Advertisement

- Japan

- /

- Professional Services

- /

- TSE:7352

3 Stocks That May Be Priced Below Their Estimated Value In January 2025

Simply Wall St

Reviewed by Simply Wall St

As global markets navigate a mixed economic landscape marked by resilient labor markets and inflationary pressures, investors are closely monitoring the impact of these factors on stock valuations. With U.S. equities experiencing volatility and small-cap stocks underperforming, there is growing interest in identifying stocks that may currently be priced below their estimated value. In such an environment, a good stock often exhibits strong fundamentals, resilience to market fluctuations, and potential for long-term growth despite short-term challenges.

Top 10 Undervalued Stocks Based On Cash Flows

| Name | Current Price | Fair Value (Est) | Discount (Est) |

| Hunan Jiudian Pharmaceutical (SZSE:300705) | CN¥17.19 | CN¥34.17 | 49.7% |

| Clear Secure (NYSE:YOU) | US$26.72 | US$53.44 | 50% |

| Sichuan Injet Electric (SZSE:300820) | CN¥50.39 | CN¥100.73 | 50% |

| NBTM New Materials Group (SHSE:600114) | CN¥15.60 | CN¥31.06 | 49.8% |

| Ningbo Haitian Precision MachineryLtd (SHSE:601882) | CN¥20.26 | CN¥40.47 | 49.9% |

| Aguas Andinas (SNSE:AGUAS-A) | CLP290.99 | CLP580.39 | 49.9% |

| Constellium (NYSE:CSTM) | US$10.35 | US$20.64 | 49.8% |

| Andrada Mining (AIM:ATM) | £0.0235 | £0.047 | 49.9% |

| Vogo (ENXTPA:ALVGO) | €2.95 | €5.88 | 49.8% |

| Shinko Electric Industries (TSE:6967) | ¥5874.00 | ¥11677.29 | 49.7% |

Let's uncover some gems from our specialized screener.

Laboratorios Farmaceuticos Rovi (BME:ROVI)

Overview: Laboratorios Farmaceuticos Rovi, S.A. is involved in the research, development, manufacture, and marketing of pharmaceutical products both in Spain and internationally, with a market cap of €3.25 billion.

Operations: Revenue Segments (in millions of €):

Estimated Discount To Fair Value: 29.9%

Laboratorios Farmaceuticos Rovi is trading 29.9% below its estimated fair value of €90.64, presenting potential undervaluation based on cash flows. Despite recent earnings showing a slight decline in sales and net income, the company's earnings are forecast to grow at 15.93% annually, outpacing the Spanish market's growth rate of 8.2%. Analysts agree on a potential stock price increase of 40.5%, although share price volatility remains high over the past three months.

- Our growth report here indicates Laboratorios Farmaceuticos Rovi may be poised for an improving outlook.

- Get an in-depth perspective on Laboratorios Farmaceuticos Rovi's balance sheet by reading our health report here.

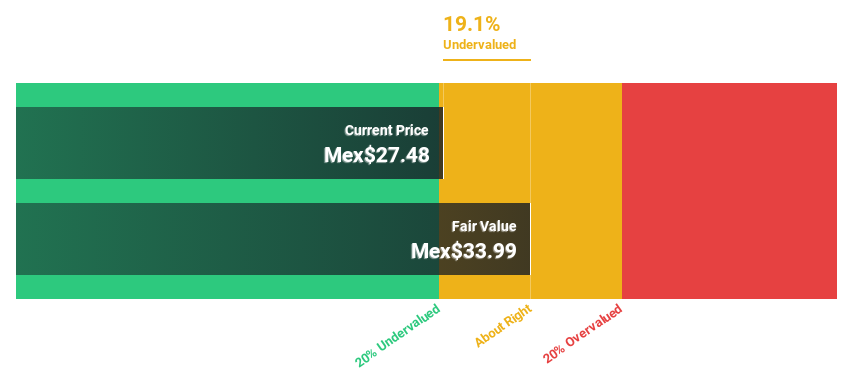

Genomma Lab Internacional. de (BMV:LAB B)

Overview: Genomma Lab Internacional, S.A.B. de C.V. operates in the pharmaceutical and personal care sectors across Latin America, with a market capitalization of MX$24.42 billion.

Operations: The company generates revenue of MX$17.47 billion from its operations in the pharmaceutical and personal care products industry across Latin America.

Estimated Discount To Fair Value: 13.7%

Genomma Lab Internacional is trading at MX$26.4, approximately 13.7% below its estimated fair value of MX$30.58, suggesting potential undervaluation based on cash flows. The company reported a strong increase in third-quarter earnings, with net income rising to MX$660.06 million from MX$370.67 million year-on-year. Despite high debt levels, earnings are projected to grow at 19.52% annually, outpacing the Mexican market's average growth rate of 12.3%.

- Upon reviewing our latest growth report, Genomma Lab Internacional. de's projected financial performance appears quite optimistic.

- Click here to discover the nuances of Genomma Lab Internacional. de with our detailed financial health report.

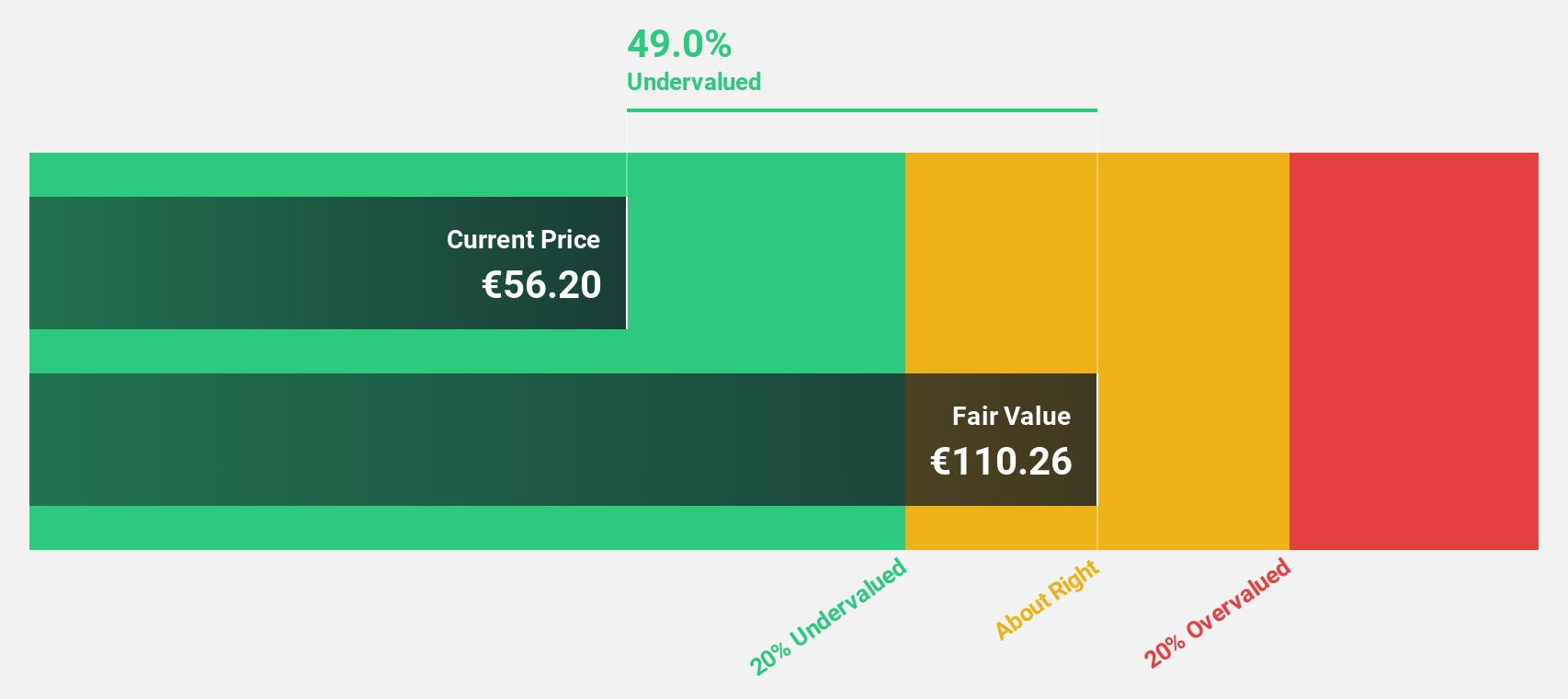

TWOSTONE&Sons (TSE:7352)

Overview: TWOSTONE&Sons Inc. operates in the IT service sector in Japan with a market capitalization of ¥42.26 billion.

Operations: The company's revenue is derived from three main segments: Engineer Platform Service at ¥12.77 billion, Marketing Platform Service at ¥509.57 million, and Consulting and Advisory Services at ¥1.05 billion.

Estimated Discount To Fair Value: 20%

TWOSTONE&Sons, trading at ¥976, is approximately 20% below its estimated fair value of ¥1219.32, indicating potential undervaluation based on cash flows. Earnings grew by 10.6% last year and are forecast to grow significantly at 31.47% annually, surpassing the JP market's average growth rate of 8%. Despite recent shareholder dilution and high share price volatility, the company's revenue growth is expected to outpace the market at 16.9% per year.

- Our earnings growth report unveils the potential for significant increases in TWOSTONE&Sons' future results.

- Navigate through the intricacies of TWOSTONE&Sons with our comprehensive financial health report here.

Summing It All Up

- Delve into our full catalog of 875 Undervalued Stocks Based On Cash Flows here.

- Hold shares in these firms? Setup your portfolio in Simply Wall St to seamlessly track your investments and receive personalized updates on your portfolio's performance.

- Elevate your portfolio with Simply Wall St, the ultimate app for investors seeking global market coverage.

Contemplating Other Strategies?

- Explore high-performing small cap companies that haven't yet garnered significant analyst attention.

- Diversify your portfolio with solid dividend payers offering reliable income streams to weather potential market turbulence.

- Fuel your portfolio with companies showing strong growth potential, backed by optimistic outlooks both from analysts and management.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Valuation is complex, but we're here to simplify it.

Discover if TWOSTONE&Sons might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About TSE:7352

Exceptional growth potential with outstanding track record.

Market Insights

Advertisement

Community Narratives

Alphabet: The Under-appreciated Compounder Hiding in Plain Sight

Fair Value US$282.83|30.2% undervalued

BL

Community Contributor

Planet Labs: At The Heart Of The Emerging New Space Boom

Fair Value US$11.31|44.5% undervalued

AN

Community Contributor

Exxon in Guyana 5 year forecast Low $135 to High $189

Fair Value US$189.00|40.8% undervalued

AG

Community Contributor