Will Group, Inc. (TSE:6089) has announced that it will pay a dividend of ¥44.00 per share on the 24th of June. This makes the dividend yield 4.4%, which will augment investor returns quite nicely.

Check out our latest analysis for Will Group

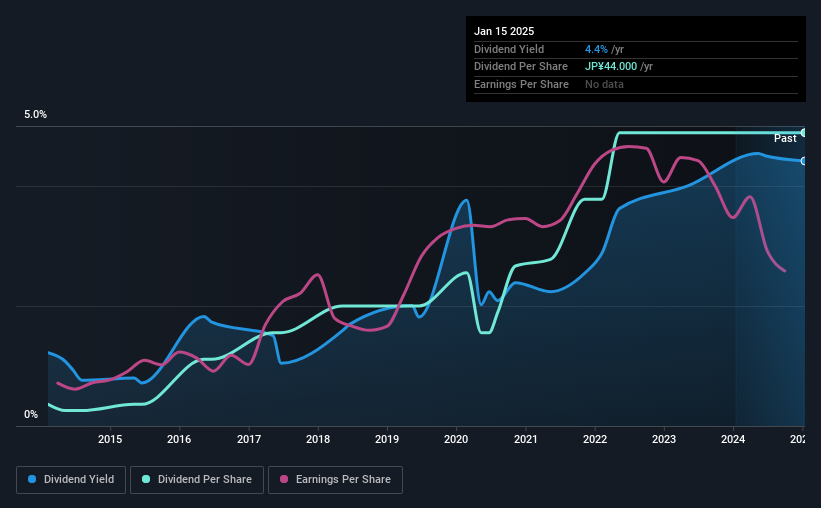

Will Group's Payment Could Potentially Have Solid Earnings Coverage

While it is great to have a strong dividend yield, we should also consider whether the payment is sustainable. Based on the last dividend, Will Group is earning enough to cover the payment, but then it makes up 345% of cash flows. The company might be more focused on returning cash to shareholders, but paying out this much of its cash flow could expose the dividend to being cut in the future.

EPS is set to fall by 3.9% over the next 12 months if recent trends continue. Assuming the dividend continues along recent trends, we believe the payout ratio could be 67%, which we are pretty comfortable with and we think is feasible on an earnings basis.

Dividend Volatility

The company's dividend history has been marked by instability, with at least one cut in the last 10 years. The annual payment during the last 10 years was ¥3.25 in 2015, and the most recent fiscal year payment was ¥44.00. This means that it has been growing its distributions at 30% per annum over that time. Will Group has grown distributions at a rapid rate despite cutting the dividend at least once in the past. Companies that cut once often cut again, so we would be cautious about buying this stock solely for the dividend income.

Dividend Growth May Be Hard To Achieve

Growing earnings per share could be a mitigating factor when considering the past fluctuations in the dividend. Over the past five years, it looks as though Will Group's EPS has declined at around 3.9% a year. If the company is making less over time, it naturally follows that it will also have to pay out less in dividends.

The Dividend Could Prove To Be Unreliable

Overall, it's nice to see a consistent dividend payment, but we think that longer term, the current level of payment might be unsustainable. While Will Group is earning enough to cover the payments, the cash flows are lacking. We would probably look elsewhere for an income investment.

Market movements attest to how highly valued a consistent dividend policy is compared to one which is more unpredictable. At the same time, there are other factors our readers should be conscious of before pouring capital into a stock. For instance, we've picked out 2 warning signs for Will Group that investors should take into consideration. Looking for more high-yielding dividend ideas? Try our collection of strong dividend payers.

If you're looking to trade Will Group, open an account with the lowest-cost platform trusted by professionals, Interactive Brokers.

With clients in over 200 countries and territories, and access to 160 markets, IBKR lets you trade stocks, options, futures, forex, bonds and funds from a single integrated account.

Enjoy no hidden fees, no account minimums, and FX conversion rates as low as 0.03%, far better than what most brokers offer.

Sponsored ContentValuation is complex, but we're here to simplify it.

Discover if Will Group might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About TSE:6089

Will Group

Provides human resource services in Japan and internationally.

Flawless balance sheet established dividend payer.

Market Insights

Community Narratives