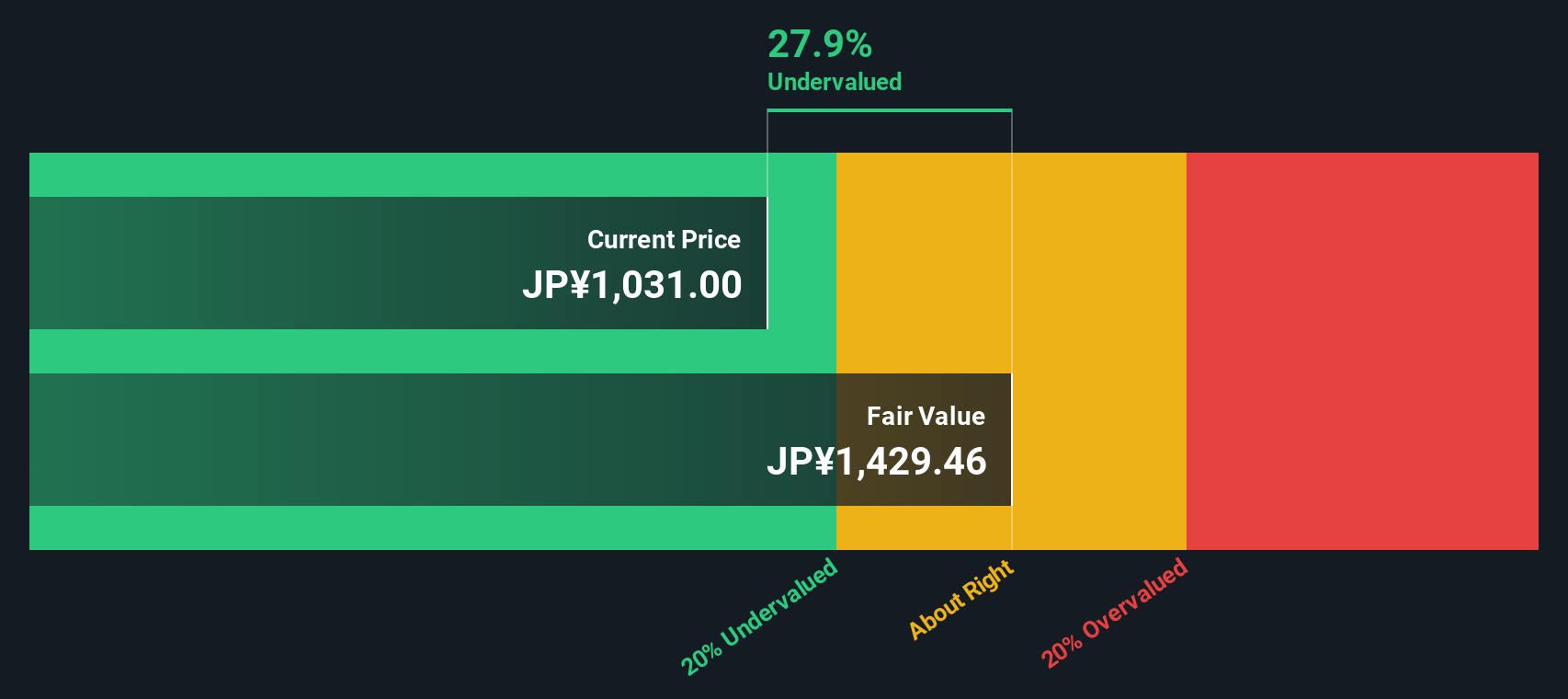

Another View: Discounted Cash Flow Analysis

While ratios tell one story, our DCF model gives a different perspective. According to this approach, TamronLtd is trading 28% below its estimated fair value of ¥1,428.5. This suggests the shares may be materially undervalued even after recent guidance and the stock split announcement. Which view will the market trust?

Look into how the SWS DCF model arrives at its fair value.

Simply Wall St performs a discounted cash flow (DCF) on every stock in the world every day (check out TamronLtd for example). We show the entire calculation in full. You can track the result in your watchlist or portfolio and be alerted when this changes, or use our stock screener to discover 896 undervalued stocks based on their cash flows. If you save a screener we even alert you when new companies match - so you never miss a potential opportunity.

Build Your Own TamronLtd Narrative

If you prefer hands-on analysis or want to draw your own conclusions from TamronLtd’s numbers, you can build your story in just a few minutes with Do it your way.

A great starting point for your TamronLtd research is our analysis highlighting 2 key rewards and 1 important warning sign that could impact your investment decision.

Looking for more investment ideas?

There is so much more opportunity beyond a single stock, and a focused search can reveal hidden gems. The right screener lets you spot tomorrow’s standouts before most investors even notice.

- Unlock consistent income streams by checking out these 15 dividend stocks with yields > 3% offering attractive yields above 3% and stable financials.

- Fuel your portfolio’s growth with these 26 quantum computing stocks featuring innovators at the forefront of quantum breakthroughs and next-generation technology.

- Capitalize on breakthrough medical trends by exploring these 30 healthcare AI stocks and find healthcare pioneers pushing boundaries with advanced AI solutions.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Valuation is complex, but we're here to simplify it.

Discover if TamronLtd might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About TSE:7740

TamronLtd

Manufactures and sells optical equipment in Japan, North America, Europe, and Asia.

Flawless balance sheet, good value and pays a dividend.

Similar Companies

Market Insights

Advertisement

Community Narratives

MicroVision will explode future revenue by 380.37% with a vision towards success

Fair Value US$60.00|98.5% undervalued

TH

Community Contributor

The Indispensable Artery for a New North American Economy

Fair Value CA$132.87|2.3% undervalued

TI

Community Contributor