- Japan

- /

- Professional Services

- /

- TSE:6089

Top Dividend Stocks To Consider In December 2024

Reviewed by Simply Wall St

As global markets navigate a complex landscape marked by rate cuts from the ECB and SNB, alongside expectations for a Fed rate cut, investors are witnessing mixed performances across major indices. While the Nasdaq Composite has reached new highs, other indexes have experienced declines amidst softening labor markets and inflationary pressures. In this environment, dividend stocks can offer stability and income potential, making them an attractive consideration for investors seeking to balance growth with reliable returns.

Top 10 Dividend Stocks

| Name | Dividend Yield | Dividend Rating |

| Guaranty Trust Holding (NGSE:GTCO) | 6.49% | ★★★★★★ |

| Peoples Bancorp (NasdaqGS:PEBO) | 5.02% | ★★★★★★ |

| Wuliangye YibinLtd (SZSE:000858) | 3.26% | ★★★★★★ |

| Southside Bancshares (NYSE:SBSI) | 4.54% | ★★★★★★ |

| Guangxi LiuYao Group (SHSE:603368) | 3.24% | ★★★★★★ |

| Padma Oil (DSE:PADMAOIL) | 7.44% | ★★★★★★ |

| Citizens & Northern (NasdaqCM:CZNC) | 6.00% | ★★★★★★ |

| Shaanxi International TrustLtd (SZSE:000563) | 3.16% | ★★★★★★ |

| Premier Financial (NasdaqGS:PFC) | 4.82% | ★★★★★★ |

| Banque Cantonale Vaudoise (SWX:BCVN) | 5.25% | ★★★★★★ |

Click here to see the full list of 1970 stocks from our Top Dividend Stocks screener.

Let's explore several standout options from the results in the screener.

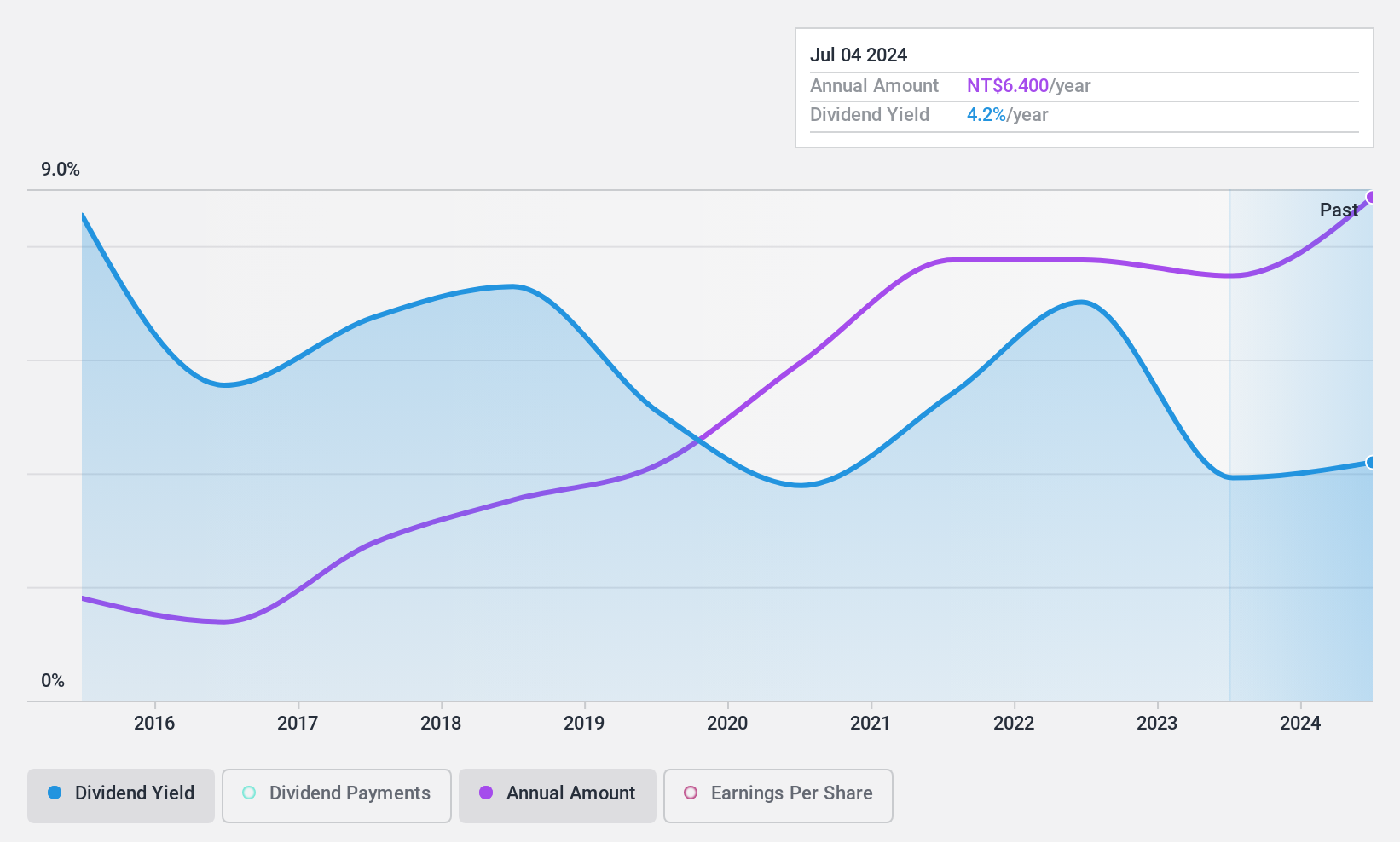

Argosy Research (TPEX:3217)

Simply Wall St Dividend Rating: ★★★★☆☆

Overview: Argosy Research Inc. manufactures and sells electronic components and connectors across Asia, the United States, and internationally, with a market cap of NT$14.37 billion.

Operations: Argosy Research Inc.'s revenue from the manufacturing and sales of electronic component products is NT$3.32 billion.

Dividend Yield: 4%

Argosy Research's dividend payments have been volatile over the past decade, with a payout ratio of 62.3% and a cash payout ratio of 77.1%, indicating dividends are covered by earnings and cash flows. Despite its low dividend yield compared to top-tier payers, dividends have increased over ten years. Recent financials show strong sales growth to TWD 2.52 billion for nine months in 2024, with net income rising to TWD 737 million, supporting future payouts amidst executive changes focused on sustainability and governance.

- Click here and access our complete dividend analysis report to understand the dynamics of Argosy Research.

- Upon reviewing our latest valuation report, Argosy Research's share price might be too pessimistic.

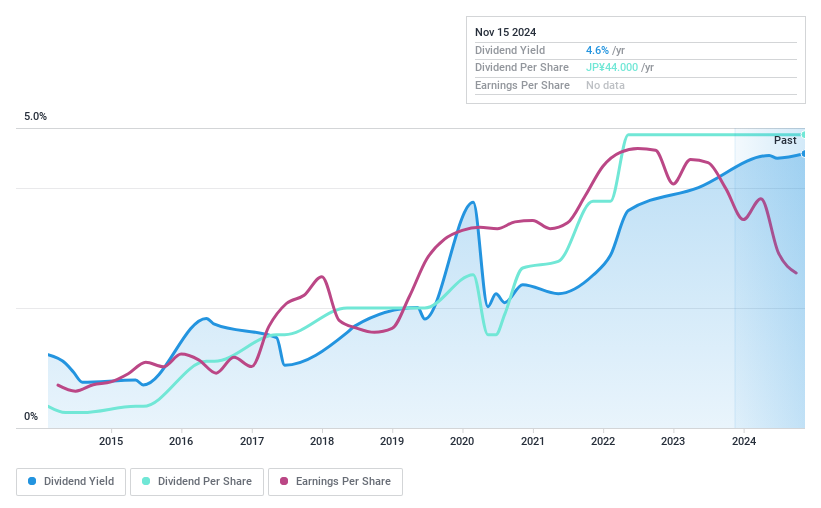

Will Group (TSE:6089)

Simply Wall St Dividend Rating: ★★★★☆☆

Overview: Will Group, Inc. offers human resource services both in Japan and internationally, with a market capitalization of ¥22.21 billion.

Operations: Will Group, Inc. generates revenue from its Domestic Working Business segment, which contributes ¥83.11 billion, and its Overseas Working Business segment, which adds ¥55.96 billion.

Dividend Yield: 4.5%

Will Group's dividend yield of 4.46% ranks in the top 25% of JP market payers, yet its payments have been volatile and unreliable over the past decade. The payout ratio is reasonable at 53.2%, but a high cash payout ratio of 344.8% raises concerns about sustainability from cash flows alone. Recent guidance revisions indicate improved operating profit due to cost control and productivity gains, which may influence future dividend stability despite current challenges in coverage by free cash flow.

- Unlock comprehensive insights into our analysis of Will Group stock in this dividend report.

- The valuation report we've compiled suggests that Will Group's current price could be inflated.

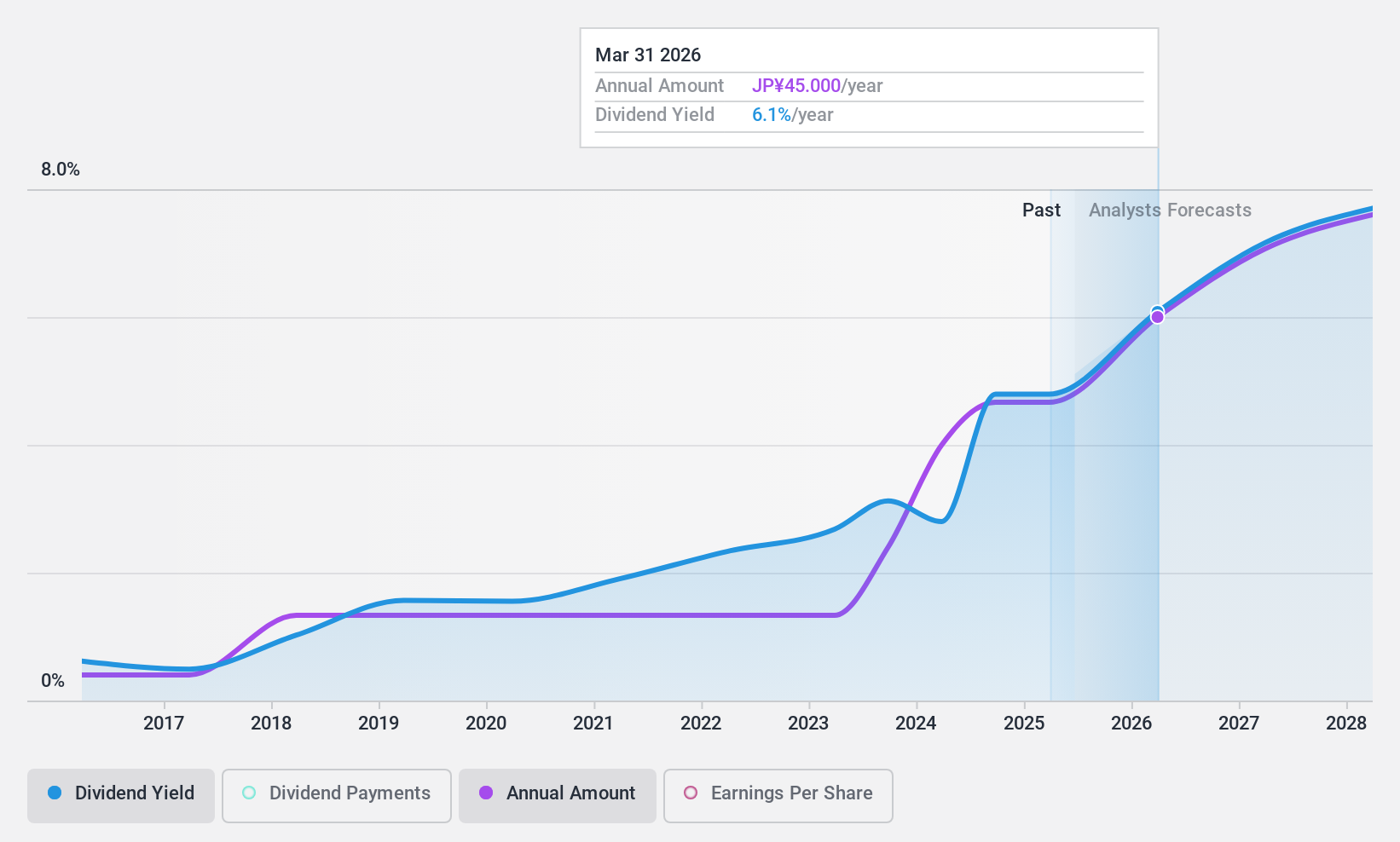

Futaba Industrial (TSE:7241)

Simply Wall St Dividend Rating: ★★★★★★

Overview: Futaba Industrial Co., Ltd. operates in the manufacturing and sale of automotive parts, information environment equipment, equipment for external sales, and agricultural equipment both in Japan and internationally, with a market cap of ¥61.21 billion.

Operations: Futaba Industrial Co., Ltd.'s revenue segments are comprised of ¥33.82 billion from Japan, ¥22.03 billion from North America, ¥7.22 billion from China, ¥6.87 billion from Europe, and ¥5.26 billion from Asia.

Dividend Yield: 5%

Futaba Industrial offers a compelling dividend profile with a 5% yield, placing it in the top 25% of JP market payers. The company's dividends have been stable and reliably growing over the past decade, supported by a low payout ratio of 43.1% and an even lower cash payout ratio of 20.5%, indicating strong coverage by both earnings and cash flows. Despite recent declines in profit margins from last year, its valuation remains attractive compared to peers.

- Navigate through the intricacies of Futaba Industrial with our comprehensive dividend report here.

- Insights from our recent valuation report point to the potential undervaluation of Futaba Industrial shares in the market.

Taking Advantage

- Get an in-depth perspective on all 1970 Top Dividend Stocks by using our screener here.

- Hold shares in these firms? Setup your portfolio in Simply Wall St to seamlessly track your investments and receive personalized updates on your portfolio's performance.

- Elevate your portfolio with Simply Wall St, the ultimate app for investors seeking global market coverage.

Searching for a Fresh Perspective?

- Explore high-performing small cap companies that haven't yet garnered significant analyst attention.

- Fuel your portfolio with companies showing strong growth potential, backed by optimistic outlooks both from analysts and management.

- Find companies with promising cash flow potential yet trading below their fair value.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

If you're looking to trade Will Group, open an account with the lowest-cost platform trusted by professionals, Interactive Brokers.

With clients in over 200 countries and territories, and access to 160 markets, IBKR lets you trade stocks, options, futures, forex, bonds and funds from a single integrated account.

Enjoy no hidden fees, no account minimums, and FX conversion rates as low as 0.03%, far better than what most brokers offer.

Sponsored ContentValuation is complex, but we're here to simplify it.

Discover if Will Group might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About TSE:6089

Will Group

Provides human resource services in Japan and internationally.

Flawless balance sheet established dividend payer.

Market Insights

Community Narratives