Advertisement

Why It Might Not Make Sense To Buy Shikibo Ltd. (TSE:3109) For Its Upcoming Dividend

Regular readers will know that we love our dividends at Simply Wall St, which is why it's exciting to see Shikibo Ltd. (TSE:3109) is about to trade ex-dividend in the next 3 days. The ex-dividend date is commonly two business days before the record date, which is the cut-off date for shareholders to be present on the company's books to be eligible for a dividend payment. The ex-dividend date is of consequence because whenever a stock is bought or sold, the trade can take two business days or more to settle. Thus, you can purchase Shikibo's shares before the 28th of March in order to receive the dividend, which the company will pay on the 30th of June.

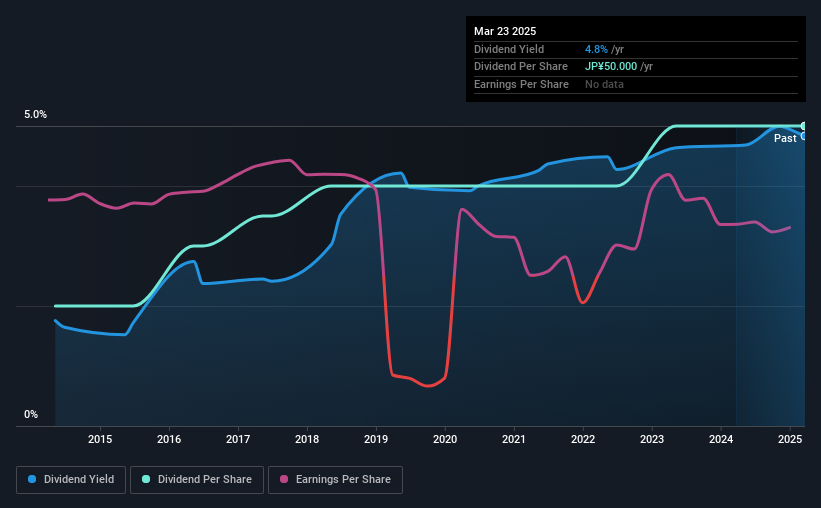

The company's next dividend payment will be JP¥25.00 per share. Last year, in total, the company distributed JP¥50.00 to shareholders. Calculating the last year's worth of payments shows that Shikibo has a trailing yield of 4.8% on the current share price of JP¥1034.00. Dividends are an important source of income to many shareholders, but the health of the business is crucial to maintaining those dividends. We need to see whether the dividend is covered by earnings and if it's growing.

Dividends are typically paid out of company income, so if a company pays out more than it earned, its dividend is usually at a higher risk of being cut. Shikibo distributed an unsustainably high 116% of its profit as dividends to shareholders last year. Without more sustainable payment behaviour, the dividend looks precarious. A useful secondary check can be to evaluate whether Shikibo generated enough free cash flow to afford its dividend. Over the past year it paid out 121% of its free cash flow as dividends, which is uncomfortably high. It's hard to consistently pay out more cash than you generate without either borrowing or using company cash, so we'd wonder how the company justifies this payout level.

Cash is slightly more important than profit from a dividend perspective, but given Shikibo's payments were not well covered by either earnings or cash flow, we are concerned about the sustainability of this dividend.

Check out our latest analysis for Shikibo

Click here to see how much of its profit Shikibo paid out over the last 12 months.

Have Earnings And Dividends Been Growing?

Stocks in companies that generate sustainable earnings growth often make the best dividend prospects, as it is easier to lift the dividend when earnings are rising. Investors love dividends, so if earnings fall and the dividend is reduced, expect a stock to be sold off heavily at the same time. It's encouraging to see Shikibo has grown its earnings rapidly, up 29% a year for the past five years. Shikibo's dividend was not well covered by earnings, although at least its earnings per share are growing quickly. Fast-growing businesses normally need to reinvest most of their earnings in order to maintain growth, so we'd suspect that either earnings growth will slow or the dividend may not be increased for a while.

We'd also point out that Shikibo issued a meaningful number of new shares in the past year. Trying to grow the dividend while issuing large amounts of new shares reminds us of the ancient Greek tale of Sisyphus - perpetually pushing a boulder uphill.

The main way most investors will assess a company's dividend prospects is by checking the historical rate of dividend growth. Since the start of our data, 10 years ago, Shikibo has lifted its dividend by approximately 9.6% a year on average. It's encouraging to see the company lifting dividends while earnings are growing, suggesting at least some corporate interest in rewarding shareholders.

The Bottom Line

Is Shikibo worth buying for its dividend? While it's nice to see earnings per share growing, we're curious about how Shikibo intends to continue growing, or maintain the dividend in a downturn given that it's paying out such a high percentage of its earnings and cashflow. With the way things are shaping up from a dividend perspective, we'd be inclined to steer clear of Shikibo.

Having said that, if you're looking at this stock without much concern for the dividend, you should still be familiar of the risks involved with Shikibo. Be aware that Shikibo is showing 3 warning signs in our investment analysis, and 2 of those are potentially serious...

Generally, we wouldn't recommend just buying the first dividend stock you see. Here's a curated list of interesting stocks that are strong dividend payers.

New: Manage All Your Stock Portfolios in One Place

We've created the ultimate portfolio companion for stock investors, and it's free.

• Connect an unlimited number of Portfolios and see your total in one currency

• Be alerted to new Warning Signs or Risks via email or mobile

• Track the Fair Value of your stocks

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About TSE:3109

Shikibo

Manufactures, processes, and markets various textile products in Japan and internationally.

Proven track record average dividend payer.

Market Insights

Advertisement

Community Narratives

The Future of Drug Testing? Fingerprint Tech Shows Serious Promise

Fair Value US$2.98|40.3% undervalued

JO

Community Contributor

Suncorp’s Next Chapter: Insurance-Only and Ready to Grow

Fair Value AU$22.83|7.9% undervalued

RO

Community Contributor

Thyssenkrupp Nucera Will Achieve Double-Digit Profits by 2030 Boosted by Hydrogen Growth

Fair Value €14.40|31.6% undervalued

CH

Community Contributor

Tesla’s Nvidia Moment – The AI & Robotics Inflection Point

Fair Value US$359.72|12.3% undervalued

BL

Community Contributor