- Japan

- /

- Professional Services

- /

- TSE:6532

High Insider Ownership Growth Companies On The Japanese Exchange In July 2024

Reviewed by Simply Wall St

Japan's stock markets have recently demonstrated robust performance, with the Nikkei 225 and TOPIX indexes reaching all-time highs, reflecting a positive sentiment despite global economic uncertainties. In this context, exploring growth companies with high insider ownership on the Japanese Exchange can offer insights into firms that potentially have aligned interests between shareholders and management, which is crucial in navigating current market conditions.

Top 10 Growth Companies With High Insider Ownership In Japan

| Name | Insider Ownership | Earnings Growth |

| SHIFT (TSE:3697) | 35.4% | 26.9% |

| Hottolink (TSE:3680) | 27% | 57.4% |

| Kasumigaseki CapitalLtd (TSE:3498) | 34.8% | 42.1% |

| Medley (TSE:4480) | 34% | 28.7% |

| Micronics Japan (TSE:6871) | 15.3% | 39.8% |

| Kanamic NetworkLTD (TSE:3939) | 25% | 28.9% |

| ExaWizards (TSE:4259) | 21.9% | 91.1% |

| AeroEdge (TSE:7409) | 10.7% | 28.5% |

| Soiken Holdings (TSE:2385) | 19.8% | 118.4% |

| freee K.K (TSE:4478) | 23.9% | 72.9% |

We're going to check out a few of the best picks from our screener tool.

Mercari (TSE:4385)

Simply Wall St Growth Rating: ★★★★☆☆

Overview: Mercari, Inc. is a company that designs, develops, and operates the Mercari marketplace applications in Japan and the United States, with a market capitalization of approximately ¥401.96 billion.

Operations: The primary revenue for this entity is generated through its marketplace applications active in Japan and the United States.

Insider Ownership: 36%

Mercari, a growth-oriented company in Japan with high insider ownership, shows promising financial trends despite some volatility. Its revenue is expected to grow at 9.7% annually, outpacing the Japanese market average of 4.3%. Earnings have surged by a very large 222.8% over the past year and are projected to increase by 18.82% annually. However, its share price has been highly volatile recently. The firm anticipates JPY 190 billion in revenue and JPY 12 billion profit for FY2024.

- Click to explore a detailed breakdown of our findings in Mercari's earnings growth report.

- Our valuation report unveils the possibility Mercari's shares may be trading at a premium.

Rakuten Group (TSE:4755)

Simply Wall St Growth Rating: ★★★★☆☆

Overview: Rakuten Group, Inc. operates globally, offering a diverse range of services including e-commerce, fintech, digital content, and communications with a market capitalization of approximately ¥1.91 trillion.

Operations: The company generates revenue through diverse sectors such as e-commerce, fintech, digital content, and communications.

Insider Ownership: 17.3%

Rakuten Group, poised for growth with high insider ownership, is expected to see revenue increase at 7.8% annually, surpassing Japan's average of 4.3%. While its Return on Equity might remain low at 8.9%, earnings are projected to grow significantly by 83.11% annually and reach profitability within three years. Recent guidance suggests a robust double-digit growth in operating results for FY2024, excluding the volatile securities sector, underscoring its potential despite some financial soft spots.

- Get an in-depth perspective on Rakuten Group's performance by reading our analyst estimates report here.

- According our valuation report, there's an indication that Rakuten Group's share price might be on the cheaper side.

BayCurrent Consulting (TSE:6532)

Simply Wall St Growth Rating: ★★★★☆☆

Overview: BayCurrent Consulting, Inc., based in Japan, offers consulting services and has a market capitalization of approximately ¥556.97 billion.

Operations: BayCurrent Consulting operates primarily in the consulting services sector in Japan.

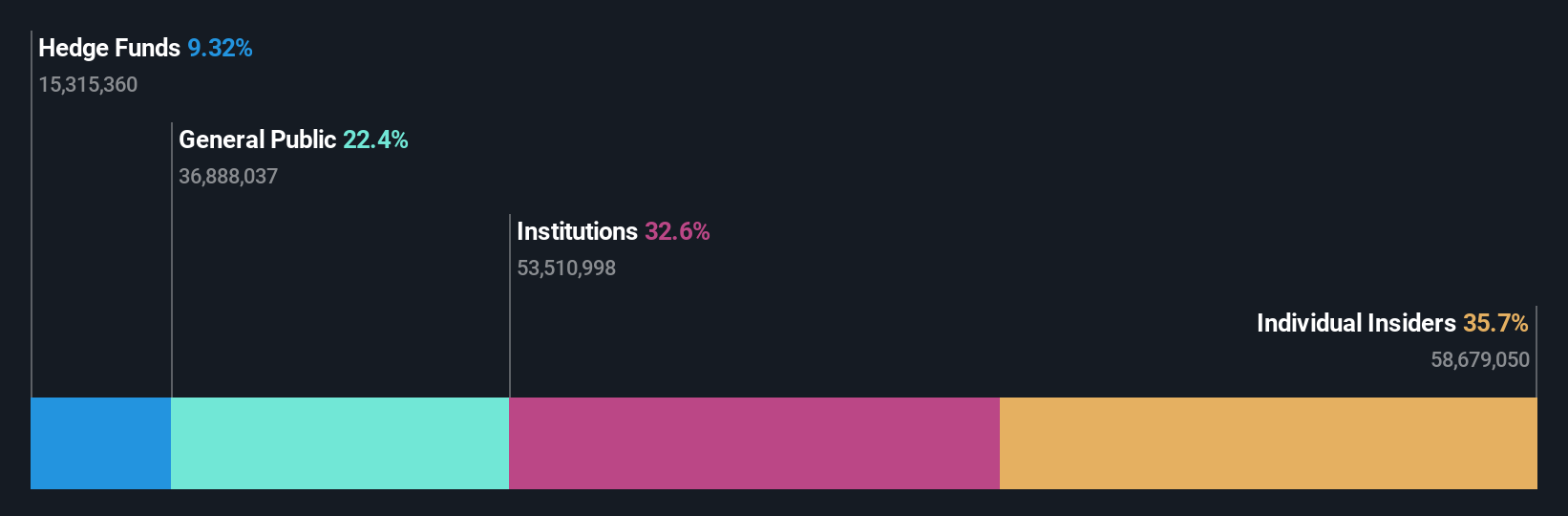

Insider Ownership: 13.9%

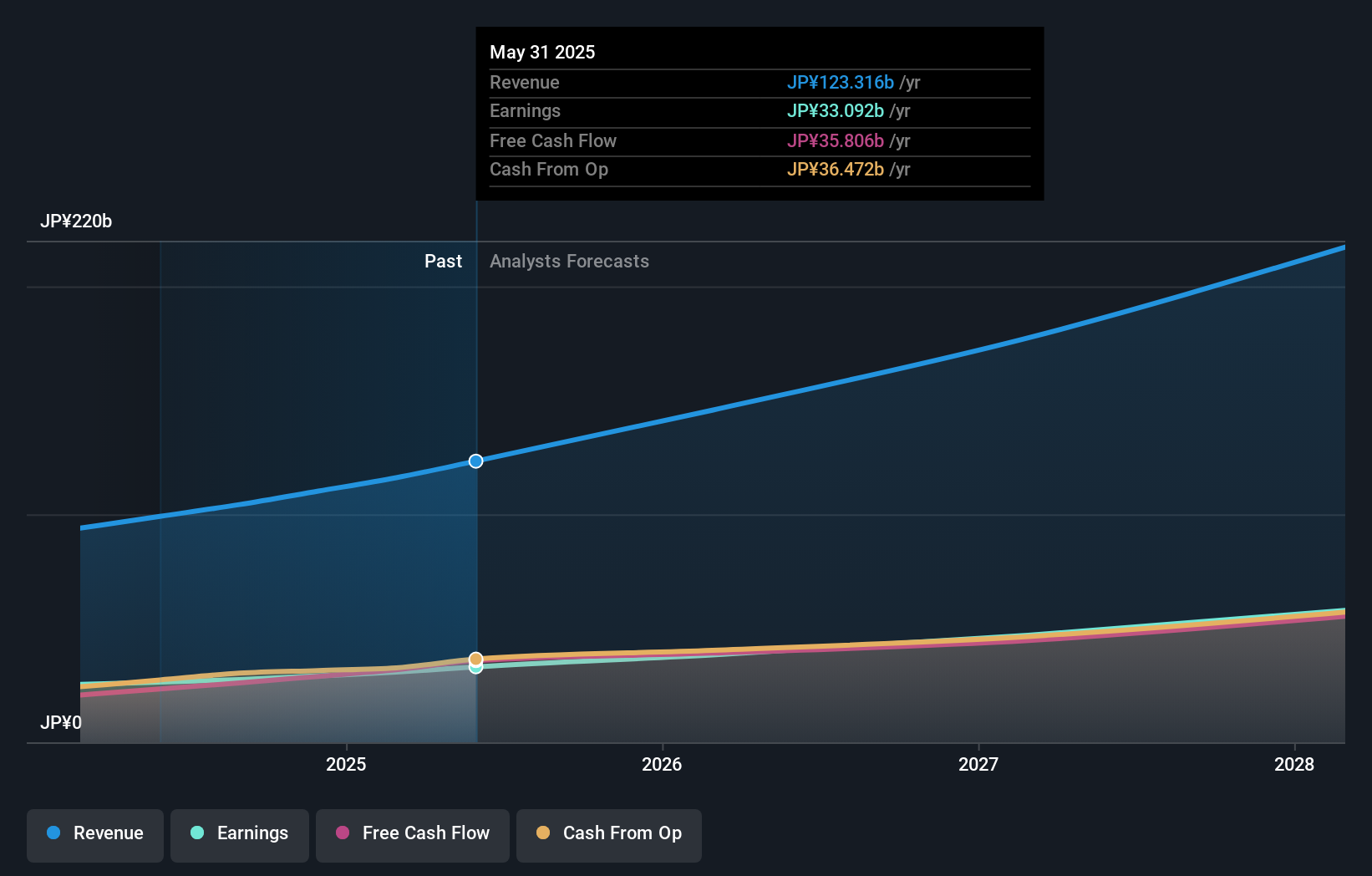

BayCurrent Consulting, with high insider ownership, shows promising growth prospects in Japan. The company's earnings are expected to grow by 18.4% annually, outpacing the Japanese market average of 8.9%. Additionally, its revenue growth forecast at 18.3% annually also exceeds the market's 4.3%. Recently, BayCurrent completed a share buyback for ¥3.60 billion enhancing shareholder value and capital efficiency despite a highly volatile share price in recent months and trading at significant undervaluation compared to its estimated fair value.

- Unlock comprehensive insights into our analysis of BayCurrent Consulting stock in this growth report.

- Our expertly prepared valuation report BayCurrent Consulting implies its share price may be lower than expected.

Turning Ideas Into Actions

- Reveal the 100 hidden gems among our Fast Growing Japanese Companies With High Insider Ownership screener with a single click here.

- Shareholder in one or more of these companies? Ensure you're never caught off-guard by adding your portfolio in Simply Wall St for timely alerts on significant stock developments.

- Maximize your investment potential with Simply Wall St, the comprehensive app that offers global market insights for free.

Want To Explore Some Alternatives?

- Explore high-performing small cap companies that haven't yet garnered significant analyst attention.

- Diversify your portfolio with solid dividend payers offering reliable income streams to weather potential market turbulence.

- Find companies with promising cash flow potential yet trading below their fair value.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.The analysis only considers stock directly held by insiders. It does not include indirectly owned stock through other vehicles such as corporate and/or trust entities. All forecast revenue and earnings growth rates quoted are in terms of annualised (per annum) growth rates over 1-3 years.

Valuation is complex, but we're here to simplify it.

Discover if BayCurrent Consulting might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About TSE:6532

Flawless balance sheet with reasonable growth potential.