Advertisement

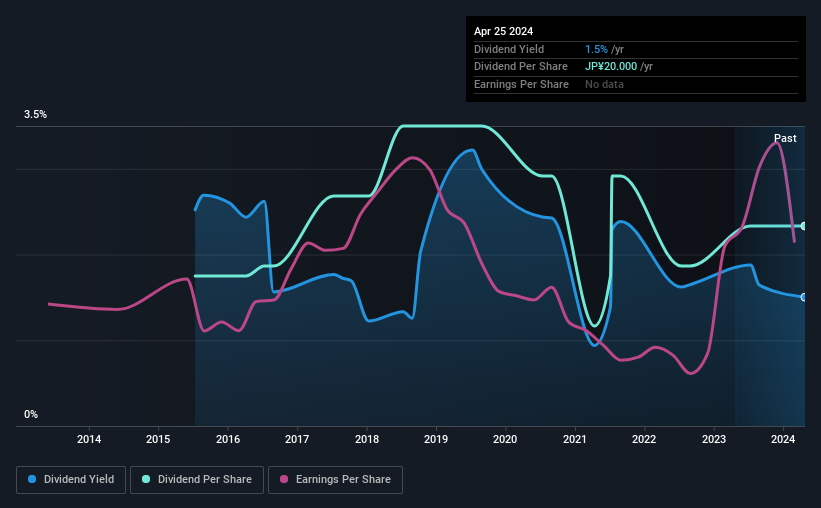

Sanki Service Corporation (TSE:6044) is reducing its dividend from last year's comparable payment to ¥20.00 on the 28th of August. The dividend yield will be in the average range for the industry at 1.5%.

Check out our latest analysis for Sanki Service

Sanki Service's Payment Has Solid Earnings Coverage

While it is always good to see a solid dividend yield, we should also consider whether the payment is feasible. However, based ont he last payment, Sanki Service was earning enough to cover the dividend pretty comfortably. The business is returning a large chunk of its cash to shareholders, which means it is not being used to grow the business.

EPS is set to fall by 3.2% over the next 12 months if recent trends continue. Assuming the dividend continues along recent trends, we believe the payout ratio could be 31%, which we are pretty comfortable with and we think is feasible on an earnings basis.

Sanki Service's Dividend Has Lacked Consistency

Looking back, Sanki Service's dividend hasn't been particularly consistent. This suggests that the dividend might not be the most reliable. The dividend has gone from an annual total of ¥15.00 in 2015 to the most recent total annual payment of ¥20.00. This implies that the company grew its distributions at a yearly rate of about 3.2% over that duration. We're glad to see the dividend has risen, but with a limited rate of growth and fluctuations in the payments the total shareholder return may be limited.

Dividend Growth May Be Hard To Achieve

Given that the dividend has been cut in the past, we need to check if earnings are growing and if that might lead to stronger dividends in the future. Sanki Service has seen earnings per share falling at 3.2% per year over the last five years. A modest decline in earnings isn't great, and it makes it quite unlikely that the dividend will grow in the future unless that trend can be reversed.

Our Thoughts On Sanki Service's Dividend

In summary, dividends being cut isn't ideal, however it can bring the payment into a more sustainable range. While Sanki Service is earning enough to cover the dividend, we are generally unimpressed with its future prospects. Overall, we don't think this company has the makings of a good income stock.

Companies possessing a stable dividend policy will likely enjoy greater investor interest than those suffering from a more inconsistent approach. Still, investors need to consider a host of other factors, apart from dividend payments, when analysing a company. For example, we've picked out 2 warning signs for Sanki Service that investors should know about before committing capital to this stock. Is Sanki Service not quite the opportunity you were looking for? Why not check out our selection of top dividend stocks.

New: Manage All Your Stock Portfolios in One Place

We've created the ultimate portfolio companion for stock investors, and it's free.

• Connect an unlimited number of Portfolios and see your total in one currency

• Be alerted to new Warning Signs or Risks via email or mobile

• Track the Fair Value of your stocks

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About TSE:6044

Sanki Service

Engages in the provision of design, construction, management, and maintenance services for various equipment in Japan and internationally.

Adequate balance sheet second-rate dividend payer.

Market Insights

Advertisement

Community Narratives

For the Emperor: Why Games Workshop Could Be a Star Investment

Fair Value UK£160.00|0.5% overvalued

RO

Community Contributor

Securitas will boost margins with AI and tech-driven services

Fair Value SEK 260.91|44.5% undervalued

UN

Community Contributor

A Leader in EV Charging with Growth Potential

Fair Value €27.00|18.7% undervalued

TI

Community Contributor