Advertisement

- Japan

- /

- Commercial Services

- /

- TSE:7846

We Wouldn't Be Too Quick To Buy Pilot Corporation (TSE:7846) Before It Goes Ex-Dividend

Some investors rely on dividends for growing their wealth, and if you're one of those dividend sleuths, you might be intrigued to know that Pilot Corporation (TSE:7846) is about to go ex-dividend in just three days. The ex-dividend date occurs one day before the record date which is the day on which shareholders need to be on the company's books in order to receive a dividend. The ex-dividend date is important as the process of settlement involves two full business days. So if you miss that date, you would not show up on the company's books on the record date. Thus, you can purchase Pilot's shares before the 27th of December in order to receive the dividend, which the company will pay on the 31st of March.

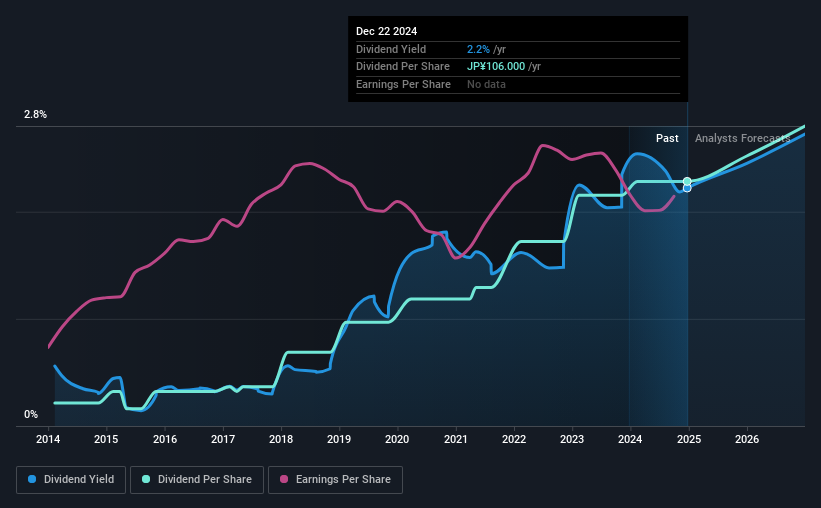

The company's next dividend payment will be JP¥53.00 per share, and in the last 12 months, the company paid a total of JP¥106 per share. Based on the last year's worth of payments, Pilot has a trailing yield of 2.2% on the current stock price of JP¥4772.00. We love seeing companies pay a dividend, but it's also important to be sure that laying the golden eggs isn't going to kill our golden goose! So we need to investigate whether Pilot can afford its dividend, and if the dividend could grow.

See our latest analysis for Pilot

Dividends are typically paid from company earnings. If a company pays more in dividends than it earned in profit, then the dividend could be unsustainable. That's why it's good to see Pilot paying out a modest 30% of its earnings. Yet cash flow is typically more important than profit for assessing dividend sustainability, so we should always check if the company generated enough cash to afford its dividend. It paid out an unsustainably high 286% of its free cash flow as dividends over the past 12 months, which is worrying. Our definition of free cash flow excludes cash generated from asset sales, so since Pilot is paying out such a high percentage of its cash flow, it might be worth seeing if it sold assets or had similar events that might have led to such a high dividend payment.

Pilot does have a large net cash position on the balance sheet, which could fund large dividends for a time, if the company so chose. Still, smart investors know that it is better to assess dividends relative to the cash and profit generated by the business. Paying dividends out of cash on the balance sheet is not long-term sustainable.

While Pilot's dividends were covered by the company's reported profits, cash is somewhat more important, so it's not great to see that the company didn't generate enough cash to pay its dividend. Were this to happen repeatedly, this would be a risk to Pilot's ability to maintain its dividend.

Click here to see how much of its profit Pilot paid out over the last 12 months.

Have Earnings And Dividends Been Growing?

Stocks with flat earnings can still be attractive dividend payers, but it is important to be more conservative with your approach and demand a greater margin for safety when it comes to dividend sustainability. If business enters a downturn and the dividend is cut, the company could see its value fall precipitously. It's not encouraging to see that Pilot's earnings are effectively flat over the past five years. We'd take that over an earnings decline any day, but in the long run, the best dividend stocks all grow their earnings per share.

Many investors will assess a company's dividend performance by evaluating how much the dividend payments have changed over time. Pilot has delivered an average of 27% per year annual increase in its dividend, based on the past 10 years of dividend payments.

The Bottom Line

Should investors buy Pilot for the upcoming dividend? It's disappointing to see earnings per share have fallen slightly, even though Pilot is paying out less than half its income as dividends. It's also paying out an uncomfortably high percentage of its cash flow, which makes us wonder just how sustainable the dividend really is. With the way things are shaping up from a dividend perspective, we'd be inclined to steer clear of Pilot.

With that in mind though, if the poor dividend characteristics of Pilot don't faze you, it's worth being mindful of the risks involved with this business. Every company has risks, and we've spotted 1 warning sign for Pilot you should know about.

A common investing mistake is buying the first interesting stock you see. Here you can find a full list of high-yield dividend stocks.

New: Manage All Your Stock Portfolios in One Place

We've created the ultimate portfolio companion for stock investors, and it's free.

• Connect an unlimited number of Portfolios and see your total in one currency

• Be alerted to new Warning Signs or Risks via email or mobile

• Track the Fair Value of your stocks

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About TSE:7846

Pilot

Manufactures, purchases, and sells writing instruments, and other stationery products and toys in Japan, the United States, Europe, and Asia.

Flawless balance sheet with solid track record and pays a dividend.

Similar Companies

Market Insights

Advertisement

Community Narratives

BMW cruising ahead with new EVs and premium models to boost revenue 5%

Fair Value €135.07|45.0% undervalued

UN

Community Contributor

EU#2 - From Humble Beginnings to Global Powerhouse

Fair Value DKK 851.04|48.9% undervalued

TO

Community Contributor