- Japan

- /

- Commercial Services

- /

- TSE:4125

Sanwayuka Industry's (TSE:4125) Weak Earnings May Only Reveal A Part Of The Whole Picture

A lackluster earnings announcement from Sanwayuka Industry Corporation (TSE:4125) last week didn't sink the stock price. We think that investors are worried about some weaknesses underlying the earnings.

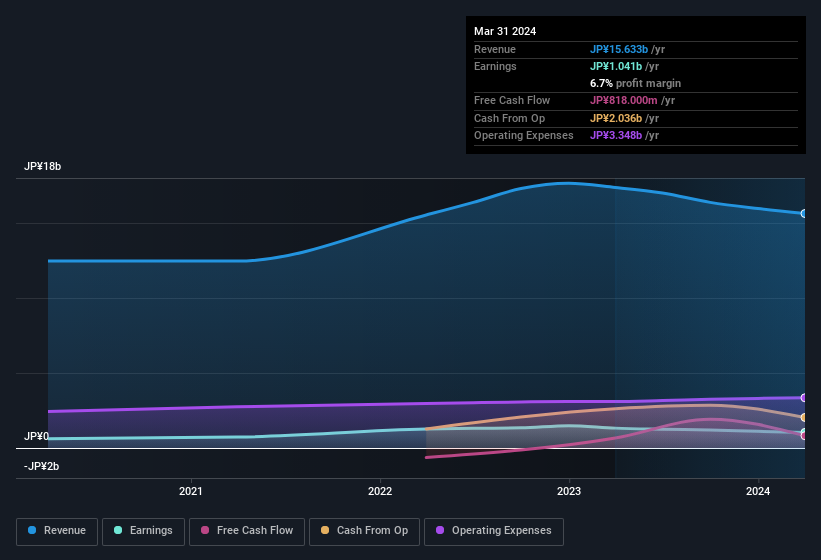

View our latest analysis for Sanwayuka Industry

The Impact Of Unusual Items On Profit

Importantly, our data indicates that Sanwayuka Industry's profit received a boost of JP¥150m in unusual items, over the last year. While it's always nice to have higher profit, a large contribution from unusual items sometimes dampens our enthusiasm. When we crunched the numbers on thousands of publicly listed companies, we found that a boost from unusual items in a given year is often not repeated the next year. And that's as you'd expect, given these boosts are described as 'unusual'. Assuming those unusual items don't show up again in the current year, we'd thus expect profit to be weaker next year (in the absence of business growth, that is).

That might leave you wondering what analysts are forecasting in terms of future profitability. Luckily, you can click here to see an interactive graph depicting future profitability, based on their estimates.

Our Take On Sanwayuka Industry's Profit Performance

Arguably, Sanwayuka Industry's statutory earnings have been distorted by unusual items boosting profit. Because of this, we think that it may be that Sanwayuka Industry's statutory profits are better than its underlying earnings power. Nonetheless, it's still worth noting that its earnings per share have grown at 12% over the last three years. The goal of this article has been to assess how well we can rely on the statutory earnings to reflect the company's potential, but there is plenty more to consider. If you'd like to know more about Sanwayuka Industry as a business, it's important to be aware of any risks it's facing. While conducting our analysis, we found that Sanwayuka Industry has 1 warning sign and it would be unwise to ignore this.

Today we've zoomed in on a single data point to better understand the nature of Sanwayuka Industry's profit. But there are plenty of other ways to inform your opinion of a company. Some people consider a high return on equity to be a good sign of a quality business. So you may wish to see this free collection of companies boasting high return on equity, or this list of stocks with high insider ownership.

New: Manage All Your Stock Portfolios in One Place

We've created the ultimate portfolio companion for stock investors, and it's free.

• Connect an unlimited number of Portfolios and see your total in one currency

• Be alerted to new Warning Signs or Risks via email or mobile

• Track the Fair Value of your stocks

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About TSE:4125

Sanwayuka Industry

Engages in the disposal, recycling, and management of industrial waste in Japan.

Excellent balance sheet slight.

Market Insights

Community Narratives